Companies in the modern era are very much focused on growth, and hypergrowth companies are driving the most gains in the stock market these days. While this narrative has been put aside a few times during market downturns, growth remains very important. However, as I said, these growth stocks can tumble when investors focus on profitability more during downturns.

That’s why hypergrowth stocks that are profitable trade at massive premiums. They have solid margins and the growth to continue driving up their share price. As long as Wall Street holds up its premium, these stocks can deliver 30%-plus growth annually. As such, I think having a stake in hypergrowth stocks is very important.

Here are seven hypergrowth stocks to look into:

Trip.com (TCOM)

Trip.com Group (NASDAQ:TCOM) operates online travel agencies in China. In Q1 2024, the company achieved an impressive 29% year-over-year revenue growth, reaching $1.65 billion. Adjusted EBITDA margin was a solid 33%. This business is solidly profitable even as it rapidly expands.

I believe Trip.com is well-positioned to benefit from the megatrends of surging outbound Chinese travel and the growing spending power of China’s older “silver” generation. Outbound hotel and air ticket bookings have fully recovered to pre-pandemic 2019 levels, while the company’s “Old Friends Club” initiative caters to the unique preferences of older travelers.

Trip.com’s international business is also flourishing, with APAC revenue soaring 80% YOY. Inbound travel to China has skyrocketed 400%, boosted by visa-free policies. Management’s move to offer free Shanghai city tours to travelers with long layovers shows they are proactively seizing opportunities in this fast-growing segment. Analysts are also very bullish here.

Click to Enlarge

Garmin (GRMN)

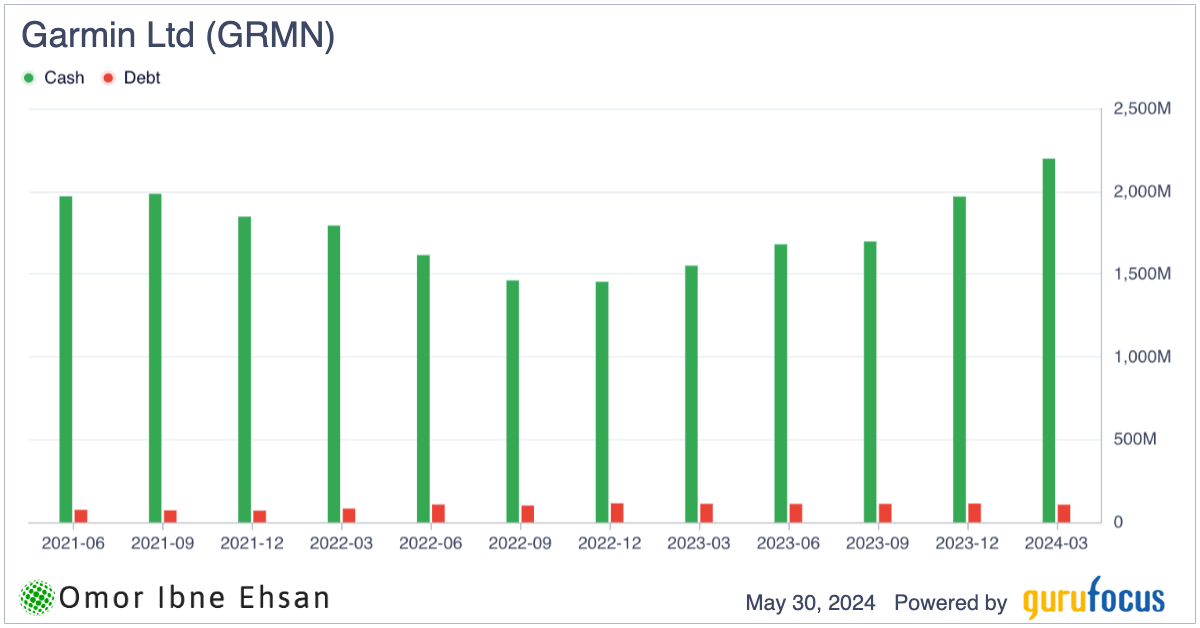

Garmin (NYSE:GRMN) sells GPS-enabled products across various markets. The company posted stellar Q1 results, with revenue surging 20% to a record $1.38 billion. Garmin is firing on all cylinders, with 4 out of 5 segments delivering double-digit growth. The cash flow here is good enough for the stock to have a 1.86% dividend yield as of writing. It also has very little debt.

Click to Enlarge

I’m particularly bullish on the aviation tailwinds propelling Garmin’s business. The segment grew a modest 2% this quarter, but make no mistake — a new boom in aviation is taking flight. Trump’s tax cuts from a few years back are finally materializing into increased air travel and jet purchases now that the pandemic has faded.

Garmin is shrewdly positioned to ride this wave with its avionics modernization programs and advanced radar systems. The company’s cutting-edge aviation tech is reducing pilot workloads and enhancing safety.

With operating margins expanding to 21.6% and generating a record $298 million in operating income, up 51%, Garmin’s growth story is gaining altitude.

Chart Industries (GTLS)

Chart Industries (NYSE:GTLS) is a leading manufacturer of cryogenic equipment used in important industries like gas and renewable energy. I’m really impressed with how well Chart performed last quarter across orders, revenue, profit margins, and EBITDA, driven by surging demand from the growing liquefied natural gas (LNG) and clean energy sectors.

Click to Enlarge

Revenue jumped 18% to $951 million while gross profit margins expanded 260 basis points to 31.8%, powering a 73% increase in EBITDA to $212 million. This improvement in margins shows the synergies from Chart’s acquisition of Howden are starting to be realized.

What excites me most is Chart’s enormous $22 billion sales pipeline, the largest in the company’s history. This pipeline signals the long growth opportunity ahead in LNG, hydrogen, water treatment, and other markets. With orders exceeding sales by 1.18 times and a rising order backlog of $4.3 billion, I expect Chart’s business momentum to accelerate throughout 2024.

The company should be able to power solid growth for many years to come.

Shift4 Payments (FOUR)

Shift4 Payments (NYSE:FOUR) provides integrated payment processing and technology solutions. I believe this fintech company is well positioned to deliver significant gains for investors willing to take advantage of the sector’s current bargain valuations.

Click to Enlarge

While the broader fintech space has struggled for a while, Shift4’s first-quarter results showed remarkable resilience and growth. The company saw a staggering 50% surge in end-to-end payment volume and an impressive 27% increase in gross profit. Even better, Shift4 expanded its EBITDA margins by 150 basis points to a robust 46% despite costs from recent acquisitions.

The company has had major wins, such as working with Foxwoods casino and developing partnerships with top global casino companies. Shift4’s restaurant point-of-sale solution, SkyTab, also showed accelerating momentum, with installs jumping 38% sequentially.

As borrowing picks up and e-commerce volumes increase, I expect Shift4’s growth to kick into an even higher gear.

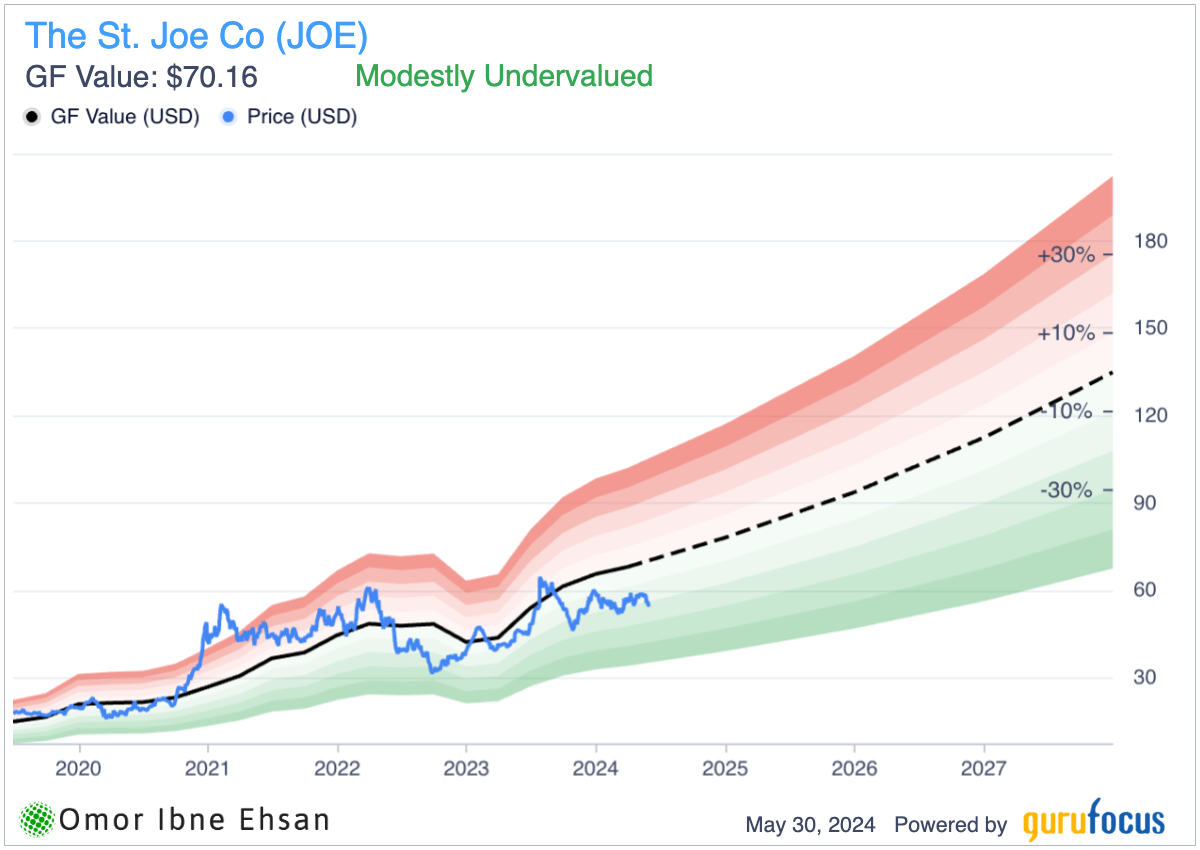

The St. Joe Company (JOE)

The St. Joe Company (NYSE:JOE) is a real estate development firm based in Florida. I believe JOE is poised for significant growth as Florida’s population surges and people relocate to Florida from across the country. In Q1 2024, JOE’s revenue jumped 20% YOY to $87.8 million, while net income attributable to the company rose 34% to $13.9 million.

Residential real estate revenue climbed 10% as JOE sold 216 homesites at an average price of $117,000, up from $80,000 a year ago. The company has another 1,335 homesites under contract, representing future revenue of nearly $120 million. With Florida now the fastest-growing state amid a national housing shortage, JOE’s 21,000 homesite development pipeline perfectly positions them to capitalize on this demand.

JOE’s unique business model includes expanding hospitality and leasing segments that complement its core residential development. This creates a virtuous cycle that should power sustainable long-term growth. Even in a recession, Florida’s population influx and housing supply constraints make JOE stock very sturdy.

Click to Enlarge

Duolingo (DUOL)

Duolingo (NASDAQ:DUOL) operates a popular language-learning app. The company’s growth seems unstoppable, with revenue surging 45% and bookings jumping 41% in Q1. I believe Duolingo is riding powerful tailwinds that could propel this stock much higher over the coming years. The global language learning market is estimated to reach a staggering $115 billion by next year, yet Duolingo has captured less than 1% of it so far. This highlights the massive untapped opportunity, especially in teaching English to the vast majority of language learners worldwide.

But even in the U.S., Duolingo is gaining rapid adoption from the younger generation’s growing interest in learning second languages. With immigration into the U.S. surging in recent years, millions of new residents could also turn to Duolingo to master English. In countries like Sweden, which has large migrant populations, Duolingo has already become a go-to resource for newcomers who want to learn the local language. I wouldn’t be surprised to see a similar trend play out in the U.S.

Li Auto (LI)

Li Auto (NASDAQ:LI) makes premium smart electric vehicles in China. While Q1 deliveries surged 52.9% YOY to 80,400 vehicles, the company admittedly faced challenges that caused its performance to fall short of initial 2024 expectations. Revenue grew 36.4% to RMB25.6 billion but missed estimates by RMB1.84 billion. EPS of RMB1.23 was also missed by RMB0.22. Gross margins remained healthy at 20.6% despite price adjustments.

I believe some cracks have begun forming in Li’s hypergrowth story. However, with RMB100 billion in cash reserves and industry-leading profitability, it remains by far the most solid EV startup. The stock has been battered by macro headwinds in China that I expect to dissipate as monetary policy loosens. Trading at just 17x forward earnings with solid revenue growth, Li looks attractive at current levels. While risks remain elevated, I think the worst is likely priced in. Analysts are very bullish here.

Click to Enlarge

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.