If I was the President of the United States, more Americans will still be alive today. Further, I would have at least attempted to protect your portfolio from volatility, unlike some people. I’m not merely boasting for the heck of it. Rather, based on my February 2020 write-up about Dropbox (NASDAQ:DBX) and the possible impact to Dropbox stock, the hypothetical Enomoto administration would have been great for this country.

As CNN’s Brianna Keilar might say, let’s roll the tape. On Feb. 27, I stated the following:

If we didn’t have the coronavirus barreling down our necks, I’d be interested in DBX for both the near and long term. In my view, I liken Dropbox to Adobe (NASDAQ:ADBE). Both provide capabilities that allow individual workers to untether themselves from the physical workspace. Although the two organizations are obviously different, they each place the emphasis on the work product, not on where it gets done.

Plus, as the gig economy becomes more prevalent in our society, I anticipate higher demand for Dropbox’s modular platform. The beauty here is that it is as simple or as complicated as you want it to be. Frankly, many people and organizations don’t need a full-blown cloud architecture from the likes of Amazon (NASDAQ:AMZN) or Microsoft (NASDAQ:MSFT). DBX fills a gig economy niche, bolstering the case for Dropbox stock.

Unfortunately, the coronavirus presents multiple headwinds. First, Dropbox stock is a growth name and therefore depends on strong risk-on sentiment. However, this is the type of sentiment that is declining by the hour due to the epidemic. If this crisis worsens – and all indications suggest this is the case – investors will likely roll their funds into risk-off or safe-haven assets.

For my second and third points, I suggested that Dropbox’s international exposure put its revenue channels at risk, while back at home, “we’re on the cusp of a serious situation.” Therefore, at the time, I felt that Dropbox stock unnecessarily risky.

Dropbox Stock Has Come Full Circle

I’m going to let you in on a little secret. The life of any public commentator of any industry is not an easy one.

Sometimes, I’m not particularly happy with some of my takes. But in other cases, I’m glad I wrote what I did. In fact, there are moments when I wish I pulled a President Trump and doubled-down and tripled-down.

This is one of those moments.

Say what you want about my specific comments on Dropbox stock, I sleep very easy at night knowing that I warned the public about taking the novel coronavirus seriously. You can’t take that away from me. It’s on record.

But what else is on the record is that I didn’t have a chance to follow up on my analysis.

Yes, Dropbox stock tanked badly several days after my article was published. But as you know, the resilience of Americans surprised me. Specifically, companies adapted to the new normal, shifting to remote operations via rapid-fire integration.

And with that, my

InvestorPlace colleague David Moadel has the better take under the context of the new normal, writing “Given the world’s irreversible trend towards distributed work and collaboration, the reward-to-risk balance of Dropbox stock becomes increasingly favorable.”

Still, is Dropbox stock now a buy? For me, DBX has come full circle. On Feb. 27, shares were priced at $19.33. At time of writing, it’s exactly 33 cents higher. Just to be clear for our possible Infowars’ viewers, that 33 is just a coincidence. I’m not part of the Illuminati.

Having learnt the lesson of Covid-19, is Dropbox stock an undervalued opportunity like Moadel suggests? To answer, I’m going to roll a different tape, the math.

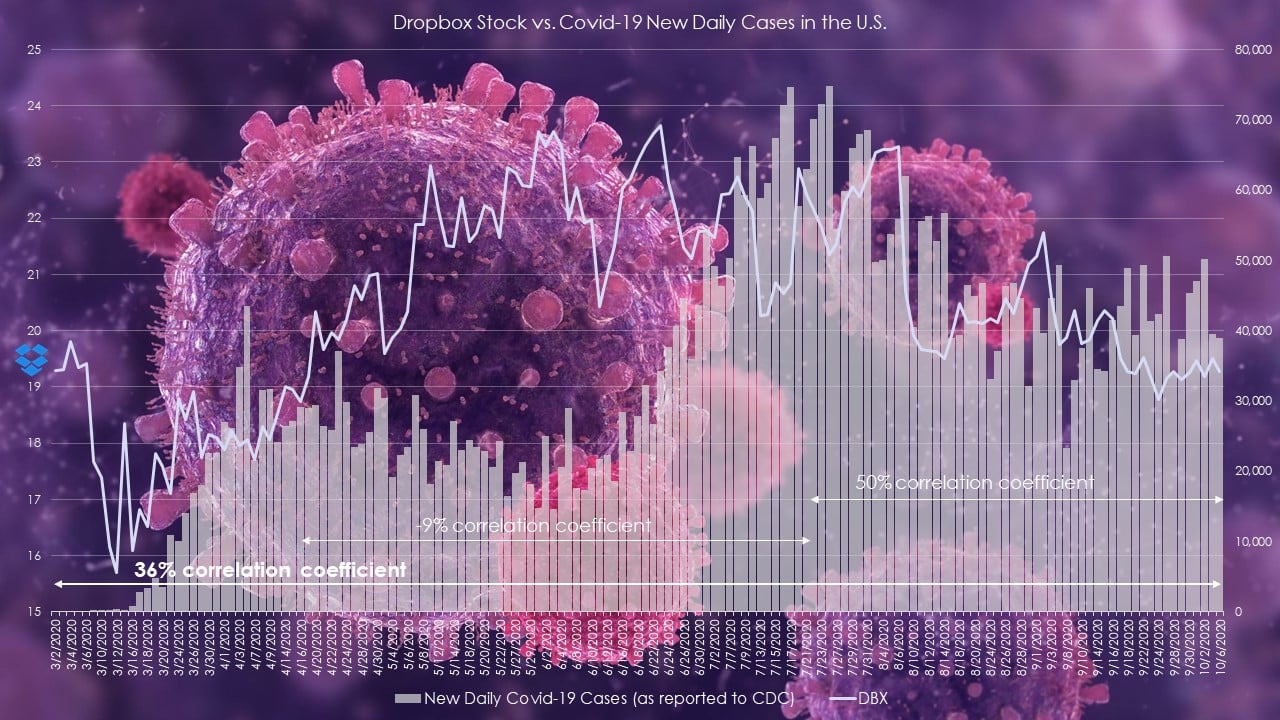

What I have in common with the incumbent is our shared love for math, facts and charts. If Moadel’s thesis is accurate, we should see a direct correlation between new daily coronavirus cases and DBX stock. As cases rise, so should demand for Dropbox’s services. So what does the data reveal? It’s inconclusive.

Click to Enlarge

From the beginning of March until Oct. 6, the correlation coefficient between DBX and coronavirus cases is 36%. That’s below the 40% threshold of where two trends are statistically significant. Further, between mid-April to mid-July, the coefficient dips to -9%, an insignificant relationship.

Finally, from mid-July to Oct. 6, the coefficient registers 50%. That is significant although the correlation could be stronger. Therefore, based on the math, DBX is not a convincing buy.

Many Questions Ahead for DBX

This isn’t to say that Moadel’s analysis is inaccurate. As he pointed out, DBX has flown under the radar compared to similar Covid plays. Therefore, it’s possible that Dropbox is suffering from a saturation of competition.

After all, this isn’t the only platform that facilitates distributed work and collaboration. And if the markets are ignoring DBX, it could be for a reason.

With a questionable correlation with coronavirus cases, I’d like to stay on the sidelines. The work-from-home narrative should be a catalyst but it’s not quite convincing yet.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.