In early October, I covered cloud computing services and content delivery network (CDN) specialist Fastly (NYSE:FSLY). At the time, I mentioned that White House health advisor Dr. Anthony Fauci held the key to the direction of Fastly stock. Basically, if everyone took the pandemic seriously — and thereby contained the spread — that would accelerate a return to normal. And that wouldn’t be too great for FSLY.

In my article, I also noted that Fastly stock had a 78.5% correlation coefficient with new daily novel coronavirus cases in the United States. I explained, “In other words, as Covid cases increase, so too does the market value of Fastly and vice versa. And that’s why I say that FSLY’s trajectory depends on Dr. Fauci.”

Back then, the seven-day moving average was about 43,000 cases. It seemed that, whether people were taking matters seriously or if the virus was running out of steam, we were finally rounding the corner. And if that was the case, the need for CDN and cloud services could decline as people returned to offices and consolidated that demand.

Unfortunately, though, Covid-19 cases have now climbed at an absolutely bonkers rate. On Nov. 6, new daily infections almost hit 133,000 cases. That contributed to a seven-day moving average of nearly 99,000 cases at the time. This disconcerting surge prompted top White House novel coronavirus advisor Dr. Deborah Birx to push for “an aggressive balanced approach.”

But — is this a cynically fortunate development for Fastly stock? Judging from the correlation between rising cases and the stock’s upward movement, it seems like you should be rooting for Covid-19 — if, of course, you had zero empathy.

However, the narrative is much more complicated than that.

The Bullish Case for Fastly Stock

On the surface, the bullish pandemic argument for the company seems reasonable. For one, this isn’t a spurious correlation, like the “relationship” between increased drownings and ice cream sales.

There’s no doubt Covid-19’s disruptiveness increased demand for CDNs. Many employees have been sent home to work, sucking bandwidth across a wider surface area. Additionally, people have been consuming more media from streaming platforms like Netflix (NASDAQ:NFLX). By this thinking, it seems obvious then that more infections bolster the case for Fastly stock.

Even hard-hit cities like New York have substantial incentives to implement harsh mitigation protocols to stem the tide

. Yes, these actions are draconian and economically disruptive. But for city and state government administrators, they’re caught between a rock and a hard place. In fact, about the only business that can benefit in this circumstance are CDN and cloud computing services. So Fastly appears to have upside, right?

There’s one problem: the correlation between the stock’s price tag and novel coronavirus cases has now gone the opposite direction.

A Key Relationship Breaks Down

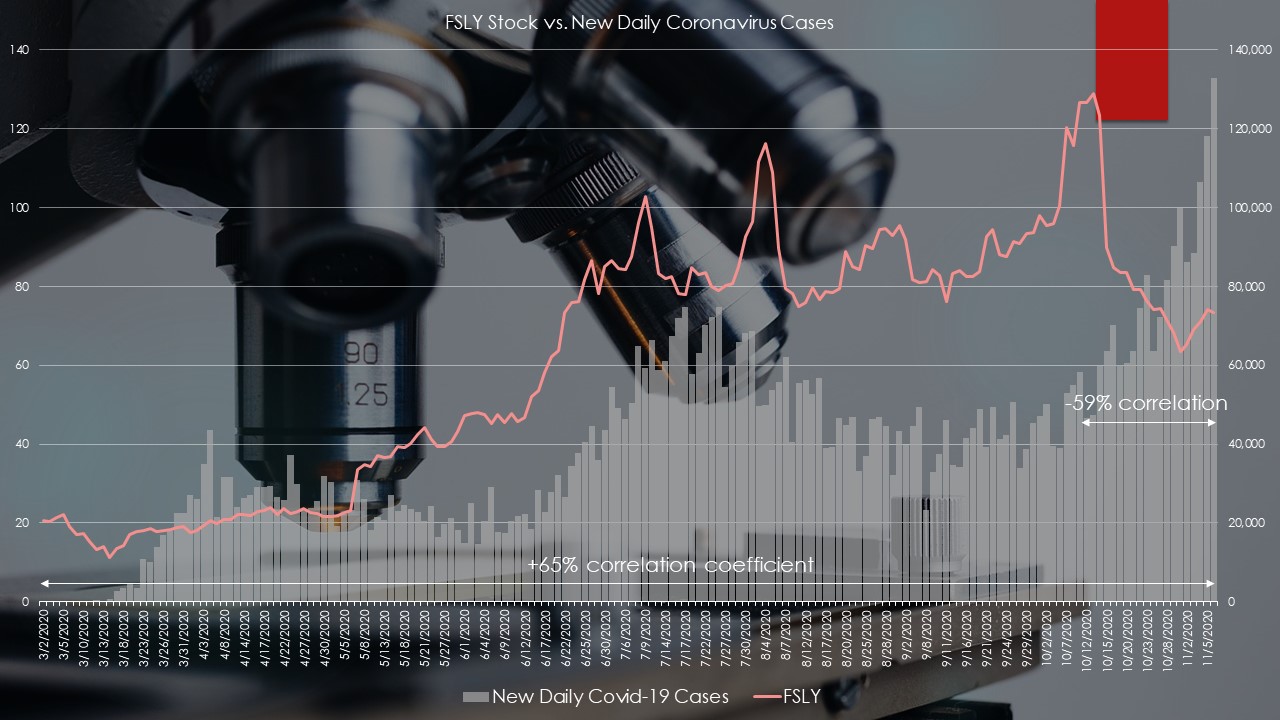

Click to Enlarge

From the beginning of March through Nov. 6, the correlation coefficient between the two metrics dropped from the aforementioned 78.5% to 65%. The biggest contributor for the decline has been the correlation from Oct. 13 through Nov. 6, which was -59%. Essentially, the correlation is now an inverse one. It now seems that as Covid-19 cases rise, Fastly stock deteriorates.

Of course, the negative catalyst here is the company’s disappointing third-quarter earnings report. As InvestorPlace contributor Chris Tyler notes, management warned stakeholders that Q3 sales would come in lighter than expected. Tyler writes, “Bottom-line, being mired in consistent red ink and negative cash flow is never healthy. And Fastly has been so for more than a couple years.”

Put another way, investors may recognize that the outside fundamentals are positive for Fastly. But the “inside” fundamentals matter, too. And both prospective buyers and current shareholders may be worried that Fastly isn’t making good use of its opportunity in the pandemic.

Time to Rethink FSLY

In both of my single-stock stories regarding FSLY, I indicated that it’s better to consider trading shares on volatility rather than as a directional play. Basically, with multiple variables at work, it was too difficult to know which way Fastly would go next. Rather, the only real certainty was that it would get there in a wildly accelerated manner.

Now, however, this assumption might change. In Q3, Fastly generated about $71 million in revenue, which was an increase of nearly 42% year-over-year (YOY). But this isn’t that impressive considering that between Q3 of 2019 and 2018, the YOY growth was 35%. Surely the growth should be much higher, considering the company enjoyed an unprecedented tailwind in 2020.

Moreover, analysts forecasted that Q3 2020 revenue would come in between $70 million to $74.7 million. Actual top-line sales were very close to the bottom end of that estimate range. This signals that Fastly wasn’t making good enough use of its circumstances.

Or, it could point to rising competition in the cloud services and CDN space. And that makes the recent inverse correlation between Fastly stock and the pandemic very significant. It confirms that — for whatever reason — the company can’t generate as much momentum as its peers. Therefore, this time around, I believe there’s a directional risk to the downside.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.