Wary investors will continue to characterize the rising stock market as a bubble ready to pop. That is wholly untrue, to some extent. A stock sector bubble is a better characterization, in light of recent market pops and drops. In January, GameStop’s (NYSE:GME) peak to $483 created a once-in-a-lifetime lift that caught short-sellers completely off guard. One hedge fund may have lost billions at that moment. Since then, the stock fell and both the buyers and short-sellers moved on.

After GameStop’s rise and fall, stocks in the silver mining business rose and then fell sharply a day or two later. Last week, the intense buying in cannabis stocks sent those already with a large capitalization to multi-year highs.

You may guess what happened next.

By the end of last week, the pump faded. Sellers lined up sell orders the very next day, sending the stocks crashing lower. Seven marijuana stocks could go down in flames. Investors should recognize the proverbial pump-and-dump schemes that plague the market today.

The seven stocks to avoid are

- Tilray (NASDAQ:TLRY)

- Aphria (NASDAQ:APHA)

- HEXO (NYSE:HEXO)

- Aurora Cannabis (NYSE:ACB)

- Canopy Growth (NASDAQ:CGC)

- Cronos Group (NASDAQ:CRON)

- Sundial Growers (NASDAQ:SNDL)

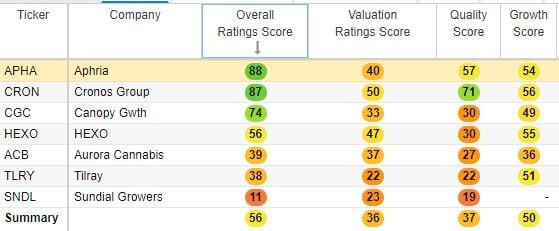

In the chart below, the overall ratings vary from a low of 11 to a high of 88 (pardon the pun). None of the stocks have a good value score.

Marijuana stocks scored by value, growth, and overall

Tilray (TLRY)

In December, Aphria and Tilray announced a merger that will create a $4 billion market capitalization cannabis firm. The deal involves no cash. APHA shareholders will get 0.8381 shares of Tilray for each Aphria to each share owned. When completed, Aphriria will own 62% of the combined firm.

The merger is critical to the survival of both firms. It will save the firms 100 million CAD ($79 million) in pre-tax annual cost synergies. With competition heating up due to years of excess production, Tilray may have a chance of survival.

On Feb. 9, Tilray announced an agreement with Grow Pharma to import and distribute medical cannabis in the U.K. This market is still very small. Investors who paid up to $67 for TLRY stock, at an $8 billion market cap, will end up regretting it. In the third quarter, Tilray posted a net loss of $2.3 million. Revenue was flat year-on-year at $51.4 million.

Expect unexpected integration costs hurting the combined TLRY-APHA firm after the deal closes.

Aphria (APHA)

Aphria traded as high as almost $27 at its peak on Feb. 10 before slumping. In Q2 2021, the company beat expectations as revenue grew. It lost money again in the period.

Aphria posted GAAP earnings losses of 42 Canadian cents per share. Revenue topped 160.53 million CAD. On closer inspections, investors should notice the adjusted cannabis gross margins slumping to 45.9%, down from 56.6% last year. Its beverage alcohol gross margin added just 533,000 CAD in the quarter.

The drop in the average retail selling price (ASP) of medical cannabis is a concern, too. ASP fell to $6.96 a gram, down from $7.38 in the prior quarter. Aphria blamed specific pricing pressures it offered to assist patients in need. Promotional programs also hurt prices. Looking ahead, the negative pressures from the Covid-19 pandemic hurting sales may end. Assuming that the vaccine protects people and the shutdown ends, sales could improve.

Since it is another marijuana stock that loses money quarterly, investors should avoid APHA stock.

HEXO (HEXO)

The decline in HEXO stock’s price reached a point where the company announced a reverse split of shares on Dec. 18, 2020. So, for every four shares owned, investors get one new share. At the time, the stock traded at below $5. To avoid the danger of falling to a stock price below the minimum, management proactively consolidated shares.

Speculators who do not recognize the lack of value a consolidation announcement signifies will lose money. HEXO stock has a good chance of continuing its drop after the temporary spike in recent weeks. In the first quarter, the company posted an 8% growth in adult-use cannabis sales. Adult-use beverage sales grew by 54%.

The weak sequential growth in revenue and the inability to reduce the cost of sales should concern shareholders. One bright spot is that gross margin improved to 35% from 30% in Q4 2020.

Hexo is not a buy at current levels. Wait for the sell-off to end before considering this speculation again.

Aurora Cannabis (ACB)

Aurora Cannabis offered its shareholders faint hope when it posted second-quarter results. Revenue from medical cannabis rose by 42% year on year to 38.9 million CAD. An impressive 562% increase in high margin international medical sales lifted results.

The company lost money again in the quarter. It posted an EBITDA loss of 12.1 million CAD. This is better than the 53.1 million CAD loss YoY. The company ended the quarter with 565 million CAD in cash.

To lower its negative cash burn rates, Aurora lowered its production levels at Aurora Sky. This lifted its cash cost of sales, thanks to the under-utilization of capacity. In the long-run, Aurora cannot keep booking restructuring costs and running below capacity. It needs to aggressively grow sales to widen its market share.

This is easier said than done. The U.S. may legalize cannabis but U.S. multi-state operators will benefit first.

Avoid ACB stock.

Canopy Growth (CGC)

The first half of Canopy Growth’s Q3 earnings results presentation did not include financials. Instead, the company touted its product innovations. For example, the National Animal Supplement Council granted Canopy Animal Health its quality seal.

Canopy listed its three-year financial targets somewhere in the middle of the presentation posted here on slide 12. It aims to grow net revenue by 40-50% CAGR. Adjusted EBITDA will not turn positive until next year, in the second half of 2022. Operating cash flow will not be positive for the full year in FY 2023. It will take another three years (FY 2024) when the company achieves positive free cash flow.

CGC stock is only for investors with a time frame of at least three years. Anyone speculating on the stock with a shorter holding period will end up disappointed.

On Wall Street, 14 of 19 analysts have a “hold” rating on the stock.

Cronos Group (CRON)

Cronos Group stock benefited from the recent volatility in marijuana stocks. The lift may prove temporary as markets eventually value stocks on fundamentals.

In the third quarter, Cronos posted operating losses of $40.2 million. If revenue nearly doubled from $5.78 million to $11.36 million, why is it still losing money? The company benefited from an increase in net revenue and the gross profit contribution of its U.S. business. But the cost of sales grew because of higher volumes in adult-use sales and purchased flower. Wholesale sales fell.

The mixed revenue results suggest that Cronos needs to expand its U.S. presence. Speculators are betting that cannabis legalization will put an end to Cronos’ quarterly losses.

Among 13 analysts, eight recommend investors “hold” while three rate CRON stock as a “sell.” SimplyWall.st is surprisingly bullish. The site figured a strong positive future cash flow would justify a fair value of around $22.

Sundial Growers (SNDL)

After long trading at less than a dollar, Sundial Growers stock touched almost $4 recently. The company’s second-quarter results showed no strength.

In that period, the Canadian LP said it was proud to post quarterly revenue of above 20 million CAD. CEO Zach George said, “We have made good progress in streamlining our business over the past six months, having eliminated non-core initiatives, reduced costs, and improved operating efficiencies.”

Sundial is counting on new product offerings and a strong reputation as a high-quality cannabis producer. Speculators could bet that this succeeds in differentiating the firm against the many competitors. If history repeats itself, Aurora, Cronos, and Canopy all promised new products ahead. When that day arrived, operating margins did not improve enough.

Sundial’s strong drop will leave many speculators facing a loss. If the stock rebounds again, those past buyers will sell the stock on the way up to break-even.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Chris Lau is a contributing author for InvestorPlace.com and numerous other financial sites. Chris has over 20 years of investing experience in the stock market and runs the Do-It-Yourself Value Investing Marketplace on Seeking Alpha. He shares his stock picks so readers get original insight that helps improve investment returns.