Unless you’re prepared to lose money, most investors – and even hardcore gamblers – should stay away from JC Penney (OTCMKTS:JCPNQ). Once a proud fixture of the New York Stock Exchange, JCP stock now has the ignominy of trading in the over-the-counter markets due to the underlying company’s bankruptcy. Still, I’ll refer to it by its familiar ticker.

No, I’m not being generous. Frankly, most investors will only recognize the old ticker. As more of a public service than anything, I want this cautionary tale to reach as wide of an audience as possible. While I’d never try to overtly force my opinion on someone, penny stocks can be very dangerous. This is especially the case for novice investors who may conflate a cheap price with a discount.

As you might imagine, I’m not too hot on JCP stock. With the novel coronavirus sparking an economic crisis, now is not the time to bet on risky retail names. Further, the pandemic has abruptly changed the consumer economy at scale. Suddenly, everyone cares about contactless delivery. Unfortunately, that only helps companies like Amazon (NASDAQ:AMZN), not JC Penney.

Still, there is a possible fundamental case for JCP stock. A few years before the present crisis, JCPenney picked up momentum with a surprising demographic: millennial moms. Part of the company’s emerging customer base, this category accounted for 45% of its revenue.

On the surface, this makes sense. Young moms, especially if they’re rearing their children alone, may not have the strongest finances. Plus, kids are expensive for any household. When you factor in the economic impact of the Covid-19 pandemic, JCP stock might seem alluring.

But don’t fall for this trap.

Demographics Is Actually a Harbinger for JCP Stock

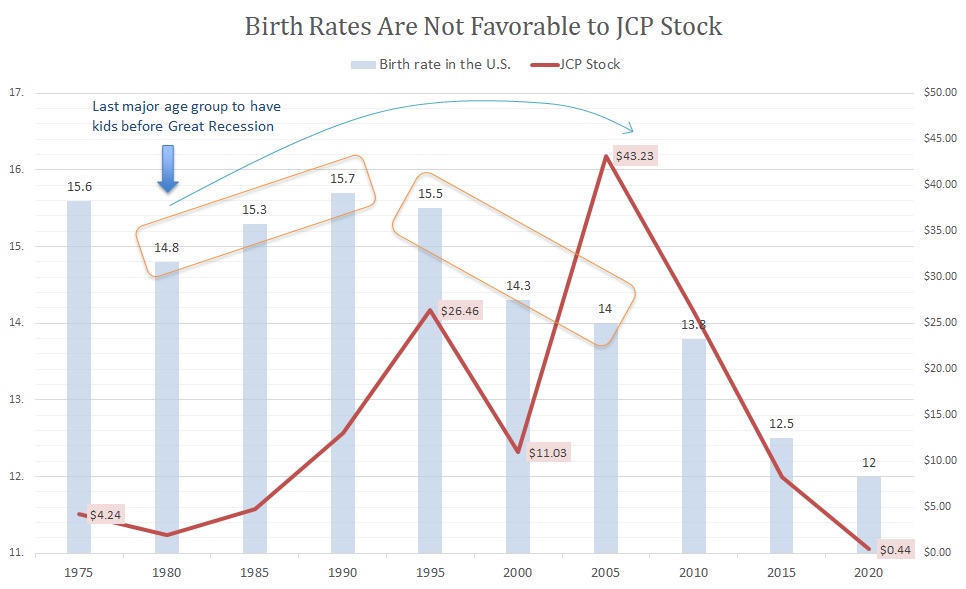

Before I get into my reservations about the demographics argument, let me suggest why this thesis sticks. From the post-World War II period to 1980, birth rates

in the U.S. declined sharply. However, from 1980 to 1990, the birth rate picked up from 14.8 live births per 1,000 people to 15.7.

The years 2000 to 2030 would represent an increase in the population of new mothers based on females born between 1980 and 1990. Therefore, I don’t think it’s entirely a coincidence that JCP stock increased in market value within this time range.

Click to Enlarge

And that may help to explain why JCPenney witnessed a boost in revenue from millennial moms. It’s really simple demographic realities at play.

But by that same token, JCPenney has much to be worried about. Because past 1990, the birth rate has been declining consecutively every five years. Largely, this suggests that whatever sales JCP has gained in recent years represents peak capacity.

Sadly, other factors exacerbate this unfavorable demographic trend. Primarily, the Great Recession took the wind out of the labor force. Of course, this downturn had a pronounced effect on millennials, who are generally behind prior generations in terms of key life milestones.

Not surprisingly, we witnessed a sizable drop in the birth rate between 2010 and 2015. Simply, fewer young families had the means to rear multiple children. Thus, as retailers move forward, they will encounter a smaller consumer base.

Also, the coronavirus is exponentially hurting embattled retailers like JCPenney. With discretionary funds on the decline, there’s just limited space for branded products. Regular, non-branded products will do just fine.

Youth Culture Is Another Challenge for JCPenney

As if JCP stock needed another reason for investors to avoid it, youth culture makes the underlying company irrelevant. Even if JCPenney overcame the declining consumer base, today’s generation just doesn’t care for brick-and-mortar retailers.

After all, we live in the Netflix (NASDAQ:NFLX) era. Yes, streaming is convenient, but it’s also significant in that it’s replacing traditional entertainment platforms. We’re seeing that today with the digitalization of commerce. Further, the new normal incentivizes e-commerce, not physical stores.

However, keep this in mind: JCP is a penny stock, which means it can act irrationally. Thus, don’t be too shocked if shares swing substantially higher for silly reasons or no reason at all.

Ultimately, though, the fundamentals will matter. And JCP stock doesn’t present a good look from almost any angle.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.