In years past, the narrative for Apple (NASDAQ:AAPL) was an easy one. Thanks to its compelling consumer brand and cohesive ecosystem, only a fool would be skeptical about Apple – and believe me, I’ve had my share of looking quite foolish on the relevance and resilience of the consumer electronics giant. But nothing lasts forever and there are deeper concerns that the company is losing its charm.

Primarily, Apple’s iconic iPhone just isn’t the license to print money as it once was. Since the beginning of 2018, the smartphone brand that started it all has represented a lesser share of the company’s total global revenue. For instance, in its fiscal first quarter of 2018, the iPhone represented nearly 70% of all sales. In Q4 2020, that share fell to a startling 40.9%.

Further, it’s no longer a remarkable proposition that Apple products are losing their luster relative to the competition. Back during the era when the iPhone was a few years removed from its debut, you could easily tell the difference between Apple’s flagship product and its rivals. Now, as Techradar.com said in its comparison between Apple and Samsung smartphones, there’s not much that separates them.

Both feature similar-looking sleek designs. As well, the competing products have emphasized high-quality camera optics to the point where you’d really have to be a true connoisseur of the digital arts to appreciate their individual nuances.

Just as importantly, Alphabet’s (NASDAQ:GOOG, NASDAQ:GOOGL) Google has invested countless hours developing its Android operating system. Today, unless you’re an operating systems snob, most users will be happy operating in either ecosystem.

And as a blog post on Ipitaka.com points out, while the Apple ecosystem is great, it can sometimes stink. From more expensive products and services to proprietary charging methods, being in this ecosystem comes at a cost. As the competition tightens, it’s becoming harder for consumers to justify the added cash outlays, helping to explain the iPhone’s sales deterioration.

Could Services Help Save AAPL Stock?

But just like outgoing President Donald Trump, you don’t want to count out AAPL until it’s truly over. Forbes contributor Dan Runkevicius makes an excellent argument: Apple is perhaps the most misunderstood company

. Specifically, the markets getting spooked over declining iPhone sales is overkill.

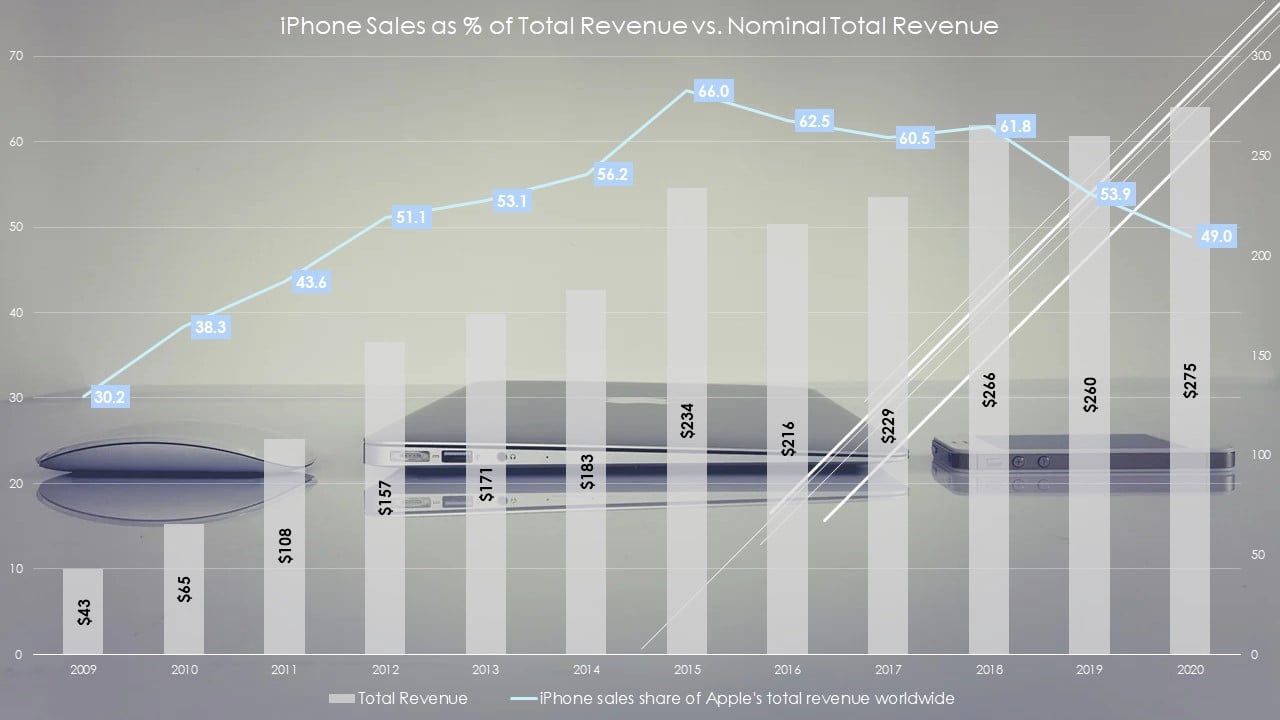

To be fair, many of those that hit the exits are likely basing their assessment on the fundamentals. Between fiscal year 2009 through 2014, total revenue at Apple increased at nearly a 34% compound annual growth rate. From 2015 through 2020, though, total revenue dropped to a startlingly low CAGR of 3.3%.

Click to Enlarge

What happened? Well, it’s easy to blame the iPhone. In 2009, iPhone sales as a percentage of total sales averaged 30.2%. In 2014, the average was 56%. One year later, this metric hit a peak of 66%. Since then, the share has declined to just under 49% in 2020.

Nevertheless, Runkevicius argues that the cycle of phone upgrades has been extended. This translates to people keeping their phones longer, accruing more service-related charges. “In other words, there are more active iPhones out there than ever before. That should be a hell of a symphony to Apple investors’ ears. Because Apple earns way more from its old phones than it does selling new ones.”

On one end, it’s a compelling thesis because Apple sells pricey warranty and insurance services, with some packages coming out to one-fourth the cost of the target device. Further, the bills that one pays with their iPhone goes partially to Apple’s pockets. As well, you have myriad services and platforms, such as iCloud, Apple Music and Apple TV.

Still, I don’t think it’s wise for investors to completely ignore phone and device sales. While service-based revenue represented 22.5% of total sales in Q4 2020, the iPhone still brings home the bacon at 40.9% total revenue share, as I mentioned near the top. Services is intriguing no doubt but it’s still got a long way to go.

Tantalizing Technical Setup

While the debate over Apple’s fundamentals rage on, the technical chart presents a tempting setup. After a robust rally between this year’s March doldrums to the beginning of September, AAPL entered a consolidation phase.

Based on my interpretation, Apple is charting a bullish pennant formation, with trendline resistance and trendline support spiraling tighter into an apex. At that point, we could see a breakout move to the upside.

It’s a similar pattern to what I saw with DraftKings (NASDAQ:DKNG) back in August. Though the fundamentals didn’t appear favorable due to the threat of a second wave that we’re seeing right now, DKNG nevertheless jumped higher, allowing speculators to capture nearer-term profits.

I see the same thing happened with AAPL, which theoretically makes it a buy despite shares being incredibly overvalued. Still, if you’re going to gamble, watch this like a hawk. As with DKNG, when investors started paying attention to the fundamentals, shares dropped like a rock.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.