After its stock market debut, SoFi Technologies (NASDAQ:SOFI) needed to overcome tremendous selling pressure. SOFI stock finally bottomed in August, dropping below $14. Buyers accumulated the stock but then dumped it by mid-November at over $20. Why is this fintech trading at a wide range? The short interest on the stock is below 7%.

Last month, the company announced a secondary offering of 50 million shares of SOFI stock. The sale is not being conducted in order to raise capital for the company, rather it’s being used to enable existing shareholders to sell their shares. Softbank, Silver Lake Partners, and the Qatar Investment Authority are selling and the shares dipped on the news.

Investors also need to look at the bigger competing credit services firm to make sense of SoFi’s volatility.

Credit Services Selloff Hurt SOFI Stock

Credit services firm PayPal (NASDAQ:PYPL) tumbled in October after markets speculated it would buy Pinterest (NYSE:PINS). PayPal later rejected the rumor. Yet markets could not let go of worries that fintech firms like PayPal face a slowdown. SoFi enjoys a market capitalization in the $12 billion range. Its price-to-sales multiple of 35 times dwarfs that of PYPL stock, which is at 9x.

Markets must correct for the overvaluation by selling SOFI stock and avoiding PYPL shares. Traditional credit card firms like Visa (NYSE:V) trade at lower P/S multiples than SoFi. Visa’s vast network, strong customer service, reliable return policy and anti-scam capabilities will attract customers. SoFi offers a credit card product and loans. Customers may sign up and manage their financial needs entirely online.

Also, SoFi’s risks increase as it scales. The more customers it adds, the more staff it needs to improve customer service. This will add to the company’s operating costs. Should costs grow faster than revenue, losses will increase. Investors are taking a risk by buying the stock today. They are betting that SoFi’s business model will scale quickly.

Fintech Targets Quality Customers

At a virtual conference earlier this month, CEO Anthony Noto said that SoFi is targeting quality customers. It wants customers with a

household income of $100,000 or more. It also wants customers with a good credit rating.

SoFi will also need sophisticated customers who are comfortable with technology. It needs to grow its loan portfolio but keeping loan losses at 7% or lower. The hot economy suggests that SoFi will have loan losses lower than that target.

In the student loan business, SoFi expects the business to grow in 2022. Before Covid-19, SoFi enjoyed a student loan volume of over $2 billion a quarter. Investors may assume that the repo market will not freeze up again. So, the combination of higher personal loans and student loans will lift SoFi’s growth in 2022.

Since SoFi has a broad product offering, expect membership growth to lead to higher products per member. CEO Noto said that product additions per member will grow faster than membership growth. Investors should look for operating margin expansion in the coming quarters. That would help justify SOFI stock’s valuations.

Card Processors Offer Alternative

On Wall Street, five analysts rate SOFI stock as a stock to buy. According to TipRanks, the lowest price target is $19. Analyst Dan Dolev at Mizuho Securities has a street-high price target of $30.

Investors wary of the fintech sector and its growing costs could consider Visa instead. The stock fell below key moving averages in the last two months and bounced back. Mastercard (NYSE:MA), no stranger to investing in fintech, offers similarly strong prospects. Both firms are growing because of strong online transaction volumes. The pandemic increased those rates. If the pandemic induces lockdowns again, credit card firms will flourish.

When SoFi reports quarterly results in February, strong loan volumes and credit card sign-ups may give the stock a much-needed lift. Investors need to examine SoFi’s return on invested capital and return on equity in that report. Should those figures disappoint, long-term investors should not worry. The business will fluctuate as SoFi builds its customer base.

Risks Similar to Traditional Banks

Just as traditional banks are dependent on the housing and credit card market, SoFi is, too. When housing prices surged in the U.S. in the last year, it pressured loan volumes. Shareholders should watch for changes in mortgage demand.

The jittery stock market is a headwind for SoFi. Its SoFi Invest unit gives active investors commission-free trading. The company encourages customers to accumulate assets and to buy exchange-traded funds. A stock correction would hurt the growth in assets under management growth. Any slowdown in SoFi Invest would spook SoFi shareholders.

Click to Enlarge

Diversification Advised

SoFi is an emerging fintech with promising growth prospects. Investors should not consider SOFI stock in isolation. Instead, to reduce risk, investors should build a portfolio that includes this company, Visa, Mastercard, and other traditional banks. That would give investors exposure to a fast-growing market at lower risk levels.

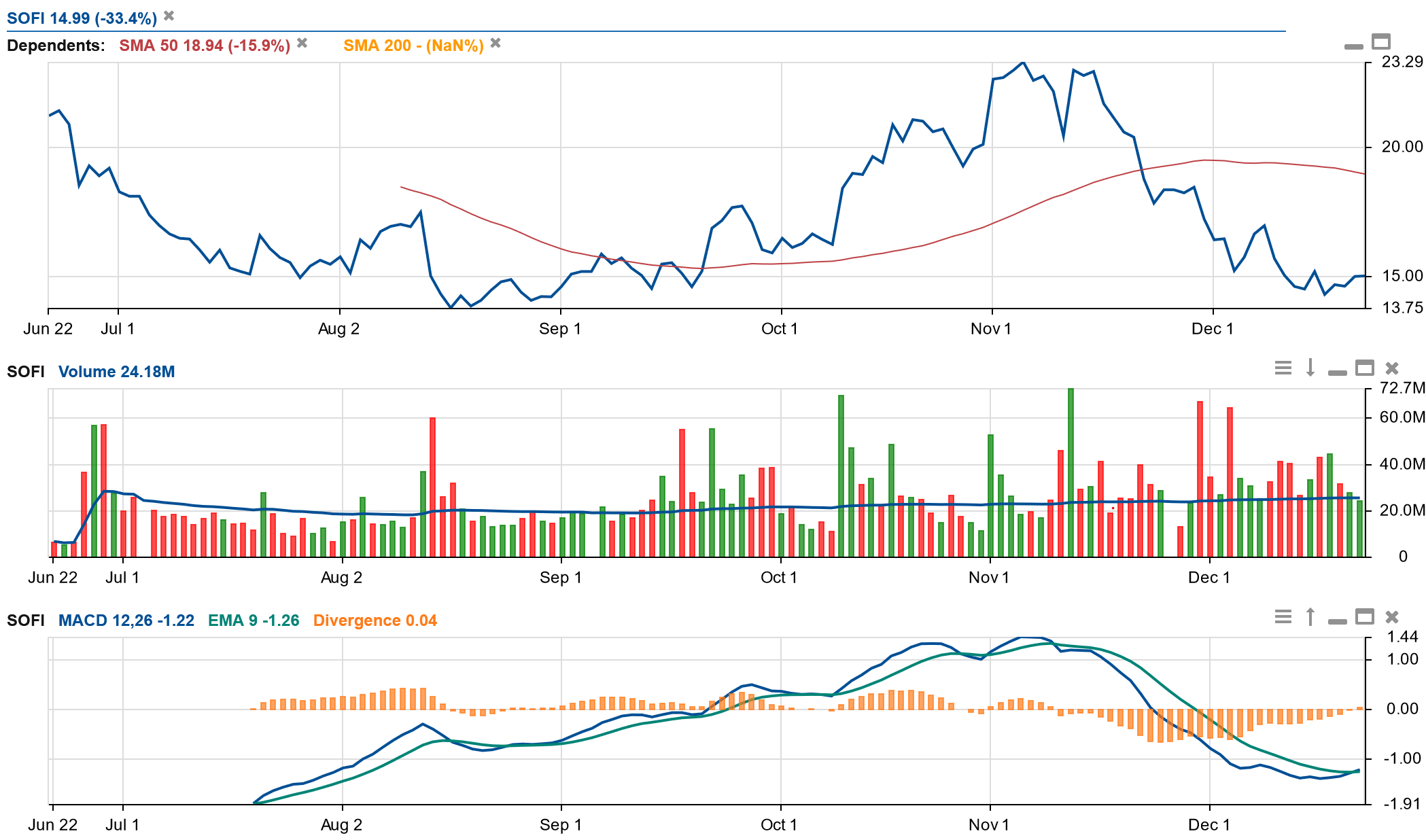

SoFi’s chart (above) shows buying volume is light as the stock rallied back to almost $15. The moving average convergence divergence is about to cross over. This suggests the stock could build an uptrend from here. Selling pressure accelerated without warning. Cautious investors could wait for the stock to form a bottom at current levels. As the stock breaks out, investors may add the stock on the way up.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com x Publishing Guidelines.

Chris Lau is a contributing author for InvestorPlace.com and numerous other financial sites. Chris has over 20 years of investing experience in the stock market and runs the Do-It-Yourself Value Investing Marketplace on Seeking Alpha. He shares his stock picks so readers get original insight that helps improve investment returns.