High-yield dividend stocks are some of the best investments you can make in the current environment. Most top growth and tech stocks are all trading at nosebleed valuations. Thus, I’d put these companies solidly in “hold” territory right now. In my opinion, it would be prudent to exercise caution when considering new positions in these frothy areas of the market.

You can take new positions in such companies for the long-run. But if you want to play it safe, dividend stocks do the job better. The best thing about high-yield dividend stocks is that you can reinvest these high yields over decades. This reinvestment, combined with the underlying stock’s appreciation, can turn a small investment into a huge amount over time. This compounding effect is a powerful wealth-building tool that patient investors can take advantage of.

Here are seven dividend stocks that, if recent trends continue, can put an extra $12k in your pocket if you invest $100k into this group. Most of these stocks don’t have double-digit yields, but they can certainly return more than $12k a year if you reinvest each year, or if these stocks appreciate more.

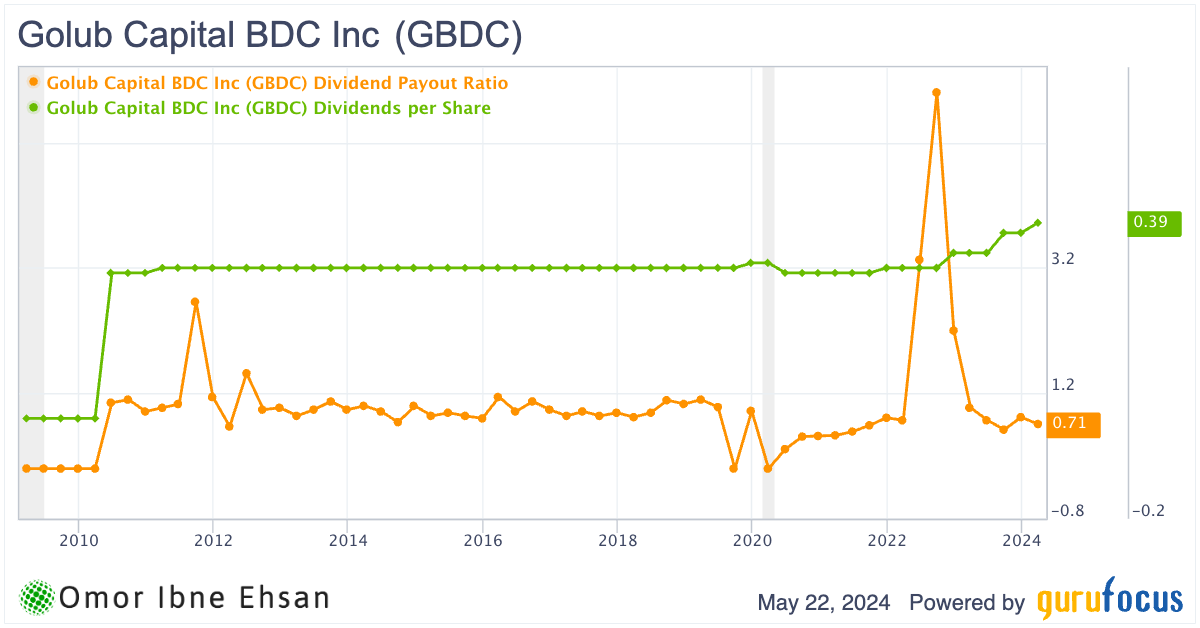

Golub Capital BDC (GBDC)

Golub Capital BDC (NASDAQ:GBDC) is a company that provides funding to medium-sized businesses through set-rate loans. BDC delivered exceptional results in its second quarter, with adjusted net investment income per share reaching a record high of 51 cents, up 21% from last year. This equates to an impressive annual return of 13.5% for shareholders.

I’m particularly enthusiastic about GBDC’s upcoming merger with Golub Capital BDC 3 and the fee reductions that will establish GBDC’s fee structure as a new “gold standard” for comparable companies. The company’s base management cost is slated to decrease to 1% as of July next year, and incentive fees will drop from 20% to 15% upon completion of the merger.

With strong credit quality, no new defaults, and a decreasing percentage of non-accruals, I think GBDC is well-equipped to benefit in this higher-interest environment. The stock currently yields around 9.54% as of writing, making it an appealing option for income investors comfortable with investing in this type of company.

Click to Enlarge

I’ll be watching to see if GBDC can maintain its momentum, but the company’s second quarter results were very positive for the bull thesis on this stock.

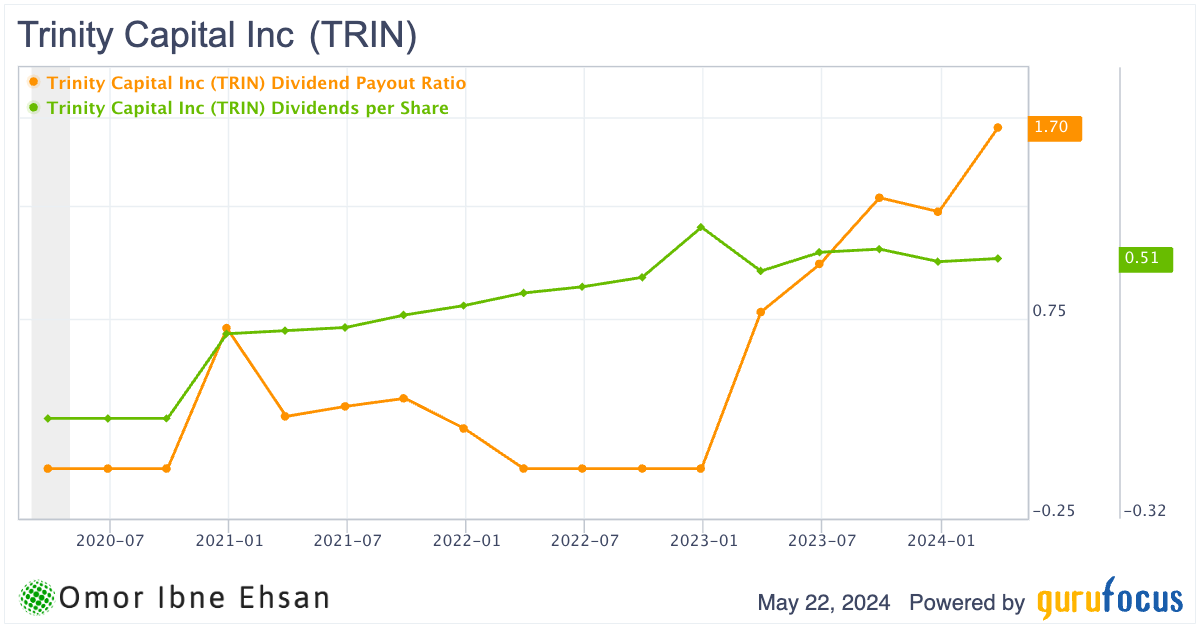

Trinity Capital (TRIN)

Trinity Capital (NASDAQ:TRIN) delivered strong results in Q1, reinforcing my conviction in this high-yield stock. This company funds growth-stage companies. The company’s financials aren’t the most stable, and this stock has seen downturns in the past. However, with a valuation that’s lower than it’s been in some time, TRIN stock is definitely a top dividend-paying stock you should consider buying.

In Q1, the firm reported $243 million in gross funding across eight new and 12 existing portfolio companies, driving 38% year-over-year growth in assets under management (AUM) to $1.6 billion.

Trinity also had a record net investment income of $25.2 million, up 30% from last year. This allowed the firm to boost their quarterly dividend to 51 cents per share, marking the 13th consecutive increase.

Click to Enlarge

With a current yield of over 13.6%, Trinity is a very tempting option for income-focused investors. Notably, 21 portfolio companies raised an aggregate $1.2 billion of equity in Q1. The company ended the quarter with $405 million in unfunded commitments, so I see more growth ahead.

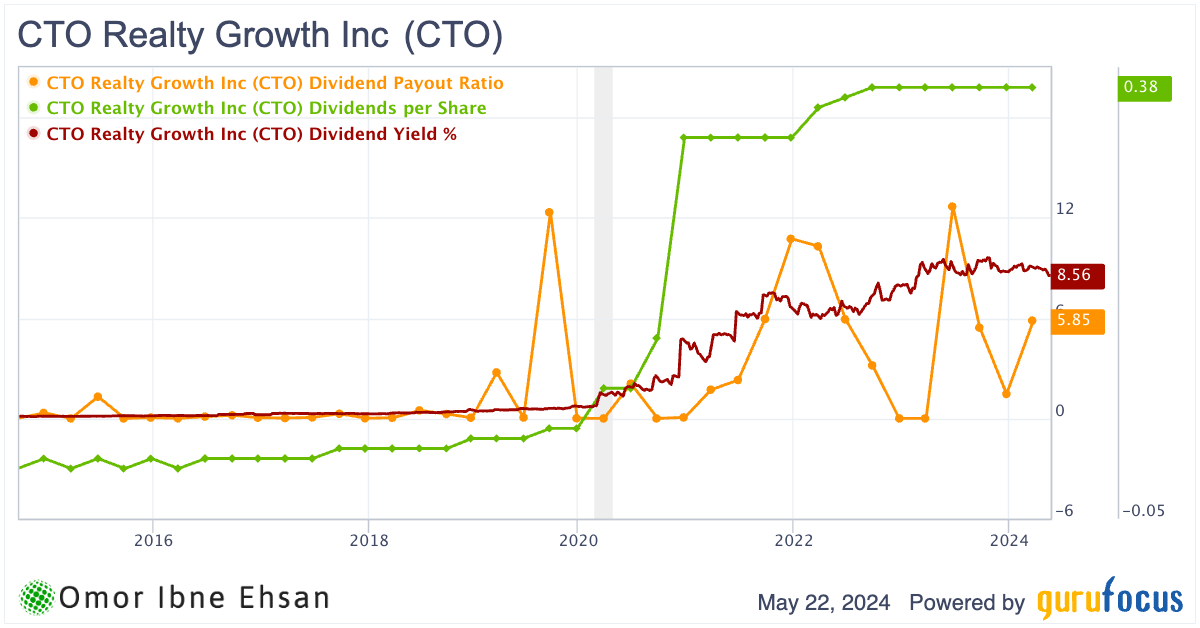

CTO Realty Growth (CTO)

CTO Realty Growth (NYSE:CTO) owns and operates retail properties across the Sun Belt. The company’s recent results highlight the ongoing strength of their business model.

CTO recently signed over 100,000 square feet of new leases, with an average rent of $27.12 per square foot. Notably, CTO secured a strong new tenant for one of their shopping centers that had been home to Regal Cinemas. This deal came in at significantly higher rental rates, too. I’m encouraged that the leases they have signed. However, the tenants that haven’t yet moved into these properties have driven a 3.5% increase in the amount of vacant space on their books.

On the acquisition front, CTO purchased the final property in a shopping center anchored by Sprouts Farmers Market, a prime retail location in the fast-growing Orlando market. With around 17% of their rental income now coming from Florida, CTO is well-positioned in a state with strong population growth.

Their issuance of Series A preferred stock, which raised $33 million, will allow CTO to pay off floating-rate debt with variable interest rates. Plus, their nearly 93% occupancy rate makes me think that this is a much safer bet than people realize.

Click to Enlarge

CTO’s dividend yield of more than 8.5% is why I think it’s a buy. But I don’t expect this yield to stick around forever, as the company doesn’t have a long history of consistently paying dividends.

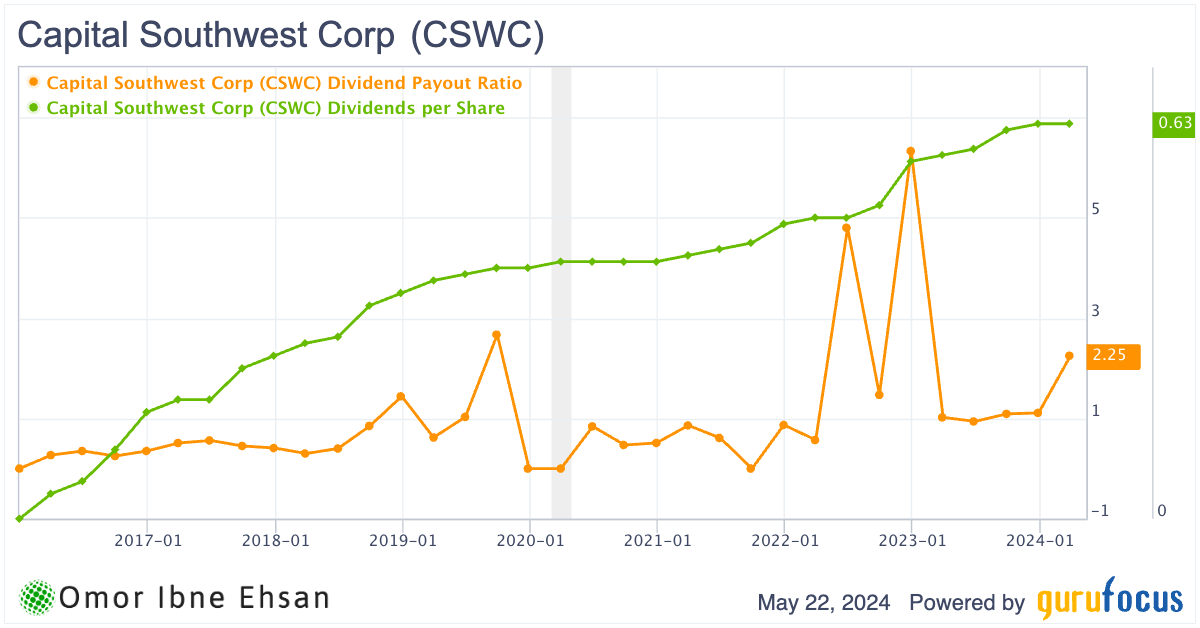

Capital Southwest (CSWC)

Capital Southwest (NASDAQ:CSWC) is a company that provides flexible funding solutions to medium-sized businesses. What continues to impress me about this lender is its strong portfolio and increasing dividend. In the 2024 fiscal year, Capital Southwest grew its investment portfolio by an impressive 22% to $1.5 billion, while boosting pre-tax net investment income per share by 18%.

The company also increased their regular dividend by 10% to $2.24 per share and paid an additional 23 cents per share in supplemental dividends. With a 121% regular dividend coverage ratio, I have confidence that these payments can be sustained.

Capital Southwest raised over $500 million in fresh capital, while maintaining a modest leverage of 0.82x debt-to-equity. And with 64 cents per share in undistributed taxable income, I expect more special dividends could be forthcoming.

Click to Enlarge

The dividend yield here is a juicy 9.5%. The company’s payout ratio may look concerning, but I think this is a short-term blip, and this ratio should return to normal levels. The median payout ratio has been around 1.02%, so a return toward these levels would be welcome.

Blue Owl Capital Corporation (OBDC)

Blue Owl Capital Corporation (NYSE:OBDC) is a business development company that provides loans to middle-market firms. Its lending portfolio has proven resilient despite rising interest rates. OBDC delivered net investment income of 47 cents per share this past quarter. This represents a solid 12.1% return on equity. What’s more, the company increased its net asset value to a record high of $15.47 per share, while maintaining an excellent credit profile.

OBDC’s portfolio companies are showing steady revenue and EBITDA growth. With an average loan-to-value ratio of less than 45% and interest coverage of 1.6x, their borrowers seem well-equipped to navigate the current environment. OBDC’s non-accrual rate remains low at just 1.8%, which gives me added confidence.

OBDC declared a 37 cents regular dividend and a five cents supplemental payout for income-oriented investors, totaling an attractive 10.12% yield as of writing. Given their strong earnings, I believe the dividend remains fully covered and primed for potential increases going forward.

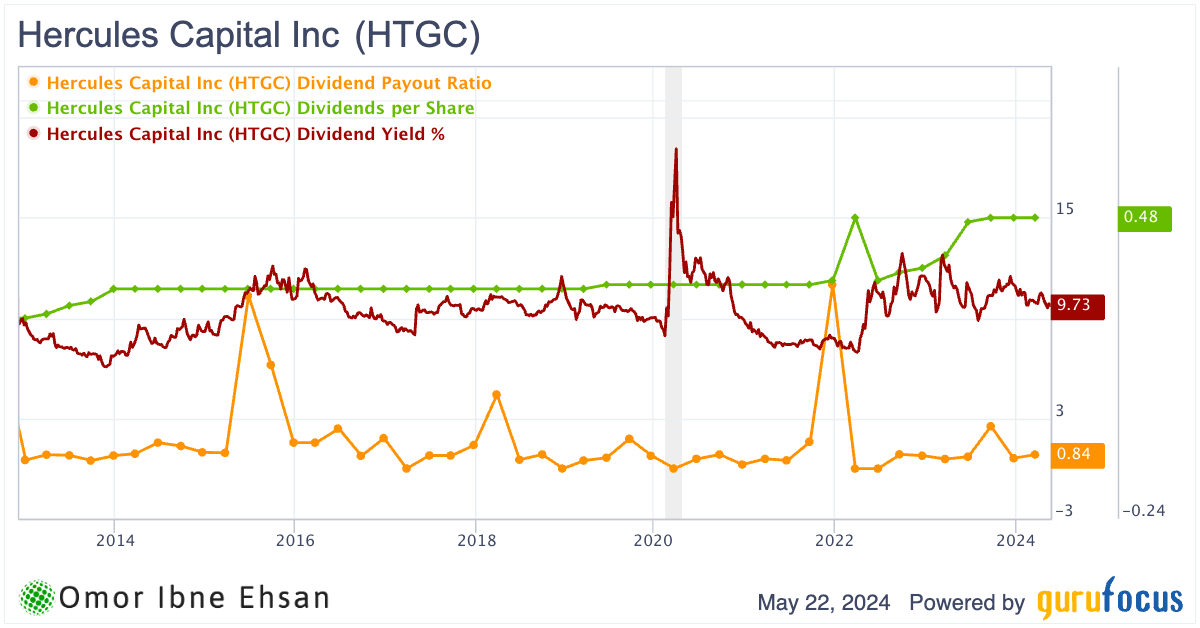

Hercules Capital (HTGC)

Hercules Capital (NYSE:HTGC) is a specialty finance company that provides debt and equity to high-growth venture capital-backed companies. This company has also had a stellar earnings season.

Hercules just delivered a blowout in Q1. The company reported record origination and funding numbers, with $956 million in gross commitments and $605 million in funding. That’s the best funding quarter in its history. This has historically been a stable stock that has rebounded consistently from previous downturns.

What’s even more remarkable is that Hurcules achieved this while maintaining a conservative 93.6% GAAP leverage ratio. That disciplined approach allowed the firm to generate a robust 14.9% portfolio yield and core net investment income of 50 cents per share, handily covering their base 40 cents dividend by 125%.

I like how they’re staying defensively positioned with 88.4% first-lien exposure, while still flexing into offense mode when quality deals emerge. With a long liquidity runway and the proven ability to perform in volatile markets, Hercules looks well-positioned to continue delivering strong NII and dividend coverage.

Click to Enlarge

HTGC’s dividend yield is attractive ,and dividend payouts have been consistent for a long time. Plus, management is balancing yield with credit quality and a fortress balance sheet. That’s a winning combination. The stock is also up 43% over the past year!

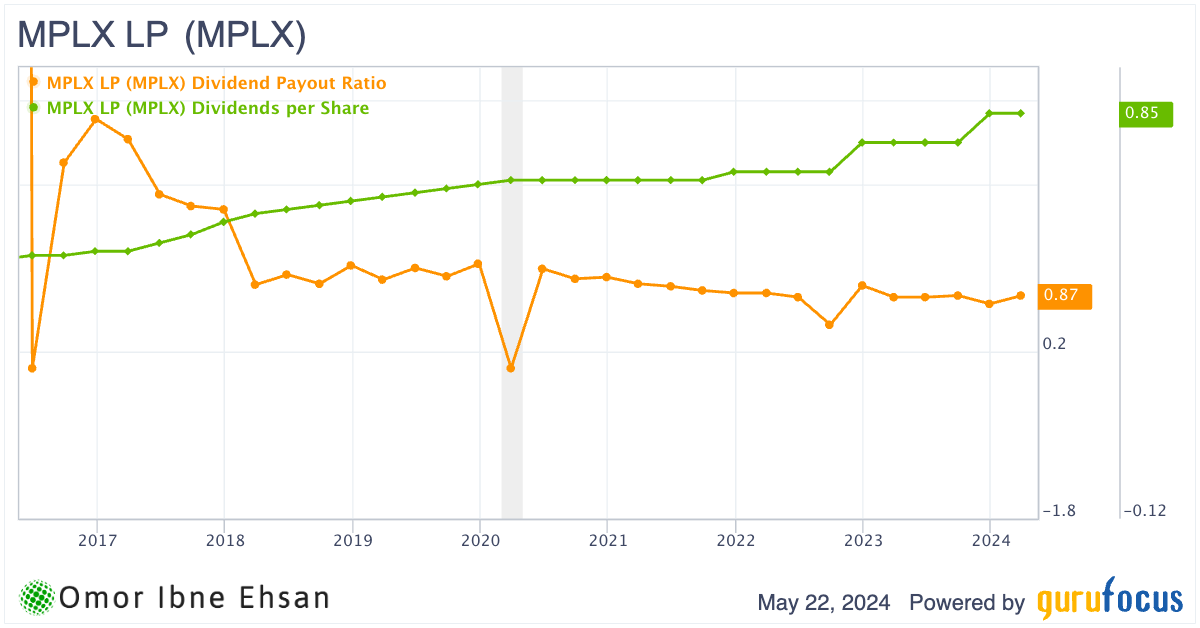

MPLX LP (MPLX)

As one of the largest fuel transporters in the United States, MPLX LP (NYSE:MPLX) operates a vast network of pipes and facilities that allow America’s energy resources to reach where they’re needed. And business has undoubtedly been booming lately.

In Q1, MPLX delivered an impressive surge in cash, with adjusted EBITDA jumping 8% to reach $1.6 billion. That tremendous profit translated into $1.4 billion of cash available for distribution, which is also up 8% compared to the prior year. Additionally, the company’s net profit margin comes in at a healthy 37.4%.

MPLX has a management team that isn’t letting all that money just sit around, either. During the quarter, the company returned a generous $951 million to unitholders. With the United States now among the lowest-cost producers globally, and worldwide demand for oil constantly breaking records, MPLX seems well-positioned to keep the payouts flowing steadily.

Click to Enlarge

Currently, MPLX stock pays out a dividend yield of 8.3%, and if Trump wins the election and drilling activity picks up, we could see a lot of upside here.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.