You may buy their attractive home goods, and many of us do. But make no mistake, Wayfair (NYSE:W) stock isn’t cheap. And for investors eyeing today’s pricey merchandise, you may want to make sure there’s a guaranteed return policy. Let me explain why you want to be really careful around Wayfair stock.

Wayfair bulls need to respectfully pull up a chair and consider today versus yesterday or that time when the bells tolled for the market.

The online seller of any and most anything home goods-related at competitive prices has been on a tear in 2020. Shares are up more than 100% since the beginning of the year. And that’s not the best Wayfair has offered investors this year either.

Since March’s terrifying and broad-based bottom caused by Wall Street’s initial pricing of the novel coronavirus, a few investors in W shares are up a stunning 840%, plus or minus a percent or two. That’s enough to even make competitors Amazon (NASDAQ:AMZN), Target (NYSE:TGT) and most certainly Macy’s (NYSE:

M), blush for sure.

Wayfair’s positive and well-above-the-market returns this year are directly linked to extended and even terminal stay-at-home marching orders from the government and some employers.

I’m confident that’s not front page news. Still, the fact is despite a substantial uptick in business driven by Covid-19, Wayfair is not the company it once was in more than one way. And that could be bad news for investors buying shares today.

From a valuation standpoint, Wayfair is now a $20 billion large-cap still mired in red ink with sales growth which could easily prove an aberrant blip on the long-term radar. Okay, to be fair and as InvestorPlace’s Louis Navellier notes, analysts do expect sales to grow 35% in 2020 on top of already impressive quadrupling of revenues since 2015.

Then again and as the price chart stresses, Wall Street was obviously wildly wrong about Wayfair not so long ago. And those same kind of conditions are taking shape in shares today.

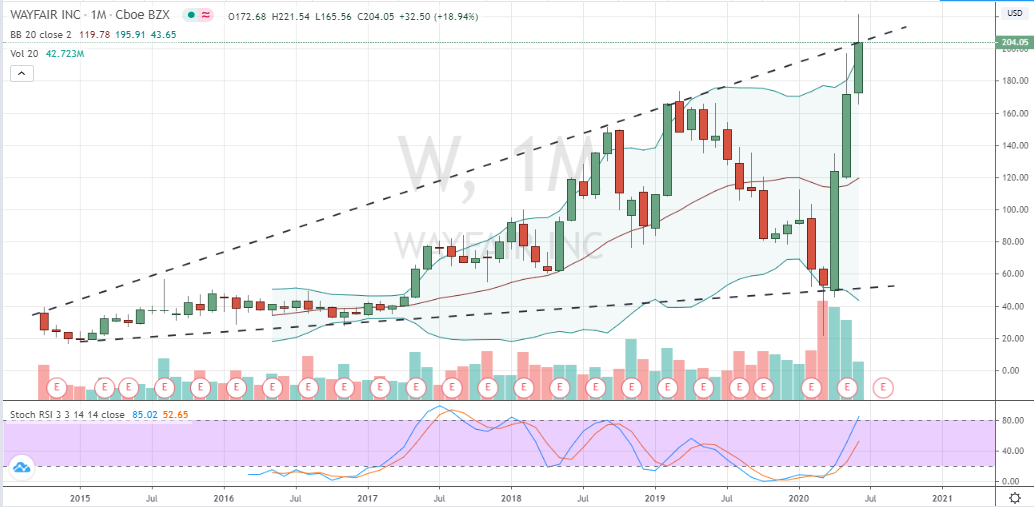

Wayfair Stock Monthly Price Chart

Click to Enlarge

If nothing else, Wayfair’s performance from its low of $21.70 set on March 19th reminds us that a forward-looking market isn’t always perfectly priced. But there is something else too.

Today’s pricing of the stock is also cautioning that investors are likely getting well-ahead of themselves.

Technically and as the provided monthly view of Wayfair shows, shares are challenging angular and Bollinger Band resistance following its uninterrupted extension in value the past three months. Stochastics is also nearing overbought levels.

The price action is the opposite, but strikingly similar to the panic activity found at the March bottom when shares pushed through technical trend-line and Bollinger supports. And bottom-line, it’s concerning.

My advice for Wayfair today is timeless and important to remember. And that is, let the buyer beware. Net, net based on the price chart and spotty fundamentals, the increased chance for a corrective move has our attention.

But in fear of sounding like one of Wayfair’s heavy bearish short population of nearly 37%, for investors unconvinced a pullback or larger correction is in order, I’d suggest hedging that stock purchase.

The Bottom Line on Wayfair

My recommendation to Wayfair investors is to buy a married put or better yet, a collar combination to limit and reduce the cost of the fully-protected protection.

One favored spread that should keep investors happy and maybe a good deal happier depending on Wayfair’s performance going forward is the August $190 put / $240 call combination.

Sure, you’ll pay a premium above the stock’s current market price to own this particular collar. But the protective value and still very generous return potential, if our concerns are unfounded, are worth every dollar in our estimation.

Disclosure: Investment accounts under Christopher Tyler’s management do not currently own positions in securities mentioned in this article. The information offered is based upon Christopher Tyler’s observations and strictly intended for educational purposes only; the use of which is the responsibility of the individual. For additional market insights and related musings, follow Chris on Twitter @Options_CAT and StockTwits.