The Chinese take their education very seriously. Therefore, at first glance, it wasn’t too surprising to see GSX Techedu (NYSE:GSX), a “technology-driven education company” headquartered in Beijing, as one of the top performing investments on the New York Stock Exchange this year. Of course, China has also garnered a reputation for less-than-stellar business practices. On Friday, some of the harshest accusations against the company apparently took its toll on GSX stock.

Most notably, Andrew Left of Citron Capital, one of America’s leading hedge funds, has called out GSX Techedu for fraud. In an email to me, Left stated bluntly, “GSX is a complete fraud a complete scam. They are harming legitimate Chinese companies and must be investigated immediately.” Specifically, the famed (or notorious, depending on your view) short-seller believes that:

- either this is the greatest business since the early days of Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) or a fraud.

- an immediate fraud investigation is needed of this Chinese company.

- this matter is completely spitting in the face of the White House’s insistence of strong auditing standards.

- Ultimately, this is a complete stock fraud – concluding between 70% to 80% of this company’s users are fake.

Of course, these are monumentally aggressive accusations against GSX stock. For the interest of time, however, I’d like to tackle the last claim about fake users.

GSX Stock Faces Serious Heat Regarding Fake Users, Revenue

Some businesses have been known to stretch the rules. But outright faking users – and therefore revenue – is one of the biggest scams you can commit against the investment community. Would GSX Techedu commit such a brazen crime?

According to Left and multiple sources, the answer is an alarming yes. Consider that there is a request on Change.org demanding that the Securities and Exchange Commission take immediate action against GSX stock.

Moreover, Citron Research released a detailed study in April of this year, analyzing line by line evidence of fake users propping up a shell of a business. Additionally, the research firm exposed unusual revenue variance between GSX and its competitors.

I encourage everyone to read Citron’s report carefully. But in summary, GSX is a student that decides to cheat on his tests. Rather than cheat smartly, though, he gets all the answers correctly, besting the top achievers in the class. Ordinarily, that would draw a teacher’s attention.

So it is with GSX stock. Further, it’s not out of the realm of possibility that a Chinese company would cheat this shamelessly. It wasn’t too long ago that investigators exposed Luckin Coffee (OTCMKTS:LKNCY) for faking its revenue.

Yet Citron in its research paper stated that “Luckin is by far a more prominent coffee shop than GSX is an education provider.” Bold stuff. However, some fraud accusations can lead to an endless rabbit hole. Is there enough public information to suggest concern with GSX stock?

Without access to Citron’s proprietary information and without the time and resources to perform “in-person” investigations, I’m left to rely on variance analytics on publicly disclosed financials. What I discovered should give you pause before even thinking about buying GSX stock.

Unusual Success Raises Eyebrows

As a China-based education company, GSX Techedu should have growth metrics similar to companies in its industry. They are:

- TAL Education Group (NYSE:TAL)

- New Oriental Education & Technology Group (NYSE:EDU)

- Koolearn Technology (OTCMKTS:KLHTF)

- China Online Education Group (NYSE:COE)

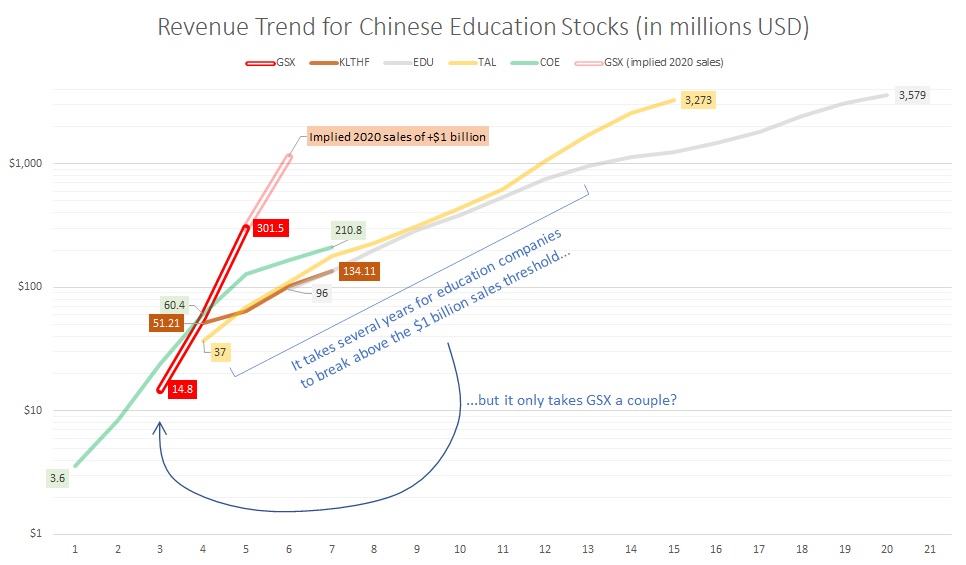

Despite being the new kid on the block, GSX Techedu enjoys an unusually robust revenue trend, a trend that is practically vertical against the competition. Further, given the dramatic explosion of sales in its most recent quarter, the company is on track to exceed revenue of $1 billion if the trajectory holds.

Click to Enlarge

However, the problem is that it took many years for TAL and New Oriental Education to breach the billion-dollar threshold. But in GSX’s case, it will do so in a couple of years thanks to its meteoric trajectory. Of course, this growth narrative has caused GSX stock to skyrocket. But Citron and others, including Grizzly Reports and Muddy Waters Research, have raised red flags.

According to Citron, it’s jarring that the Chinese media never called GSX disruptive or gave it much praise following its initial public offering. As its research paper states:

You cannot hide a fast-growing education company in China. China’s media covers the education industry the same way the U.S. media covers the Kardashians. If this company had 432% revenue growth in one year on that scale – it would be widely known and widely reported.

To be fair, achieving success, no matter how extreme, isn’t a smoking gun. Nevertheless, it arouses suspicion, especially when GSX spends so little on its research and development. Upon closer inspection, it’s also highly improbable that GSX stock can justify its premium.

Wildly Anomalous Growth Rates

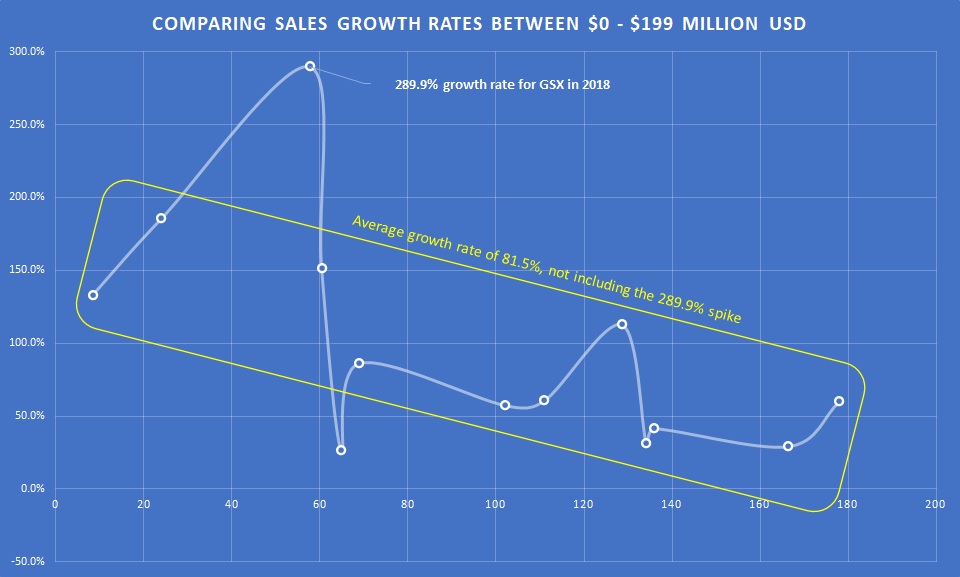

In 2018, GSX generated revenue of $57.7 million, up nearly 290% from 2017’s tally. That alone is anomalous compared to growth rates seen in other Chinese education providers.

Among generated sales between zero to under $200 million, the average year-to-year sales growth rate (not inclusive of the aforementioned 290% spike) is 81.5%. Out of companies not named GSX, the highest YOY rate generated was 185.7%. As you would expect from the law of rising numbers, as the nominal comparisons increased, growth rates trended down.

Click to Enlarge

Thus, I find the 290% spike highly unusual. Still, I will concede that there’s some element of plausible deniability here.

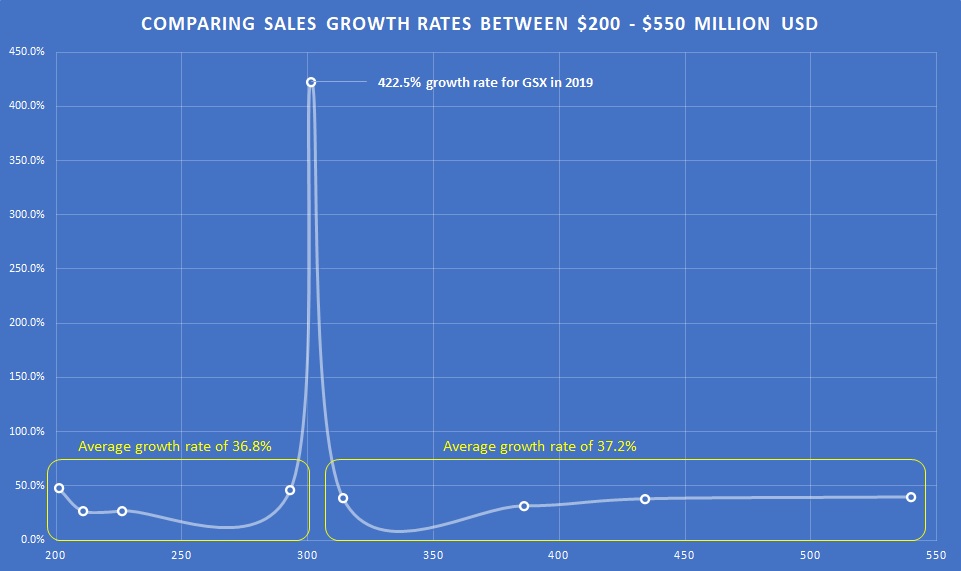

But there’s no such margin afforded when you compare growth rates among generated sales between $200 million and $550 million. In this framework, the average YOY growth rate (again, not including GSX’s rate) is much lower than the first framework at 37%. This makes sense because of the law of large numbers – the larger the comparisons, the “harder” it is to generate big percentage gains.

Click to Enlarge

Yet against the average growth rate backdrop of 37%, GSX stuns with a whopping 422.5% rate. This occurred in 2019, when the company rang up $301.5 million (versus $57.7 million in 2018).

Simply put, this type of growth does not happen in this sector. So, bearish analysts are right to be skeptical.

What the Real Picture Most Likely Is

Interestingly, when you back out GSX’s absurd growth rates and replace them with reasonable ones that are in line with industry averages, you get a clearer picture of GSX stock. It isn’t a pretty one, to be sure. But at least you have an idea of what you’re really dealing with.

Here’s what I did. Rather than 290% YOY growth in 2018, I assumed 210%. This is still generous but brings the framework toward the credible end of the spectrum. From this exercise, I have 2018 revenue of just under $45.9 million.

Then, for 2019, I dramatically discounted the growth rate to 88.2%. This is far more reasonable for a Chinese education company that has generated at least $40 million in sales. Following some simple calculations, I get 2019 revenue of $86.3 million.

That’s only 28.6% of reported 2019 revenue or 71.4% down from the reported tally. Hence, Andrew Left’s claims that 70% to 80% of GSX’s users are fake have credibility under peer review. When you back out the alleged fraud, the company represents roughly a quarter of what it claims.

Now, this isn’t a wholesale endorsement to short GSX stock. Shorting is very risky business. What I’m confident about, though, is that you should perform extensive research before buying shares. These accusations have more meat on them than you might think.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.