ArcLight Clean Transition Corp. (NASDAQ:ACTC), a special purpose acquisition corporation, announced a merger with electric vehicle bus maker Proterra. Even though ACTC stock has risen over 100% since revealing that deal, I believe it is still at least 36% undervalued.

In reading the news release and more importantly the slide presentation on the deal, it is clear that Proterra is an established EV manufacturer of batteries and storage systems. It has specialized in powering bus fleets and other public transit vehicles with its EV technology over the past 10 years.

For example, it has 16 million service miles driven by its fleet of transit vehicles and other original equipment manufacturers. Some of these OEMs are Freightliner Custom Chassis Corporation, Thomas Built Buses, Van Hool, Bustech, and Optimal-EV. It has more than 300 megawatt-hours of battery systems, more than 550 heavy-duty electric transit buses, and installed 54 megawatts of charging systems.

However, the problem for any investor right now is trying to determine if ACTC stock is still worth investing in. Is ACTC stock still undervalued? I believe it is by at least 36%, and the rest of this article will show why.

Valuing ACTC / Proterra

ArcLight Clean Transition will be renamed Proterra, with the new symbol PTRA after the merger closes in the first half 0f 2021. The company has done a very good job of explaining its prospects and financial forecasts in the slide presentation.

ACTC stock now has pro format market capitalization of $5.988 billion at today’s price of $24.94. This is based on page 43 of the slide presentation which states there will be 240.1 million shares outstanding after the merger closes.

Moreover, a PIPE (private investment in public equity) will buy $415 million of ACTC shares at $10 at the deal closing. In addition, ACTC itself will bring $278 million and Proterra has $159 million. Therefore, there will be $852 million in total cash at the deal’s close. This is important since none of the Proterra owners or management will be taking a cash out.

Therefore, the implied pro format enterprise value is $5.136 billion. How does this compare with forecast sales and earnings? The company is very helpful in providing estimates.

Click to Enlarge

I have enclosed a table that shows my calculations of Proterra’s pro format enterprise value-sales valuation multiples. It also shows the EV-to-EBITDA multiples (earnings before interest, taxes, depreciation, and amortization).

As I say this is very helpful. Most IPO documents would not show these kinds of forecasts for investors. The bottom line is that ACTC stock / Proterra trades for 11.7x EV/sales for 2022 and 15x using a present value adjustment.

Comp Valuation for ACTC Stock

What we need to do now is compare these multiples to its peers, such as Plug Power (NASDAQ:

PLUG), Ballard Power Systems (NASDAQ:BLDP), Workhorse (NASDAQ:WKHS), Tesla (NASDAQ:TSLA), Nio (NYSE:NIO) and a number of foreign companies.

Proterra provides comparisons on pages 45 and 46 of the presentation. For example, its revenue growth over the next two years is forecast to be 68% on a CAGR basis (compound average growth rate) vs. 37% for its peers. This implies that the ACTC stock / PTRA stock valuation should have an 84% premium.

The average EV-sales ratio of its peers is 10.3x for 2022. ACTV has a multiple of 11.7x and 15.5 times (adjusted for present value).

Click to Enlarge

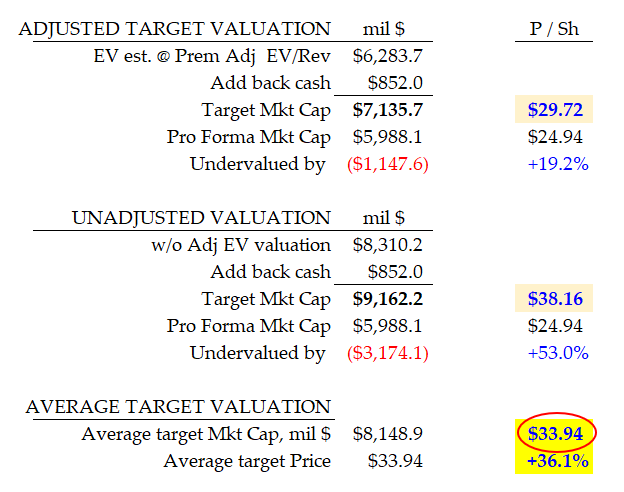

However, if we multiply Proterra’s 83.8% premium by the market average of 10.3, the target EV multiple to sales should be 18.9x. This implies that ACTV/PTRA stock is still worth much more. The adjusted (for present value) target value works out to $29.72 per share.

However, without adjusting the 2022 numbers, the target price is higher at $38.16. Therefore, the average of these two is $33.94, which is 36% higher than today’s price of $24.94.

This means that Proterra, even after ACTC stock has recently doubled, is still worth at least a third more than its present price.

On the date of publication, Mark R. Hake holds a long position in Tesla (TSLA) stock.

Mark Hake writes about personal finance on mrhake.medium.com and runs the Total Yield Value Guide which you can review here.