One of 2020’s largest initial public offerings (IPOs), Rocket Mortgage (NYSE:RKT), formerly Quicken Loans, has also been one of the strangest. Shares in the mortgage originator have swung wildly from its $18 IPO price to almost $29 (and then back down again) as investors have second-guessed the value of RKT stock. It’s been a strangely wild ride for such a large company.

With shares rebounding yet again, it’s time to ask: is RKT stock a good long-term investment?

Upending Mortgage Lending

In just two short years, the Detroit-based fintech company has quietly become America’s largest mortgage originator. And with only a 9.2% market share in a massive $2.2 trillion market, the company has ample room to grow.

But does that make RKT stock worth it?

We’re going to take a long, hard look at the business, regulation, and valuation of RKT stock, and how investors should play one of 2020’s largest IPOs.

A Solid Core Business

As its name suggests, Rocket primarily operates a mortgage origination business. Customers call (or more commonly, use its mobile app or website) to get a new mortgage or refinance. The firm will then either approve or deny the loan, quote rates, and perform a title insurance check. In 2019, Rocket originated $145 billion of such mortgages.

The company, however, doesn’t usually retain the loans themselves. Instead, they sell more than 90% of all loans to government-sponsored entities, such as Fannie Mae (OTCMKTS:FNMA) and Freddie Mac (OTCMKTS:FMCC), for securitization. (The lowest-quality mortgages are usually sold to Fannie Mae).

So how does Rocket Mortgage make money? Three ways. Firstly, all mortgage originators earn a fee every time they write a mortgage. The amount collected typically runs between 0.5% – 1%, which adds up quickly. Rocket made $4.9 billion in 2019 selling loans.

Secondly, Rocket also retains servicing contracts. That means they’re responsible for collecting payments and managing the relationship with borrowers. Not every originator works in this business, since it’s a steadier stream of income, but can quickly turn risky if borrowers default. In 2019, the segment amounted to a smaller $950 million for Rocket.

Finally, Rocket also generates income from extra services, such as title insurance ($558.6 million revenue), marketing ($237.2 million in revenue), and real estate agent services ($43.1 million).

Rocketing growth at Rocket Mortgage

It sounds like a straightforward business, doesn’t it? But how did Rocket Mortgage become America’s top mortgage originator so quickly?

There are two key reasons.

Reason 1: Rocket’s Online Model

Firstly, Rocket is an online-only company. Unlike its major bank competitors, Rocket has no need to sink cash into a nationwide network of physical branches. Instead, the company invests heavily in its website, mobile app, and customer service capabilities.

It sounds like a minor step, but it’s worked amazingly in the stodgy financial world. Rocket boasts a 76% retention rate for refinancing, compared to an industry average of just 22%. And its J.D. Power Net Promoter Score (NPS), a measure of consumer satisfaction, stands at 74, compared to an industry average of just 16.

Rocket’s online-only model also gives the company a massive efficiency advantage. The average loan takes only 32 days to close, or 25% faster than competitors. According to Nerdwallet, its fee rate typically runs just 0.5% of the loan amount, rather than the typical 0.5% – 1% range.

In other words, the company does a far better job providing quality services online at lower costs.

But Rocket’s success also had to do with luck …

Reason 2: Rocket Mortgage Isn’t a Bank

Rocket’s biggest boost came from unintentional consequences of U.S. banking legislation.

When most people think of the 2008 financial crisis, they see the failure of banks and regulations. But what happened afterwards was equally groundbreaking. In response to the crisis, governments created a slew of rules to reduce the risk of future bank crises. These laws, known as Basel III, forced commercial banks to hold far more capital on their balance sheets.

While this made banks far safer, it had an unintended consequence: it created a vacuum in riskier lending. And non-bank fintech startups saw the opportunity.

- Peer-to-peer lending: Lending Club, Prosper

- Personal finance: SoFi, OneMain

- Prepaid debit cards: Green Dot, NetSpend

These companies all act as middlemen in the financial world: focusing on customer acquisition and immediately selling off loans to third parties.

Rocket Mortgage has been among these non-bank firms. Unencumbered by pesky capital requirements, RKT has been free to issue mortgages far faster than traditional banks. When mortgage rates dropped in 2019, Rocket processed 74% more originations as customers rushed to refinance.

Banks, on the other hand, can’t ramp up as fast. Instead, they’re forced to maintain capital since the process involves the bank’s own money. Put another way, banks haven’t followed Rocket Mortgage because they can’t take the business. It’s no surprise that their share in mortgage originations have steadily declined since 2007.

There’s an irony to the story. Over time, Rocket has started to look more like a bank than an internet startup; its balance sheet is stuffed full of loans that were once destined for Fannie Mae or Freddie Mac. Today, the company has grown its held-for-sale loan portfolio to $12 billion. While that’s still smaller than Wells Fargo’s (NYSE:WFC) $19.8 billion figure, keep in mind that Wells has an equity base 50 times larger than Rocket’s.

So what can go wrong for Rocket as it starts to resemble a bank? Plenty.

Lack of Regulation Leads to Risk-Taking

Rocket’s free-wheeling lending comes with significant risk.

While low capital requirements mean strong growth in good times, they can bankrupt a company in bad times (as banks realized during the 2008 financial crisis). Even mortgage originators aren’t immune. “The business of servicing mortgages can become capital-intensive if a mortgage goes bad,” explains The Economist. “The servicing firm must carry the costs until the mortgage is repaid—which can take years.”

There’s more. During the financial crisis, the U.S. government forced many banks to take back some of their mortgages or pay fines. That means the loans RKT passes off to Fannie Mae and Freddie Mac still retain an element of risk.

If a mortgage crisis happens again, Rocket could find itself responsible for far more than just the $12 billion on its books. And with just $3.6 billion of equity, Rocket shareholders could get wiped out in a hurry. That’s what makes RKT stock so risky and hard to value.

What’s RKT Stock Worth?

There are two opposing forces to valuing RKT stock. On the one hand, RKT will grow fast thanks to light regulations of non-bank companies. The U.S. government has made little recent effort in reining in non-bank startups. On the other hand, RKT retains a massive amount of financial risk because of its leveraged capital structure.

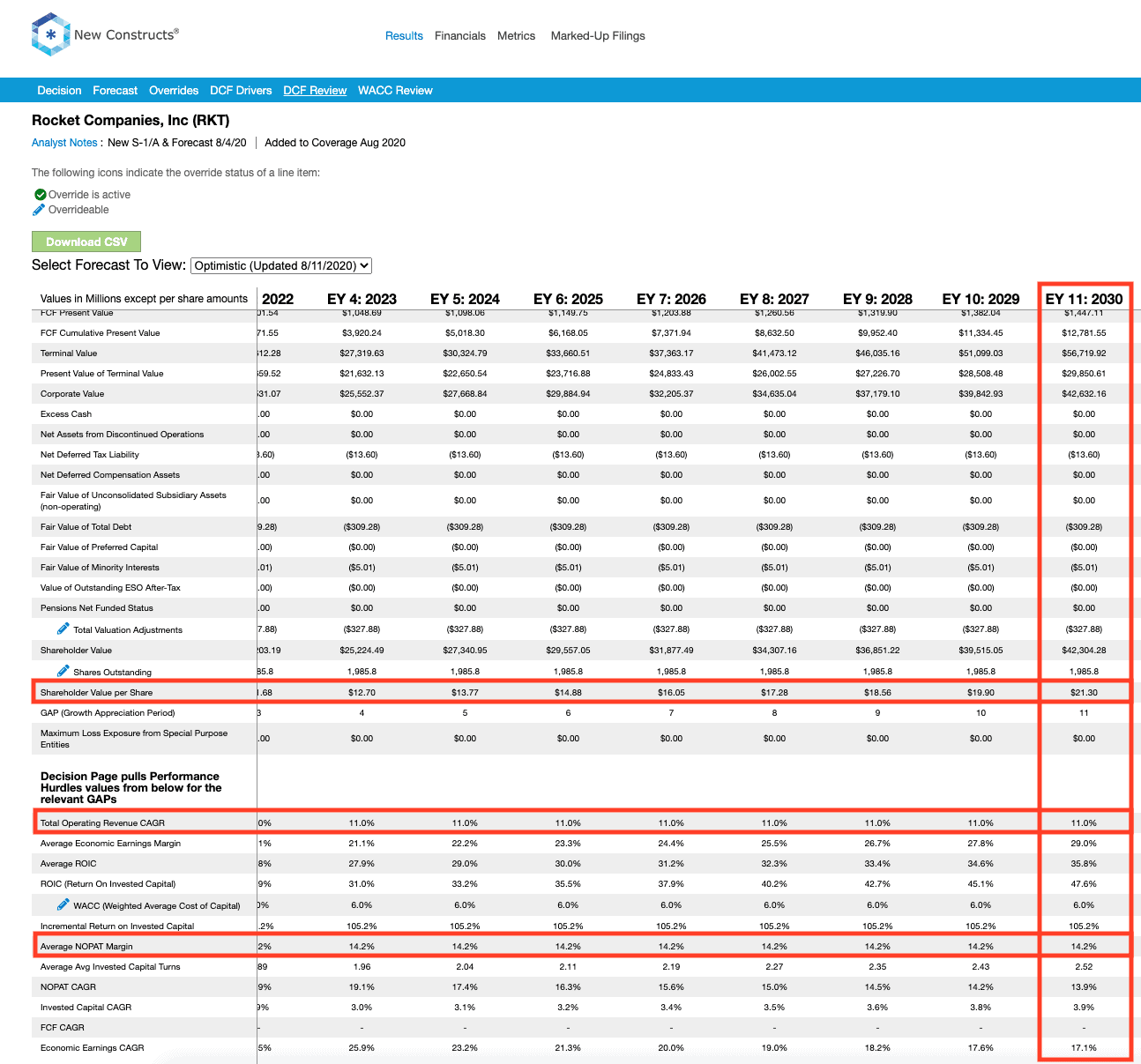

So, what’s the company worth? An analysis by David Trainer of stock valuation firm New Constructs shows, RKT would have to expand Net Operating Profit (NOPAT) margins from 11% to 14% and maintain an 11% growth rate over the next 11 years to justify a $22/share stock price.

{kind=link}

New Constructs has a $21.30 price target for RKT Stock

That’s certainly possible for Rocket Companies. RKT still only has a tiny share in U.S. mortgage originations, and the auto/personal loan segments remain mostly untapped. Bullish investors will quickly point out that RKT can also use its existing relationships to cross-sell its other financial products. Raising its growth rate to 16% puts fair-value closer to $34.30.

In an even more upbeat case, a 20% growth rate suggests $45 fair value.

On the flip-side, risk-averse investors will point out that RKT’s financials look more like a highly leveraged bank’s. In July, Moody’s, a credit rating service, affirmed its Ba1 junk rating on the company’s senior unsecured debt on concerns over rising delinquencies. It’s a common problem in the financial world: the average price-to-earnings (P/E) ratio for financial institutions is just 7.4x vs. 27.5x P/E for non-financial companies.

“Mortgage companies … have precisely zero revenue visibility, limited revenue sustainability, and their margins are highly correlated to industry volumes”, wrote Susquehanna analyst Jack Micenko in an industry note. He estimates RKT stock fair value at just $18.

In truth, RKT’s valuation lies somewhere in between the extremes.

What’s Next for RKT?

As interest rates stop falling and the refinancing market dries up, Rocket must resist the siren’s call of holding more mortgages on its balance sheet to generate income. It’s easy money in good times, but carries a lot of risk.

But will they hold off?

Very possibly. Given billionaire founder Dan Gilbert’s long track record, there’s a good chance the company will avoid the temptation and stick to their lucrative front-end product.

But the moment Rocket starts padding its balance sheet to earn banking profits, investors should run for the exits.

Tom Yeung, CFA, is a registered investment advisor on a mission to bring simplicity to the world of investing. On the date of publication, Tom Yeung did not have any positions in the securities mentioned.