If you’re looking for penny stocks to buy in June, you should remember that it is difficult to predict whether or not a stock will pop in a particular month.

As such, I am focusing more on long-term bets, offering good entry points in June. I believe this should lead to a much greater chance of success. I am focusing on penny stocks with underlying businesses that are likely to turn profitable soon or are already profitable–or at least have the cash to cover their losses until they turn profitable.

This should insulate you from potential dilution and expose you to hefty upside potential. Here are seven such penny stocks to buy.

Podcast One (PODC)

PodcastOne (NASDAQ:PODC) is a leading platform that shares content across major podcast directories. This smaller company is set up for big growth in the coming years. The podcast industry is taking off, with more people tuning in all the time and large players like Spotify (NYSE:SPOT) investing heavily in exclusive shows. PodcastOne is well-positioned to benefit from these positive trends.

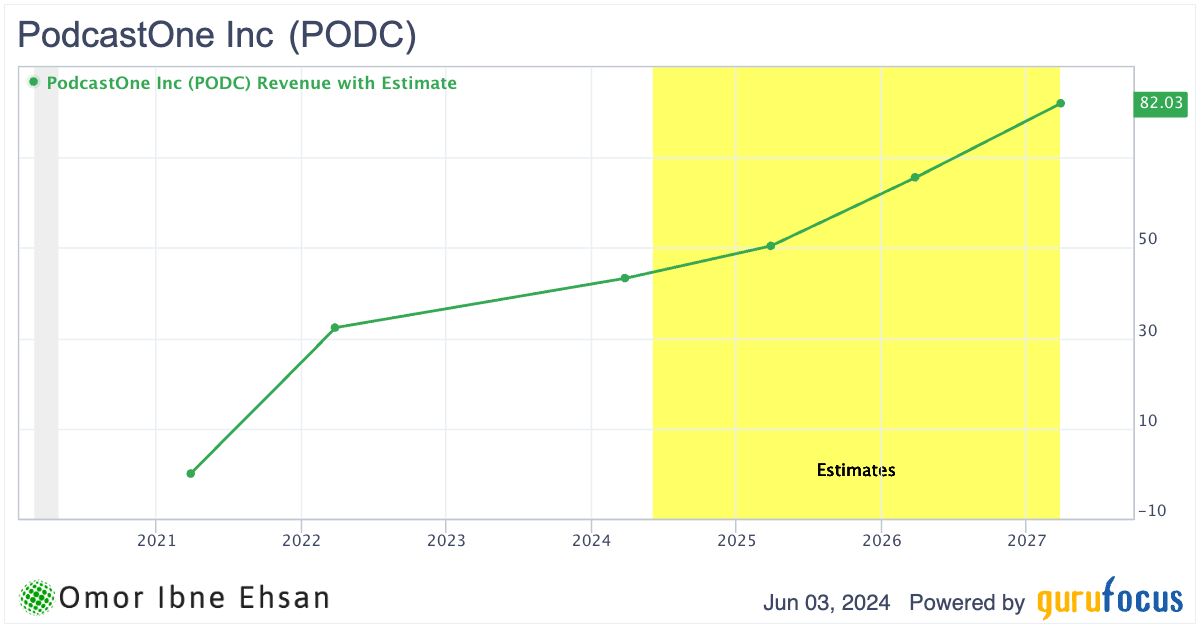

It has a growing roster of popular shows and high-profile talent signings. The company also has revenue growth of 22% year-over-year, driven by rising ad rates as brands see the unique engagement of podcast promos. With a market cap of just $44 million, PodcastOne looks significantly undervalued compared to peers, considering it has 6 million monthly active listeners. Revenue is expected to see solid growth going forward.

Click to Enlarge

As major tech platforms compete for audio dominance, I wouldn’t be surprised if a larger company wanted to acquire PodcastOne. Taking a small speculative stake in PODC could deliver multibagger returns for investors willing to accept some ups and downs.

Intellicheck (IDN)

Intellicheck (NASDAQ:IDN) provides identity verification solutions that can help prevent fraudulent activity. Companies need stronger identity protection across different industries as reports of theft and account takeovers have surged.

With reported losses from identity fraud reaching an enormous $23 billion in 2022, according to Javelin Strategy & Research, companies simply cannot ignore this growing crisis. Intellicheck could be a big beneficiary of this megatrend. Real estate and financial services, two key markets they work in, are struggling with unusually high rates of impersonation fraud and fraudulent applications.

The company posted Q1 revenue of $4.68 million, up 10% YOY. It doesn’t look flashy right now, but analysts expect 14% growth in sales for all of 2024 and 19% sales growth next year. Moreover, profitability is close, with 3 cents in EPS expected in 2024 and 9 cents next year. In a world where one data breach can instantly shatter user trust, this company could land big contracts.

FingerMotion (FNGR)

FingerMotion (NASDAQ:FNGR) offers mobile payment and recharge services in China. I believe this company is well-positioned to benefit from some significant trends unfolding. With over 1.4 billion mobile subscribers, China has the largest mobile market in the world. FingerMotion’s “Telecommunication Products & Services” has been driving the majority of the company’s growth.

This is mostly due to China’s rollout of 5G connectivity. The telecom segment saw revenue grow from $27 million to $32.8 million from 2023 to 2024. Thus, total revenue climbed $1.74 million despite declines in other segments.

While still experiencing a net loss of $3.8 million, it is down significantly from losses of $7.6 million in 2023. Gross profits grew 67%, so I see breakeven if the trajectory continues. Of course, the stock price may fluctuate considerably. However, the potential upside could be significant.

SelectQuote (SLQT)

SelectQuote (NYSE:SLQT) provides insurance sales and distribution services. SelectQuote’s strong Q3 results show a turnaround and position it for continued growth. Revenue of $376 million (up 26% YOY) beat estimates by nearly $37 million, driven by the core Senior Medicare Advantage segment delivering $204 million at a healthy 30% EBITDA margin. This marks nine straight quarters of the Senior business overdelivering.

SelectQuote’s focus on operating efficiency is working, with marketing and operating costs remaining well below 2021 levels despite the robust top-line growth. The company’s agent productivity initiatives and improved marketing targeting are driving sustainably lower customer acquisition costs. At the same time, SelectQuote’s push into healthcare services is already bearing fruit, with membership exceeding 75,000.

The company is now tapping into the massive market opportunity around Medicare Advantage. With 10,000 seniors aging into Medicare eligibility each day (probably even more in 2024) and MA penetration steadily rising, SelectQuote’s largest segment has a long growth runway ahead. The company’s unique omnichannel distribution platform and carrier relationships position it to continue taking share in this expanding market.

I think the company has turned the corner. With management guiding for positive operating cash flow in fiscal 2024 and multiple margin expansion levers, the stock is poised for meaningful upside ahead. It is up 62.5% in the past year. Analysts see more ahead.

Click to Enlarge

SigmaTron International (SGMA)

SigmaTron (NASDAQ:SGMA) provides electronic manufacturing services. I believe this penny stock could appreciate significantly in the coming months. The company’s latest earnings show strong tailwinds, with profits bouncing back by 103%. Revenue also grew 3.4%.

With $194.5 million in current assets, including $135.5 million of inventory, SigmaTron appears well-positioned to fulfill rising orders. The EMS megatrend should continue driving growth, especially in key end-markets like industrial electronics and medical devices. It does have some debt, but profits are starting to improve. The stock is up nearly 86% from its Oct. 2023 trough, and as long as profits keep rebounding, I see further upside.

WM Technology (MAPS)

WM Technology (NASDAQ:MAPS) provides software infrastructure solutions for the cannabis industry. The company’s Q1 2024 results show promising signs of recovery and profitability. Net income surged to $2 million, a significant turnaround from the $4 million loss in Q1 2023. Adjusted EBITDA also improved to $9.6 million, up from $7.1 million YOY.

While revenue dipped slightly to $44.4 million due to industry consolidation and constrained client budgets, WM Technology is making smart moves. They removed non-paying clients and discontinued certain lower-margin SaaS products. This strategic pruning boosted the average monthly revenue per paying client to $2,997.

Building strong client relationships and streamlining operations should position them well in the dynamic cannabis market. The company’s cash position also strengthened to $35.7 million.

As more states legalize cannabis and the industry matures, WM Technology’s specialized software solutions could be in high demand. Not many cannabis stocks are profitable, so I have a good conviction. Plus, recovering TTM revenue could send shares higher.

Click to Enlarge

Jewett-Cameron Trading Company (JCTCF)

Jewett-Cameron Trading Company (NASDAQ:JCTCF) manufactures and distributes specialty metal and wood products through its subsidiaries. While not a true penny stock with shares trading slightly above $5, the company’s tiny $19 million market cap should make it count.

Jewett-Cameron is well-positioned to benefit from the ongoing construction and home improvement boom. The company’s Q2 2024 results were solid, with sales up a modest 1.1% to $8.2 million as higher margins boosted gross profits by 7.5%. However, a 25.1% surge in SG&A expenses dragged operating income down 19.3% to $1.1 million.

That said, Jewett-Cameron’s balance sheet remains pristine, with $1.1 million in cash and zero debt. While the business isn’t setting the world on fire, steady demand for its metal and wood products coupled with strong financial health make Jewett-Cameron an intriguing micro-cap to watch. If management can rein costs and capitalize on favorable industry trends, this under-followed gem could quietly deliver a big upside.

On Penny Stocks and Low-Volume Stocks: With only the rarest exceptions, InvestorPlace does not publish commentary about companies that have a market cap of less than $100 million or trade less than 100,000 shares each day. That’s because these “penny stocks” are frequently the playground for scam artists and market manipulators. If we ever do publish commentary on a low-volume stock that may be affected by our commentary, we demand that InvestorPlace.com’s writers disclose this fact and warn readers of the risks.

Read More: Penny Stocks — How to Profit Without Getting Scammed

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.