We’ve seen another Wall Street darling effectively bite the dust. DraftKings (NASDAQ:DKNG) has declined 45% from its Oct. 2 high to its Nov. 1 low. Amid that slide, DraftKings stock declined in 16 out of 21 trading sessions. For bulls, it has not been an easy ride.

This stock has been obliterated, but should it have been?

On Oct. 5, DraftKings announced that it would raise almost $1 billion in cash. It also announced a record quarter with its preliminary results. The company sold 32 million shares, 16 million of which were in a secondary offering and 16 million of which were from various insiders.

However, I think the stock is being unfairly punished. More than half of the insider sales came from Shalom McKenzie, the former owner of SBTech, which merged with DraftKings before the combined entity went public under the latter’s name.

Aside from a large chunk of the sellers being from the initial tie-up deal, DraftKings raising $960 million is a positive, not a negative. Let’s not forget we’re still in the novel coronavirus pandemic. Should the sports world go back offline, DraftKings will need enough cash to hold itself over until better days.

Let’s look at a few reminders of the positives.

The Positives for DraftKings Stock

Over the last month, the rhetoric has shifted firmly into the negative for DraftKings stock, even though there are still plenty of positives.

The Big Ten and PAC 12 returned to action. The NBA, NHL and MLB finished their seasons. Despite some turbulence with the novel coronavirus, the NFL continues to forge through its season in relatively smooth manner.

In other words, the sports world proved that it can handle operations within the Covid-19 world. Perhaps that will change if cases continue to spike, but for now, DraftKings should avoid an environment like late Q1 and early Q2 2020.

Let’s also not forget about the company’s exclusive deal with the New York Giants. Or that DraftKings opened to the first betting shop in a U.S. arena. The D.C. arena is home to the NBA’s Wizards, NHL’s Capitals and WNBA’s Mystics.

While not the main driver of business, this brick-and-mortar approach could be a solid business plan down the road — particularly when fan traffic picks back up.

What else? Let’s not forget that DraftKings got Michael Jordan involved as a special advisor to the board and as an investor. Also, the company inked an exclusive content deal with the king of sports, ESPN.

Those are two big catalysts, in my opinion, but it doesn’t stop there. The election is proving to be a catalyst for furthering the legalization of sports betting.

Bottom Line on DKNG

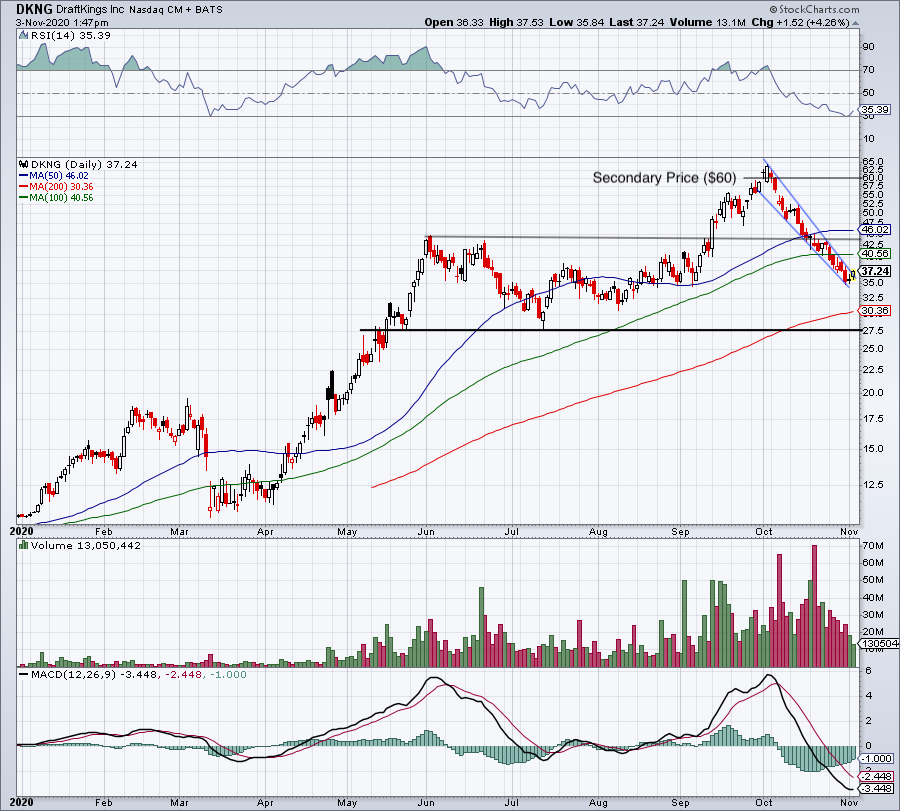

Click to Enlarge

When DraftKings last reported earnings, it had more than $1.2 billion in cash and no debt. Earlier in the year, it noted that its monthly cash burn would only be in the $15 million to $20 million range without major sports action.

Add the additional cash from the most recent raise and DraftKings balance sheet is in very solid shape. There should be no concern over the company’s liquidity at this stage.

While consensus estimates are decisively bullish – calling for 46% revenue growth in 2021 to $770 million – it’s the long-term growth investors are after. From a recent InvestorPlace article:

Macquarie analyst Chad Beynon ‘believes that by 2025, 96 percent of the US population will have access to legal OSB.’

He also argues that, ‘the US internet casinos and sports wagering markets will be worth a combined $33.7 billion in 2030, up from just $1.4 billion last year,” and sees DraftKings “posting revenue of $535 million this year and topping $1 billion in 2022 before ascending to $4.3 billion in 2030.’

A look at the charts shows a steep decline from the $60s down to $35. It’s definitely possible we see further weakness in DraftKings stock. In that case, look for a dip down to the 200-day moving average and potentially the $27.50 area.

On the upside, look for shares to break out of this falling wedge look (blue lines). A break higher puts the 100-day moving average in play, followed by the May high and breakout level from September near $43. Above the 50-day moving average and DraftKings stock can really fly higher.

On the date of publication, Bret Kenwell held a long position in DKNG.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell.