It seems that for the past several weeks, the news has been dominated by questions surrounding the Covid-19 vaccine candidates: Which company’s candidate will be approved first? Is subunit or nucleic-acid-based better? When will everyone have access? For prospective buyers of Carnival (NYSE:CCL), I’m afraid the answers to these questions don’t really matter. Regardless of a vaccine, investors should avoid CCL stock.

It’s true that the main catalyst for CCL stock is the success of President Donald Trump’s Operation Warp Speed. But so many other factors will come into play once we have an effective vaccine. To start, will people even get vaccinated once it’s approved?

Obviously, the answer is that at least a good portion of the U.S. population would likely oppose mandatory vaccination like they would oppose giving conquered territory back to Mexico. To be fair, I don’t blame the anti-vaxxers. Yes, the Democrats and the mainstream media make fun of them. But you know what? Trampling on people’s right to do what they want with their bodies — sound familiar, anyone? — is a slippery slope.

And what should genuinely concern those holding CCL stock in the near term is that the news event that catalyzed share prices can also quickly become a liability. Yes, it’s encouraging that Pfizer (NYSE:PFE), Moderna (NASDAQ:MRNA) and possibly Novavax (NASDAQ:NVAX) are prime vaccine candidates in the battle against the novel coronavirus. But can we be brutally honest with each other? This is what I call a “paper” encouragement.

From one consumer survey, 77% of Americans read food labels, and that makes sense. People want to know what they’re putting in their body. If a similar percentage of people are skeptical about the vaccine, many millions could potentially refuse Pfizer’s and Moderna’s nucleic-acid-based vaccines, as they are experimental approaches. Further, if forced to vaccinate, I think most will opt for Novavax’s subunit vaccine, which is a proven platform.

Unfortunately, the process of making subunit vaccines is lengthy and complicated relative to RNA-based vaccines. That’s a strike against subunits and, by logical deduction, CCL stock. After all, the Carnival doesn’t just need vaccines. They need a situation where most people are comfortable taking them.

CCL Stock May Be Facing a Calm Before the Storm

While you might regard the above as me being a negative Nancy, please note that I don’t mind speculation. For instance, I’m bullish on cryptocurrencies

, and there are few markets as volatile. It’s just that I prefer sectors where I’m confident in the long-term trajectory.

As you can guess, I don’t have that confidence for CCL stock and the cruise liners. Not only will millions not want to be vaccinated, the process itself will likely be cumbersome. RNA and subunit vaccines will likely require two injections to be effective, posing logistical challenges. Further, storage requirements may prevent some solutions from being appropriate for infrastructurally compromised regions.

But even if we had a convenient, proven, single-dose Covid-19 vaccine, I would still be hesitant of buying CCL stock. Sure, the market is at record highs, but also rising are suicidal ideations and mental health problems. I’m sorry, but the sudden correlation of these two metrics don’t make a lick of sense.

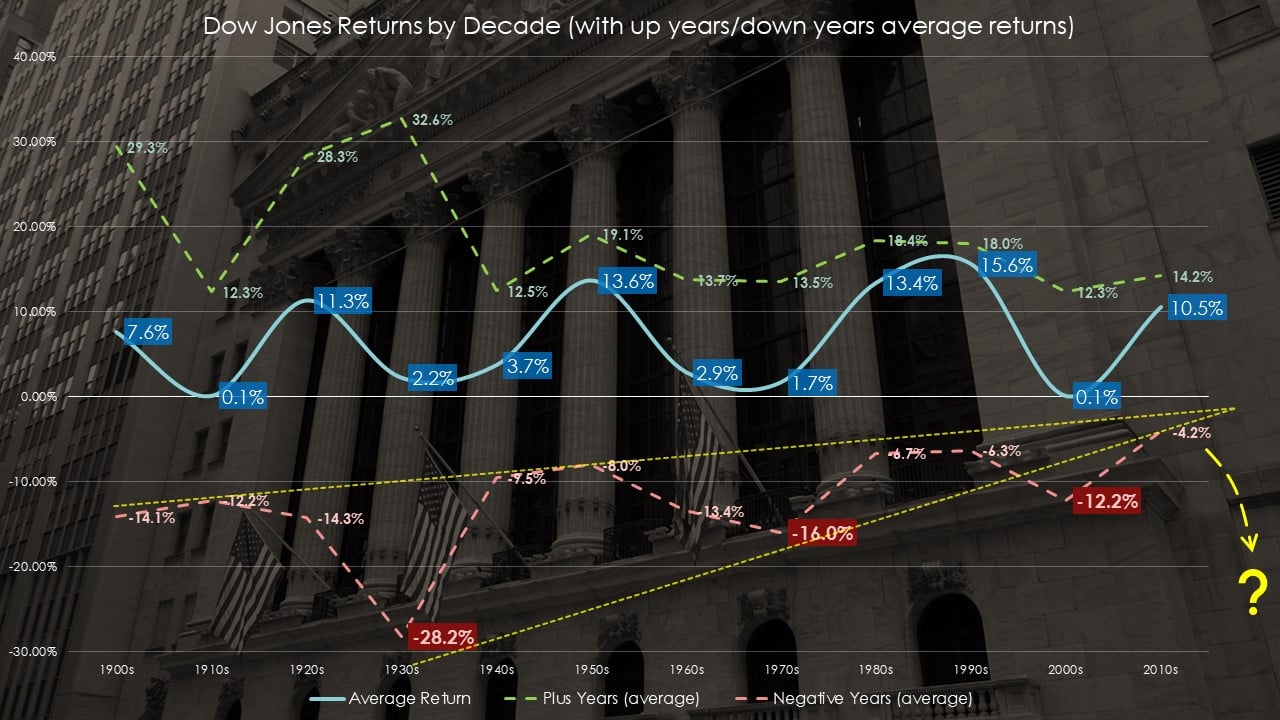

Adding to this broader concern is the cyclical nature of the stock market — specifically, that we may be on the wrong end of the cycle. Since the 1980s, we’ve seen three decades of double-digit returns in the Dow Jones, with only one decade falling outside this boundary. Frankly, this is an unprecedented circumstance, which begs the question: Are we facing a potentially severe corrective event?

Click to Enlarge

Personally, I believe caution is warranted. It’s not just that we’re enjoying decades of bullishness without many bear phases to bring us to equilibrium. Rather, it’s that the average returns by decade are progressively closer to the average of bullish years. Moreover, the average of bearish years is progressively becoming less bearish.

Call me crazy — and I know some of you do! — but I see a rising wedge pattern developing in the average returns by decade for negative years. If you’re familiar with technical analysis, you’ll know that rising wedges have bearish implications.

Further, rising wedges often occur at the tail end of a rally. Basically, they signal an exhaustion of the bulls to keep pushing the target asset higher. Therefore, if the broader market is forecasting trouble, I’m not sure if CCL stock can withstand the incoming waves.

Take Some Profits Off the Table

Certainly, if you gambled on CCL stock before its recent run up, you should be congratulated for your intrepidness. But now would be the time to think intelligently. Unless you see a substantive improvement in Covid-19 cases, along with a true pathway toward economic recovery, the cruise-ship industry is trouble with a capital “T.”

All you have to do is look at recent stock market performances to be uncomfortable. In the 1980s, the Dow averaged a return of 13.4%, with positive years averaging 18.4% and negative years averaging -6.7%. In the 1990s, the average was 15.6%, with a positive average of 18% and a negative average of -6.3%.

Last decade? We averaged 10.5%, with the ceiling at 14.2% and the floor at a remarkably high -4.2%. But I’m not sure how long this collective optimism can last without incurring a correction.

Again, you see the evidence of a strange dichotomy at work. The Wall Street fat cats are raking in the dough, while those on Main Street are losing their homes, their businesses and, in some cases, their lives. Put simply, this is not a healthy, credible environment for CCL stock.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.