Despite the market currently undergoing one of the strongest rallies this year, you should still look out for stocks to sell. The market might be cooperating right now, but that’s not helping certain businesses. The headwinds are too strong for many of them to take off. Plus, if we see the market start going the opposite way, these businesses would be the first to go under.

Moreover, it’s always a good idea to exit bad positions and shift that money to better companies. It’s not worth making a contrarian bet on certain stocks that will likely dilute you into oblivion or give you little upside even if they succeed. You’re much better off putting your cash into quality companies that aren’t missing out on the rally.

With that in mind, here are seven stocks to sell:

SolarEdge (SEDG)

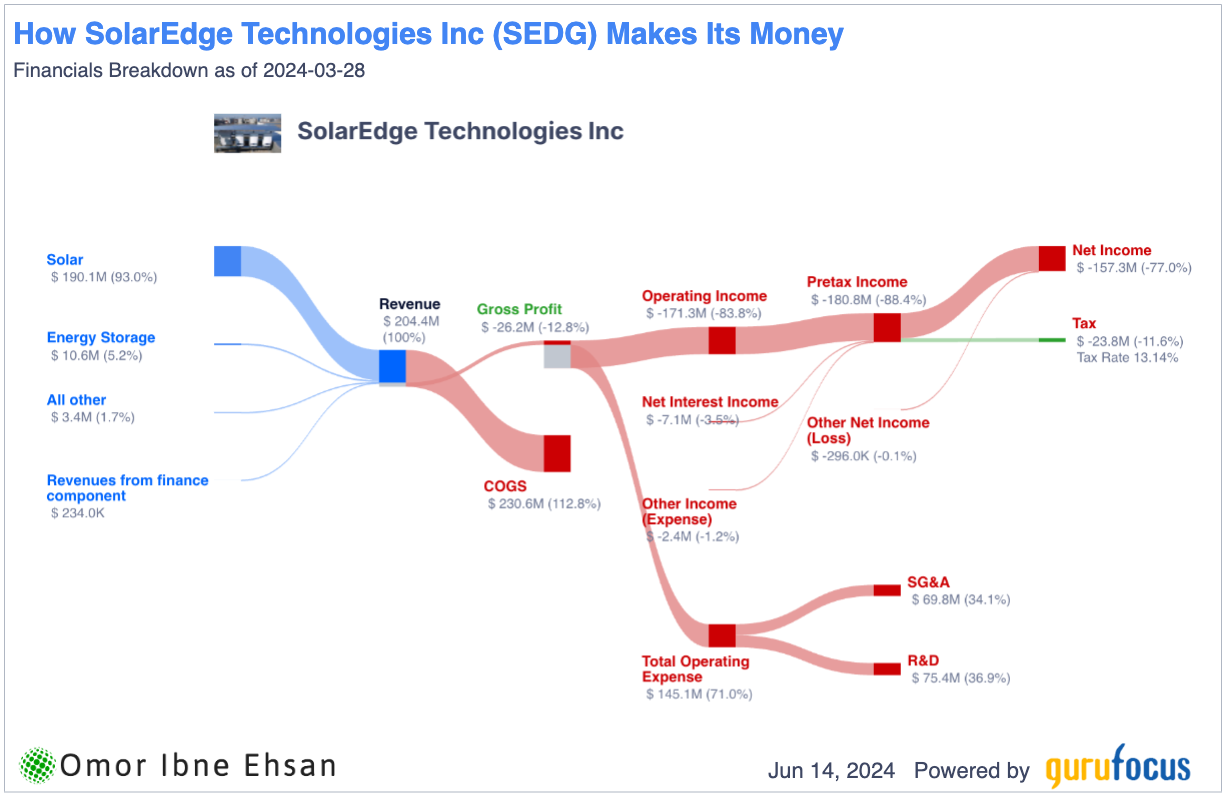

SolarEdge (NASDAQ:SEDG) provides solar power optimization and monitoring solutions. The solar sector has faced intensifying headwinds in recent years that show no signs of abating. In Q1, SolarEdge’s revenue plummeted 78% year-over-year to just $204 million, as solar sales cratered to $190 million. The company shipped a meager 1.1 million power optimizers and 69,000 inverters — a troubling sign of eroding demand.

While management touts growth in the commercial segment and battery adoption, I believe these green shoots will be smothered by the macro challenges plaguing solar. It also has a ghastly -77% net margin.

Click to Enlarge

The painful Q1 miss on the bottom line indicates profitability remains a distant dream. As interest rates stay elevated and competing solar suppliers flood the market, I expect SolarEdge’s woes to compound in the coming years. By 2025, this once-promising solar player may be forced into diluting shares for cash.

Healthcare Services Group (HCSG)

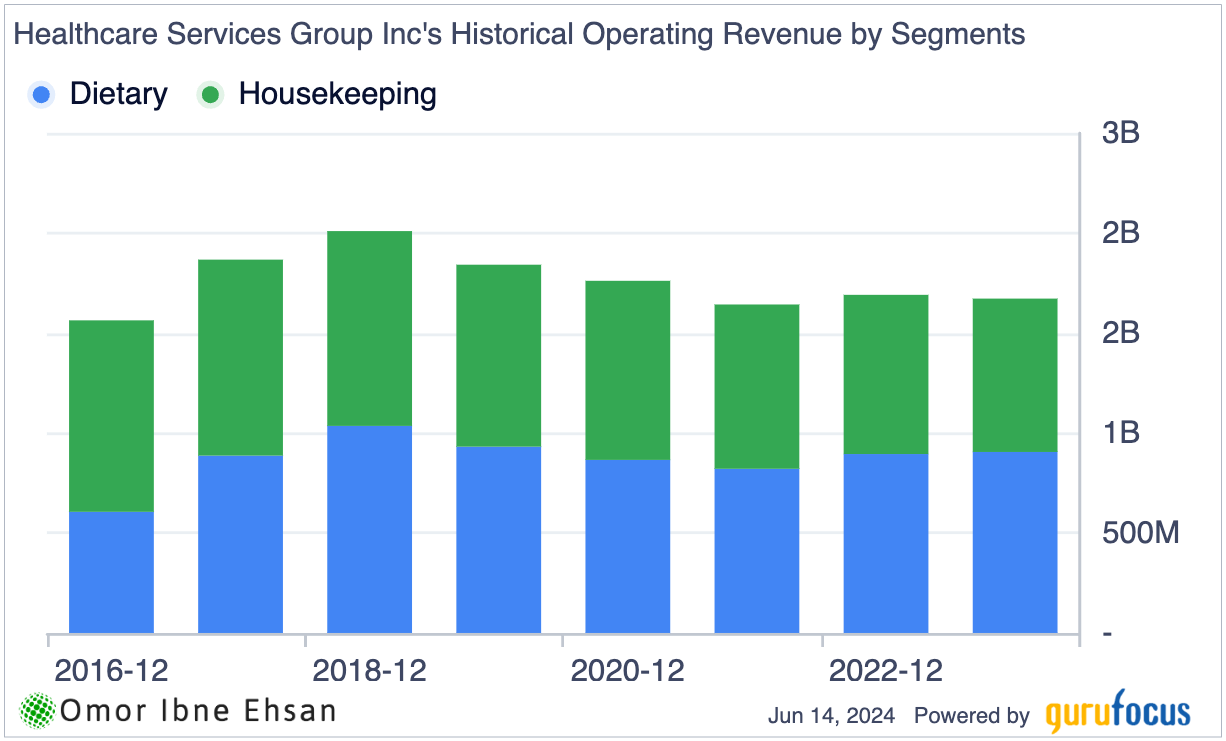

Healthcare Services Group (NASDAQ:HCSG) provides housekeeping, laundry, dining, and nutrition services to the healthcare industry. The company has been struggling since 2017, and I believe its challenges are only intensifying with the new nursing home staffing rule. HCSG has faced a string of negative revenue revisions lately, which is concerning. While management is touting Q1 results as “strong,” I’m not convinced. The 1.5% revenue growth was actually a miss, and cash collections were disrupted by the Change Healthcare cyberattack. The top line has been very boring here.

Click to Enlarge

Sure, HCSG is profitable for now, and analysts predict low double-digit revenue growth. But without a dividend to entice shareholders, I expect the stock to drift lower. There are simply better opportunities out there, in my view, to get more attractive financials and valuations along with a solid dividend yield.

Industry headwinds like inflation, higher borrowing costs, and burdensome regulations aren’t going away anytime soon. I’d steer clear of HCSG shares at these levels and wait for a better entry point when the outlook improves.

Methode Electronics (MEI)

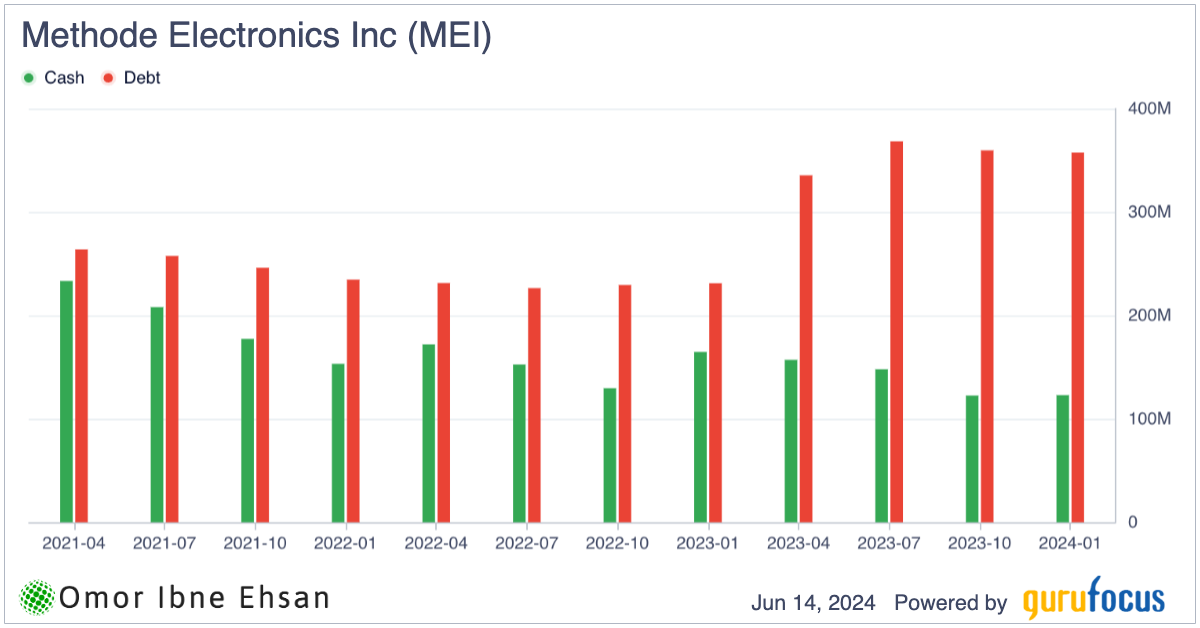

Methode Electronics (NYSE:MEI) manufactures custom-engineered products for automotive, industrial, and other end markets. The company’s heavy reliance on the struggling automotive sector is a major red flag for me. MEI’s Q3 sales declined $21 million YOY to $260 million, missing estimates by a worrying $28.5 million. The sales drop was entirely in the auto segment across all regions due to program roll-offs, EV demand weakness, and operational inefficiencies. Management even admitted that the EV outlook is softening in the near term. Its cash holdings are also going lower while debt is going up.

Click to Enlarge

I expect these auto headwinds to linger and weigh heavily on Methode’s financials. Analysts project revenue will fall 6.4% this year and decline again next year. The company is also suffering from higher new program launch costs that are hurting margins. While MEI pays a dividend, I have little confidence in its sustainability, given the thin margins and quarterly net loss. With auto weakness showing no signs of abating, I believe investors should steer clear of Methode stock. The risks far outweigh any potential rewards here.

PetMed Express (PETS)

PetMed Express (NASDAQ:PETS) sells pet medication, food, and other health products online. While the overall pet market has been thriving, with pet spending in the U.S. rising 7% to $147 billion in 2023, according to the American Pet Products Association, PetMed has utterly failed to capitalize on these favorable industry tailwinds.

The company’s Q4 FY2024 results were dismal, with EPS of -25 cents missing estimates by 25 cents. Sure, revenue grew 6.6% YOY to $66.5 million, but that anemic growth is nothing to celebrate given the booming demand for pet products, especially among younger consumers who are prioritizing pet ownership over having kids.

I see nothing but pain ahead for this stock. The company’s margins are showing no signs of improving. I don’t see any promising trends in this report that could turn things around anytime soon.

Rivian (RIVN)

Rivian Automotive (NASDAQ:RIVN) makes electric vehicles. The company’s first-quarter results may have exceeded its outlook, but I remain skeptical about Rivian’s long-term prospects. With a net loss of $1.24 per share, Rivian continues to hemorrhage cash at an alarming rate. The EV sector as a whole is struggling, especially in the U.S., with most startups perpetually burning through capital while generating lackluster sales.

Despite Rivian capturing a 5.1% EV market share in Q1 and hosting 90% more demo drives, I doubt these initiatives will translate into sustainable profitability. The unveiling of their new mid-sized R2 platform starting at $45,000 seems like a desperate attempt to boost demand in an increasingly crowded market. I don’t think the company will be able to sell those at positive margins.

I believe the company will have no choice but to further dilute shareholders with additional cash raises in the coming years. Plus, if we see a second Trump administration, we could also see EV tax credits and subsidies being rolled back. I’d steer clear of this stock.

ChargePoint (CHPT)

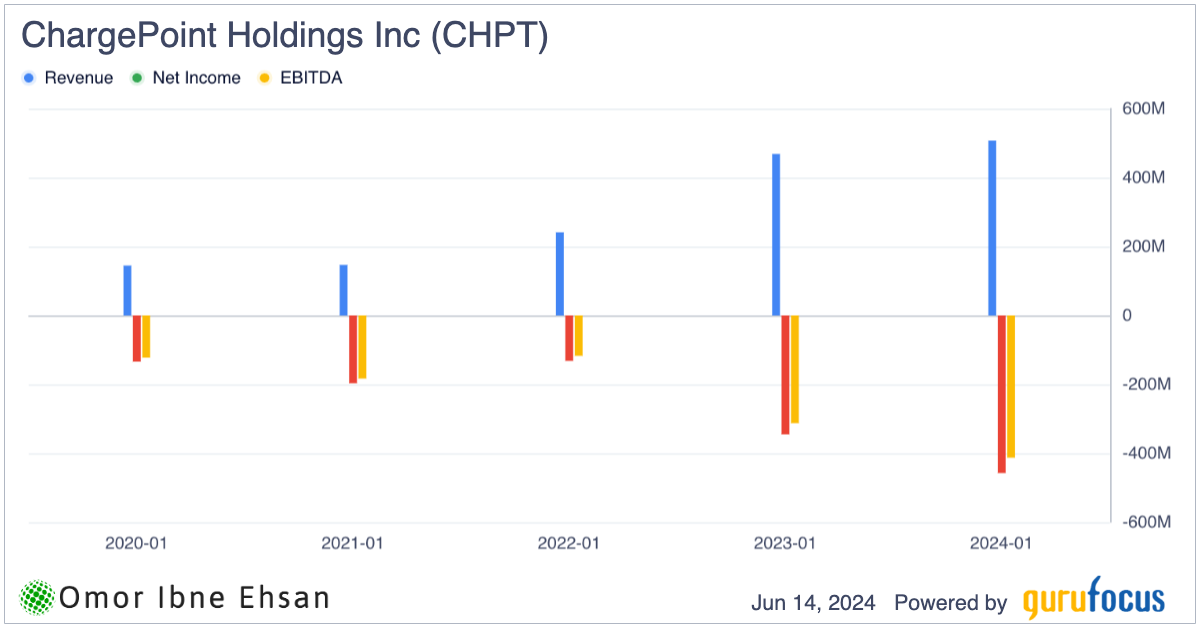

ChargePoint (NYSE:CHPT) provides electric vehicle charging solutions. I’m growing increasingly concerned about the company’s prospects and believe it’s one of the stocks to sell. The entire EV sector is facing significant headwinds, and charging companies like ChargePoint are feeling the brunt of it. With fewer EVs on the road than anticipated and intensifying competition, ChargePoint is rapidly losing market share.

Moreover, the company’s financials paint a bleak picture. In Q1, ChargePoint reported a staggering non-GAAP pre-tax net loss of $45.2 million, and its cash position has dwindled to just $262 million. At this burn rate, I seriously question the sustainability of its business model. Losses are only getting worse.

Click to Enlarge

Management’s talk of achieving adjusted EBITDA positivity by Q4 seems like a pipe dream, given the mounting challenges. Construction delays are already pushing out revenue, and inventory levels are ballooning. Thus, I think it is one of the top stocks to sell right now.

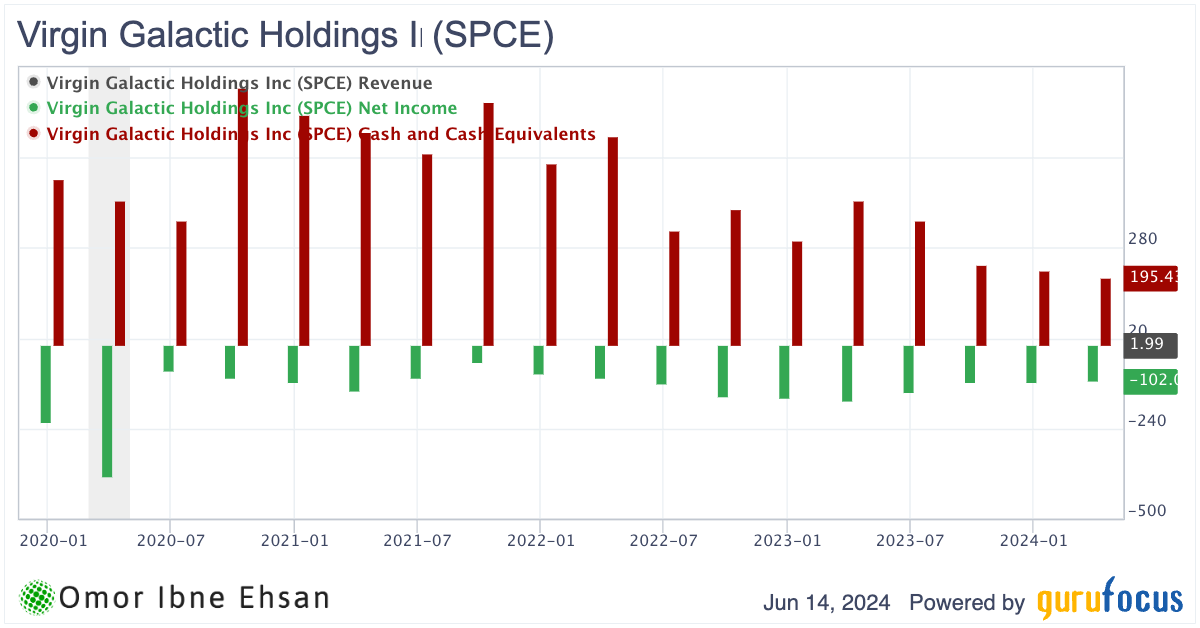

Virgin Galactic (SPCE)

Virgin Galactic (NYSE:SPCE) is an aerospace company that aims to make commercial spaceflight a reality. However, I believe their lofty ambitions may be nothing more than a pipe dream at this point. The stock has been absolutely crushed over the past few quarters as the company hemorrhages cash at an alarming rate. It has been forced to heavily dilute shareholders just to keep the lights on.

Click to Enlarge

While the idea of space tourism sounds exciting, I’m skeptical there’s a large enough market of wealthy individuals willing to shell out hundreds of thousands of dollars for a brief joyride to the edge of space in 2024. Virgin Galactic seems to be far ahead of its time, with many high-net-worth individuals not even aware the company exists.

The recent reverse stock split announcement only reinforces my bearish stance. I wouldn’t be surprised to see Virgin Galactic enter a vicious cycle of endless dilution and reverse splits in the coming years just to avoid being delisted. As such, I think it is one of the top stocks to sell.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.