Whenever a the market takes a dip, it allows value investors to discover stock bargains.

There are plenty of reasons for a stock to be widely sold, so buying discarded stocks is not risk-free. Markets likely sold the stock for a reason.

The company may have issued a weak quarterly earnings report, shared bad news or merely fallen out of favor. After growth investing performed well compared to value investing, readers need to keep asking why a stock is on sale.

If the company’s business model is not broken, investors may decide if the stock’s discount is big enough to offset risk. More importantly, a company facing headwinds ahead will need more than one quarter to revive its prospects. Investors need to be compensated for the risk of betting that the company will turn around.

Seven companies plunged in recent months are those that readers should consider. Listed in alphabetical order, these stack bargains might well be worth that risk.

- AMC Networks (NASDAQ:AMCX)

- Chewy (NYSE:CHWY)

- CRISPR Therapeutics (NASDAQ:CRSP)

- Garmin (NYSE:GRMN)

- Medtronic (NYSE:MDT)

- Pinterest (NYSE:PINS)

- Teladoc Health (NYSE:TDOC)

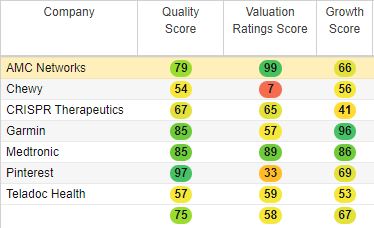

In the table from data supplied by StockRover.com, the average quality score is 75/100.

Click to Enlarge

This strong score suggests that investors are impatiently selling companies that offer a strong return on investment.

For example, Garmin, Medtronic, and Pinterest have the highest quality scores on the list. AMC Networks and Medtronic offer deep value.

Chewy and Teledoc have fair scores. That does not mean their stock will stay at lows forever.

Stock Bargains: AMC Networks (AMCX)

The pandemic in the last year created an unsustainable growth rate for streaming firms. In the third quarter, AMC Networks posted strong momentum. The markets ignored the results.

In Q3, the company posted revenue growing by 24% year-over-year to $810.77 million. Non-GAAP earnings per share topped $2.68.

The multinational basic cable television channel keeps attracting subscribers. With streaming products AMC+, Acorn TV, Shudder, Sundance Now and ALLBLK, AMC Networks will reach nine million paid subscribers.

The company’s long-term strategy for profitability is monetizing its intellectual property and high-quality content and leveraging its strong legacy channels business.

Investors are wary of the cable business. AT&T (NYSE:T) owns HBO Max but shares fell. ViacomCBS (NASDAQ:VIAC) peaked at $101.97 in March 2021. The stock faded for months, breaking down after failing to hold the $40.00 level.

AMCX stock will report strong growth as its engagements through marketing and promotions pay off in the coming years. AMC+ is still in the early phases of growth. It only launched the service last year.

Chewy (CHWY)

In September, Chewy posted Q2 net sales of $2.16 billion, up 26.8% from last year. It lost $16.7 million, due partly to a $25.6 million share-based compensation. Shares started slipping after that report.

In the September quarter, net active customers rose by 21%. Speculation that churn rates are rising hurt investor confidence. The cost of attracting new customers may rise.

In the third quarter, Chewy discussed its higher costs in detail. It faced port congestion and higher container rates. This led to a three-fold increase in inflation on spot rates compared to Q1 costs.

Chewy ramped up production ahead of the holiday season. This raised costs for the period. Revenue grew by 24.2% year-over-year to $2.21 billion, but it lost 8 cents a share on a GAAP EPS basis.

Chewy benefited from distortions in demand during the pandemic. As the lockdown eased, bears speculate that Chewy’s business momentum may, too.

Fortunately, people need to spend any amount on their pets. The under-performance in CHWY creates a buying opportunity for investors. Expect very strong sales during the holiday quarter. That will set up a stock rebound in the next month.

Stock Bargains: CRISPR Therapeutics (CRSP)

Gene editing firm CRISPR is best known for its VCTX210 trial for an allogeneic, gene-edited, immune-evasive, stem cell-derived therapy for the treatment of type 1 diabetes (T1D).

After Health Canada approved its clinical trial application, investors may consider CRSP stock as it reports positive results from the study.

CRISPR has a broad portfolio besides a therapy for treating sickle cell disease and beta-thalassemia. It has a next-generation immune-oncology platform. The therapies are CTX110, CTX120 and CTX130.

Regenerative medicine is promising. Impatient market participants sold the stock instead of waiting for the company to prove its prospects will play out. If it works, patients do not need to depend on organ donors. Instead, CRISPR engineering will give scientists the ability to mass-produce organs.

CRISPR said that it is working with its partner Vertex Pharmaceuticals on meeting regulatory requirements for CTX001 treatment. Once it meets all regulatory requirements, it will apply for regulatory approval of the drug. This is a catalyst that may send CRSP stock back to previous highs.

Garmin (GRMN)

Garmin shares peaked at around $175 in the summer, it trades below $140 today. The company posted strong Q3 results but disappointed investors with a disappointing outlook.

Garmin posted revenue of $1.19 billion, up 8.2% year-on-year. Operating income fell by 11% year-over-year to $283 million. Higher freight costs hurt margins. Looking ahead, lead times on equipment are getting longer. That will hurt fourth-quarter revenue.

To counter-balance shipment delays and higher costs, Garmin is increasing its inventory levels. It may meet demand levels, at the risk of holding extra supply.

In 2022, Garmin expects higher capital expenditure. Fortunately, consumer demand for fitness and outdoor-related products is still strong. During the pandemic cycle, Garmin did not face any weakness in the wearables market.

The company is differentiating itself from the active lifestyle theme. With promotional activity, Garmin has a good chance of increasing its market share. Still, COO Cliff Pemble is conservative. He is only expecting normal, seasonal demand. This positions Garmin to beat expectations in the next quarter.

Stock Bargains: Medtronic (MDT)

Medtronic’s uptrend broke in late summer. MDT stock formed a downtrend and selling momentum accelerated in recent weeks. On Dec. 15, the medical devices firm disclosed a Food and Drug Administration warning letter.

The FDA said that after an inspection of its diabetes business that concluded in July, it identified inadequacy in quality. At the Northridge facility, MDT had “inadequacy of specific medical device quality system requirements.”

To address the issues, Medtronic will hire external experts and add resources. Corrective actions and process improvements should satisfy the FDA’s concerns.

The diabetes division is a small contributor to the business. Medtronic expects revenue to fall in the low single-digit percentage.

In the third quarter, Medtronic posted top-line growth of 3% year-over-year to $7.8 billion. It earned 97 cents a share. It forecasted revenue to grow by 7% to 8% for the fiscal year 2022. This is below its prior expectation of 9%. Markets punished the stock by around $100 last week.

Most analysts have a bullish rating on Medtronic, with an average price target of $136 (per Tipranks).

Pinterest (PINS)

Social networking site Pinterest is growing at a steady pace. In the third quarter, revenue grew by 43% year-over-year to $632.93 million. Markets are still concerned about user metrics.

Monthly active users grew by only 1% year-over-year to 444 million. In the fourth quarter, Pinterest expects revenue will grow in the high teens percentage year-over-year. Still, operating expenses will grow.

In its growth phase, Pinterest needs to invest in the business. This includes creating a native content/Creator ecosystem. It also must spend on brand marketing.

Cautious investors are overlooking the 43% growth rate. Instead, user growth may cool, pressuring Pinterest to increase marketing and research and development efforts. This will add to losses in the coming year.

Investors will realize that Pinterest needs to sustain strong user growth first. Profits will come later. As users seek alternatives to the current social networking sites, Pinterest will attract buyers again.

Teladoc Health (TDOC)

The resurgence in the omicron variant will necessitate Telemedicine. Short-sellers are circling Teledoc stock with a short float of 15%.

Investors cannot predict how severely governments will lock down businesses. Teledoc’s outlook is unchanged in its absence. The company expected revenue for 2021 in the range of $2.015 billion to $2.025 billion. The virtual care leader will reach revenue of over $4 billion by 2024.

TDOC stock is out of favor because revenue growth alone will not justify a higher share price. The company needs to show investors that its Livongo acquisition will add meaningfully to profits.

The company is a long-term growth story. It will need a few years before it turns a profit. The health care industry takes gradual steps in moving from physical appointments to virtual-based ones.

Investors should take advantage of the volatile stock price movements. Fundamentals take time to mature. Teledoc has a multi-channel network that is growing. As payers and providers join the network, people in need of telemedicine will connect, too.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Chris Lau is a contributing author for InvestorPlace.com and numerous other financial sites. Chris has over 20 years of investing experience in the stock market and runs the Do-It-Yourself Value Investing Marketplace on Seeking Alpha. He shares his stock picks so readers get original insight that helps improve investment returns.