The electric vehicle industry has been struggling, and it is easy to argue that most EV stocks are worth selling at this point. Rate cuts are unlikely to be fast enough, barring a recession, which would be even worse for EVs. With that in mind, it makes sense to look for EV stocks to sell before the lights go out.

EV startups should be the top candidates if you are looking for EV stocks to sell. These companies have been some of the worst performers in the market so far. They are perpetually diluting their shareholders and burning huge amounts of cash with only a few dozen units to show for it. And, even those units are sold at negative margins.

With that in mind, here are seven EV stocks to sell.

VinFast Auto (VFS)

VinFast Auto (NASDAQ:VFS) is a Vietnamese electric vehicle manufacturer that has seen its hype train derail spectacularly over the past year. Once touted as a potential EV juggernaut, VinFast’s dirt-cheap labor costs and massive addressable market in Southeast Asia had investors salivating over its export potential.

However, the curtain has been pulled back to reveal a company hemorrhaging cash at an alarming rate with no clear path to profitability. In Q1, VinFast delivered a paltry 9,689 vehicles globally, a rounding error compared to established automakers. While this represented 444% year-over-year growth, it’s building from an extremely low base.

Management’s full-year target of 100,000 deliveries seems like a pipe dream, considering the sluggish 2,421 quarterly run rate. VinFast’s VF 5 and VF 6 models accounted for the bulk of sales.

Despite management’s rosy outlook, macroeconomic headwinds and fading EV exuberance will likely keep VinFast’s sales stuck in neutral for the foreseeable future. I have little confidence this cash-burning machine can achieve sustainable profitability before diluting equity holders into oblivion.

Lucid Group (LCID)

Lucid Group (NASDAQ:LCID) manufactures luxury electric vehicles, but I believe this EV startup is a prime example of a struggling company that investors should avoid. Saudi money is unlikely to keep it afloat forever.

In Q1, Lucid missed on both the top and bottom-lines, with EPS of -30 cents missing by 5 cents and revenue of $172.74 million missing by $9.74 million. While deliveries were up 39.9% YOY, Lucid only expects to produce about 9,000 vehicles in 2024. That’s a drop in the bucket compared to Tesla’s (NASDAQ:TSLA) production.

Sure, Lucid touts its superior technology and steadfast support from Saudi Arabia’s PIF. But the reality is that this company is burning cash at an alarming rate. Lucid had to raise another $1 billion just to keep the lights on this quarter, and it will need more!

Even with the U.S. subsidies and tariffs currently propping up American EV companies, I don’t believe Lucid can compete with Tesla in the long run. Throw in the uncertainty around the 2024 elections and potential rollback of EV subsidies, and Lucid looks like a sinking ship.

Faraday Future Intelligent Electric (FFIE)

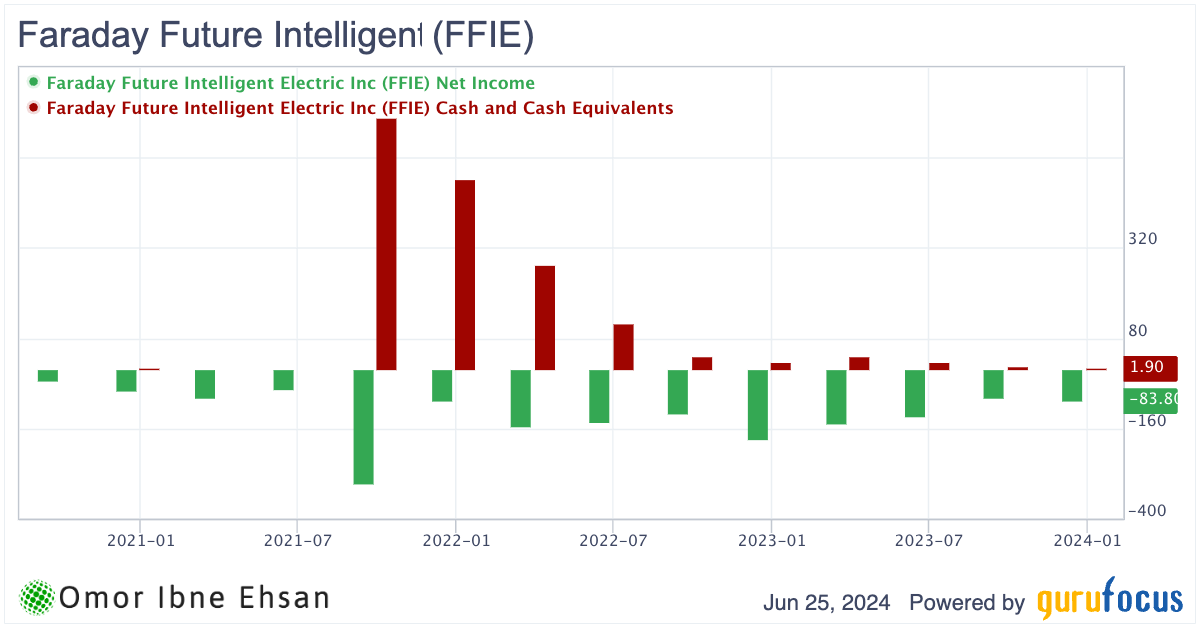

Faraday Future (NASDAQ:FFIE) develops and manufactures ultra-luxury electric vehicles, but that’s about the only positive thing I can say about this struggling company. The company delivered a measly 11 vehicles to date. That’s not a typo. The company’s flagship FF 91 2.0 costs an eye-watering $309,000, which is enough to buy nearly six Teslas with similar specs. It’s hard to imagine any significant demand at those astronomical prices, especially considering the FF 91 is already outdated by several years in its capabilities.

Faraday Future’s financials paint an even bleaker picture. The company racked up a staggering $1.5 billion in net losses over the past three years while burning through cash at an alarming rate. As of now, Faraday has less than $2 million in cash remaining, which is barely enough to keep the lights on, let alone scale vehicle production.

Click to Enlarge

To make matters worse, Faraday Future is caught in a vicious cycle of dilution and reverse stock splits that are rapidly eroding shareholder value. In fact, management just proposed another reverse split ranging between 1-for-2 to 1-for-40 shares. That’s not the kind of financial engineering that instills confidence.

Given these immense challenges, I struggle to see how Faraday Future can avoid bankruptcy in the coming months. The company is essentially trying to sell an overpriced, outdated product to a minuscule market while hemorrhaging cash. That’s a recipe for disaster in my book, placing FFIE among EV stocks to sell.

Nikola (NKLA)

Nikola Corporation (NASDAQ:NKLA) manufactures electric and hydrogen-powered trucks. The company reported a disappointing Q1 2024, with revenue of just $7.5 million, missing estimates by a staggering $7.83 million. This 32.56% YOY decline highlights the immense challenges Nikola faces in its niche market.

I believe Nikola’s focus on electric and hydrogen trucks is simply too far ahead of its time. The technology isn’t there yet to make these vehicles viable for most companies. Battery limitations severely hinder the practicality of electric trucks, while hydrogen infrastructure remains scarce. Nikola’s venture into EV military vehicles seems even more far-fetched in the current landscape.

The company’s future looks bleak, with mounting losses and dwindling cash reserves. Nikola burned through $131 million in Q1 alone. I wouldn’t be surprised to see them file for bankruptcy protection in the coming quarters as they struggle to stay afloat.

Unless EV subsidies ramp up significantly, I don’t see how Nikola can compete against traditional trucks. Companies adopting Nikola’s offerings would likely destroy their bottom-lines.

Rivian Automotive (RIVN)

Rivian Automotive (NASDAQ:RIVN) builds and sells electric pickup trucks, SUVs and delivery vans. Despite growing its market share to 5.1% and becoming the fifth best-selling EV maker in the U.S. in Q1, I believe Rivian faces an uphill battle. The company posted a staggering net loss of $1.45 billion in the quarter, which is simply unsustainable. Yes, Rivian still has a sizable $7.9 billion cash buffer, but at this burn rate, bankruptcy isn’t out of the question.

I’m skeptical about Rivian’s path to profitability without significantly raising prices, which the current market won’t support. And if EV subsidies get cut, Rivian’s challenges will only intensify. The stock is also seeing substantial dilution, so even in a best-case scenario, shareholders might not see meaningful returns.

While Rivian’s vehicles are impressive, and the brand is gaining traction, I think the company is biting off more than it can chew.

ChargePoint Holdings (CHPT)

ChargePoint (NYSE:CHPT) provides EV charging solutions. But this stock is one to sell before it plummets to zero. The company has been hemorrhaging market share over the past few quarters as it struggles with deep unprofitability. ChargePoint’s revenue in Q1 was only $107 million, a concerning 18% YOY decline. Gross margins inched up to a meager 24%, while its adjusted EBITDA loss was still an abysmal $36 million.

Management seems to be grasping at straws, touting “large deals” later this year to achieve EBITDA breakeven by Q4. However, I have little faith in this pipe dream, considering ChargePoint’s track record of overpromising and underdelivering. The reality is that ChargePoint is simply outmatched by bigger, more competitive players in the EV charging space. Dilution is already on the rise here.

Click to Enlarge

With EV adoption still in the early innings, ChargePoint will likely run out of cash and declare bankruptcy long before industry tailwinds can rescue its business model.

Innoviz Technologies (INVZ)

Innoviz Technologies (NASDAQ:INVZ) makes LiDAR sensors and perception software for autonomous vehicles. I’m very bullish on the LiDAR sector’s long-term potential, but that doesn’t mean every company is a smart bet. Innoviz is one struggling EV stock I would sell before it potentially heads to zero. The stock has plunged 64.7% in the past year as net losses hit $30.1 million in Q1 alone. With just $123.4 million in cash left, I don’t believe Innoviz has the funds to survive long enough to turn profitable.

While Innoviz scored early wins with BMW (OTCMKTS:BMWYY) and VW (OTCMKTS:VWAGY), competition is rapidly intensifying. Rivals are also launching Level 3 autonomy and aggressively pursuing the same automakers. Meanwhile, Innoviz is burning cash supporting these complex rollouts across the globe. Gross margins improved to just 17% but remain concerningly low. I view INVZ as one of the EV stocks you will want to sell now.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.