Upstart (NASDAQ:UPST) describes itself as an artificial intelligence lending platform that partners with financial institutions. When readers take away the AI and fintech buzz words, it has a business that is easy to understand. It provides consumer loans using a different algorithm. UPST stock suits investors that predict a customer’s creditworthiness using non-traditional variables, like education and employment.

How does Upstart differentiate itself from other credit services firms? Is Upstart worth the premium?

Invest in AI-Driven Lending Platform With UPST Stock

Upstart has seen some success with their new methods. The Corning Credit Union, a $2.1 billion credit union representing over 1,700 employer groups and businesses, recently selected Upstart’s AI-powered lending platform to provide personal loans. CCU will deliver an all-digital experience through the Upstart partnership. It will result in CCU’s ability to lend to more qualified members. By serving more clients with affordable credit, CCU’s business will grow.

CCU will join Upstart’s Referral Network. Through the network, Upstart.com will qualify loan applicants. If they meet CCU’s credit policies, the customer may complete the application on the CCU-branded site.

Neither company disclosed the value of the partnership. Investors need to infer what it will mean for Upstart’s growth potential. It has disruptive technology and tremendous revenue growth. In the second quarter, Upstart posted revenue growing by 1,018% to $194 million. In the third quarter, it posted revenue of $228 million, up by more than 250% from the year before.

250% Revenue Growth and Positive Net Income in Q3

Skittish investors sold off technology and credit services firms that did not have a profit. Upstart is profitable but still fell. The market mistakenly included UPST stock in the tech correction of 2022. Objective investors should look at the firm’s recent results. In the third quarter, Upstart reported a net income of $29.1 million, up from $9.7 million in the previous year.

Upstart’s Chief Executive Officer, Dave Girouard, said “Since Upstart’s IPO a year ago, we’ve more than tripled our revenue, tripled our profits, tripled the number of banks and credit unions on our platform, and tripled the number of auto dealerships we serve.”

At that growth rate, investors may argue that UPST shares should trade at a price-to-earnings of 300 times (or a P/E to Growth of 1.0 times). Instead, bearish investors are building a bet against the stock’s prospects. The short float is nearly 10%.

Strong Moat

Co-founder and Chief Data Scientist Paul Gu created the complex AI system powering Upstart. Competitors cannot easily copy the algorithm Upstart uses to accurately predict which customers it should lend to. Upstart compiles massive amounts of data to achieve the best profitable lending decisions. This is also known as machine learning. From there, the AI system decides which customers have minimal loan default rates.

The market panic discounts Upstart’s potential data advantage in the credit services market. Investors are judging fast-growing firms based mostly on valuation. They are switching to lower valuation firms like Visa (NYSE:V) and

Mastercard (NYSE:MA). Last week, MA and V stock both erased much of their losses from 52-week highs.

UPST stock is unlikely to return to the Oct. 2021 breakout that ended at $401.49. Still, the company will likely post consistently strong operating profits in 2022. For example, in this enterprise value-to-revenue multiples model, UPST shares are worth around $120.

Nasdaq Volatility a Major Risk

The proverbial “the markets can remain irrational longer than you remain solvent” applies to Upstart investors. Shares could spike higher or continue falling. If the stock stays in a holding pattern, that is the best scenario. This would set the stock up for a breakout to the upside if Nasdaq’s correction ends.

More importantly, Upstart will post its next quarterly earnings report in the month ahead. The company showed no signs of a slowdown in the last two quarters. Chances are high that Upstart will beat earnings and revenue expectations. Per Tipranks, analysts have an average price target of around $236. Wall Street expects Upstart will post earnings of 51 cents a share.

The company historically beat EPS estimates for four straight quarters.

Simplywall.st is cautious on Upstart’s fair value. It set a fair value of $56.95.

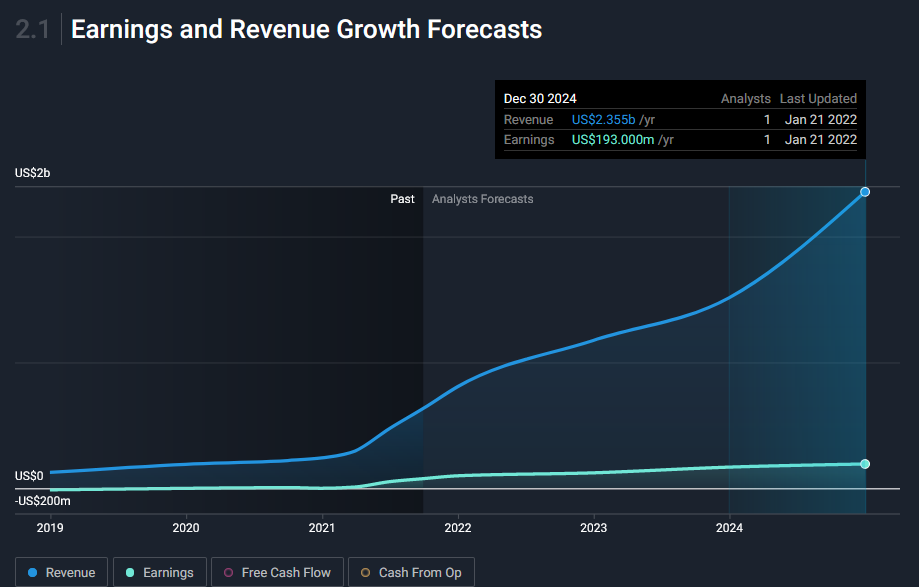

Click to Enlarge

Upstart could post moderate EPS growth in 2022, despite strong revenue. In the forecast to the right, Upstart’s revenue and profits will grow sharply.

Management must reinvest cash flow back to the business. This hurts profits. Impatient investors may sell shares in reaction to low profits. Growth investors experienced in holding strong companies like Upstart may ignore the volatility. In the long run, Upstart is carving a niche in the lending market.

Your Takeaway on UPST Stock

Demand for loans and credit services will only keep growing. Upstart is one of the few growth firms that are out of favor. That sentiment may not last much longer.

Investors should consider holding a position in Upstart along with established credit card firms. Readers cannot predict the future of market direction. Upstart might move either way, too. Consider holding Visa, Mastercard, and some Upstart shares to gain exposure to this fast-growing sector.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Chris Lau is a contributing author for InvestorPlace.com and numerous other financial sites. Chris has over 20 years of investing experience in the stock market and runs the Do-It-Yourself Value Investing Marketplace on Seeking Alpha. He shares his stock picks so readers get original insight that helps improve investment returns.