If you are looking for explosive upside potential, it is a good idea to look at some dirt-cheap stocks under $10. There are many companies trading at bargain levels and have significant room for upside going forward as they recover and ramp up production.

Of course, stocks look dirt cheap on paper and are not worth buying, but I think the ones I’ll be discussing today have significant upside potential that outweigh the downside risk. These companies also have much lower dilution than many peer companies of a similar size. As such, I think it is more likely for you to land a multibagger with these dirt-cheap stocks:

SkyWater Technology (SKYT)

SkyWater Technology (NASDAQ:SKYT) is a U.S.-based semiconductor foundry that specializes in manufacturing chips for a wide range of applications. I believe this company has tremendous long-term potential as the only American-owned pure-play semiconductor fab, especially given the current geopolitical landscape and the U.S. government’s commitment to bolstering domestic chip production.

While SkyWater’s Q1 2024 results were mixed, with revenue of $79.64 million missing estimates by a narrow margin, the company’s ATS development revenue reached a record $61 million, up 28% year-over-year.

Analysts see a clear path to profitability for SkyWater. Analysts project EPS to skyrocket by 700% between 2025 and 2027, with revenue growth expected to hit nearly 17% this year. With the likelihood of further government support, SkyWater seems poised for explosive upside in the coming years as domestic chip production takes center stage.

Archer Aviation (ACHR)

Archer Aviation (NYSE:ACHR) develops electric vertical takeoff and landing (eVTOL) aircraft for urban air mobility. I believe Archer is making impressive strides in eVTOL development that could position it as an industry leader in the coming years.

In Q1, Archer logged over 100 flights of its Midnight eVTOL, putting it on pace to exceed 400 flights in 2024. Midnight, with a 6,500-pound max weight and 47-foot wingspan, is designed to maximize payload and passenger comfort. The first conforming Midnight for FAA certification is on track to begin flights this year.

Importantly, Archer has invested over $50 million in its supply chain to ensure production can scale efficiently. It also installed a high-volume automated battery pack manufacturing line. As these upfront costs roll off, Archer’s cash burn should decrease meaningfully as it shifts to commercial launch preparations.

While risks remain in this nascent industry, Archer’s $1.1 billion cash position provides a solid runway. Analysts project Archer could generate $5 billion in revenue in 2033. Trading around $3.5, ACHR looks like a bargain with explosive long-term potential if it can execute on its vision. Analysts think the same.

Click to Enlarge

iLearningEngines (AILE)

iLearningEngines (NASDAQ:AILE) is an AI-powered learning automation company for corporate and educational use and I think it’s one of the most under-the-radar AI plays out there right now. In Q1 2024, revenue surged 33% YOY to $125 million, and annual recurring revenue jumped 34% to $479 million. The company reported a net loss of $25.9 million, which was driven entirely by one-time items. Excluding those, iLearningEngines actually increased its non-GAAP profitability compared to last year.

With over 4.7 million licensed users already, this company’s automation solutions have massive potential. As more industries race to automate processes, iLearningEngines’ market opportunity is huge. Yes, losses are a problem at the moment, but analysts expect the company to turn a profit in 2025 and deliver explosive growth going forward. If it can meet those long-term expectations, the stock is trading at just six times the estimated 2030 earnings. That’s pretty cheap for an AI company whose revenue is projected to soar from $540 million this year to $1.2 billion by 2030. Keep this under-the-radar AI play on your radar.

Genius Sports (GENI)

Genius Sports (NYSE:GENI) provides data and technology to the sports, sports betting and media industries. I believe GENI stock still has explosive upside potential despite more than doubling over the past two years. In Q1, the company beat earnings estimates with 23% YOY revenue growth to $120 million. Management also raised full-year 2024 guidance, now expecting around $500 million in revenue.

The rise of live sports streaming is a major tailwind that should drive sustainable growth for years to come. Analysts are projecting revenue to increase another 21% this year and for Genius to turn profitable by 2026. With $73 million in cash, a huge market opportunity, and consistent execution, I’m confident Genius has the runway and resources to deliver on these expectations.

While the stock has already rallied impressively, I think the current valuation remains muted relative to Genius’ long-term potential. If management continues beating targets and capturing share in the rapidly expanding digital sports ecosystem, GENI could certainly be a multibagger winner from here. This is an exciting under-the-radar growth story with plenty of fuel left in the tank.

Vimeo (VMEO)

Vimeo (NASDAQ:VMEO) offers video hosting, sharing, and services. I believe Vimeo stock could have explosive upside from current levels under $5 per share. The company reported strong Q1 2024 results, with revenue growing 1.3% YOY to $104.9 million, beating estimates by $4.6 million. EPS of 4 cents also exceeded expectations by 5 cents.

Vimeo Enterprise showed impressive momentum with major customer wins, while the self-serve segment proved resilient despite pulling back on marketing spend. Profitability is already inflecting, with Vimeo swinging from a $10 million adjusted EBITDA loss just a year ago to a $12 million profit this quarter. Margin expansion potential looks immense as Vimeo optimizes its model.

While Vimeo was once positioned as a distant competitor to YouTube in the crowded video streaming space, the company has smartly pivoted to focus on its unique strengths in video hosting and creation tools. As more platforms crack down on ad-blockers, Vimeo’s ad-free model could become increasingly attractive.

Analysts see earnings surging from 5 cents in 2024 to nearly 60 cents in 2033, but I believe the most compelling upside driver is Vimeo’s potential as an acquisition target.

Gambling.com (GAMB)

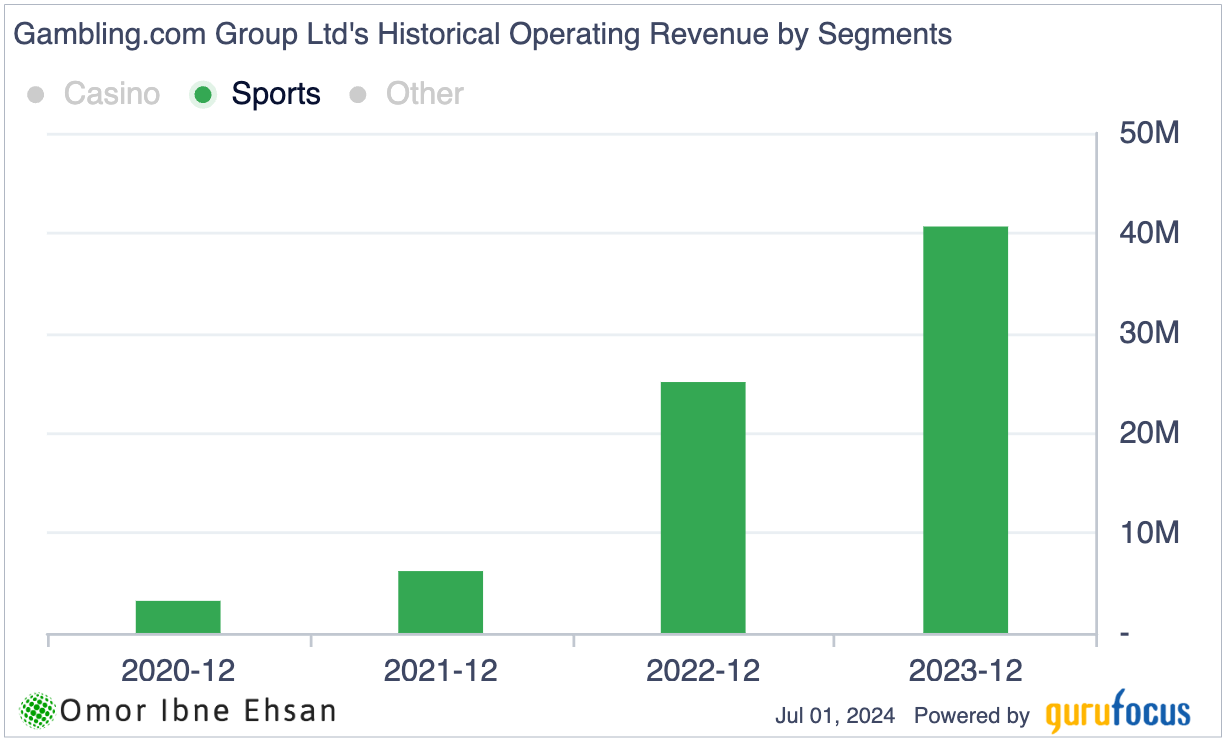

Gambling.com (NASDAQ:GAMB) operates as a marketing company connecting online gambling operators with players. The company reported strong Q1 2024 results, with revenue growing 9.45% YOY to $29.22 million. This performance exceeded consensus estimates and was driven by robust growth across all geographic regions. The sports segment has seen explosive growth.

Click to Enlarge

I believe Gambling.com is well-positioned to benefit from the long-term megatrends of legalized sports betting and online gambling. As more states legalize these activities and younger generations increasingly engage in online gambling, companies like Gambling.com, which acts as a bridge between players and operators, stand to gain significantly.

Despite the stock being down around 47% from its peak, I see substantial upside potential from current levels.

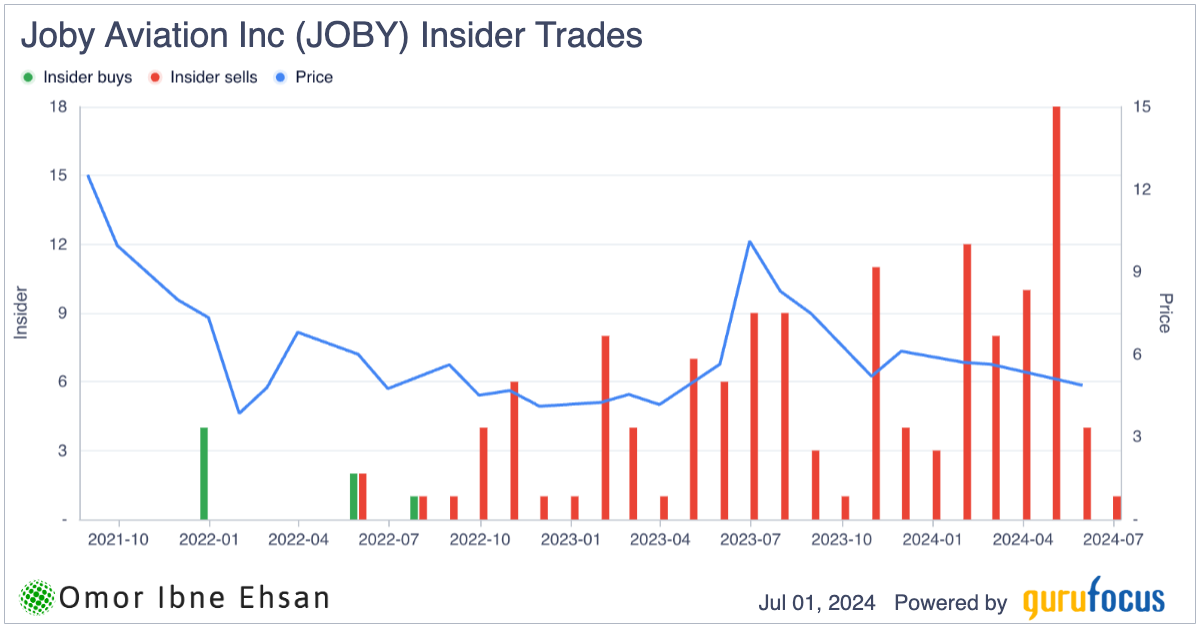

Joby Aviation (JOBY)

In Q1, Joby (NYSE:JOBY) hit a major milestone, becoming the first eVTOL maker to have its final airworthiness criteria published in the Federal Register. The company also began submitting system-level test plans, a key part of stage 4 certification.

I’m impressed by how Joby is executing on an aggressive timeline. Management reiterated their target to launch commercial service in 2025. With over $900 million of cash, Joby has the balance sheet to get there. However, I’m putting this stock on the caboose of this list due to the amount of insider selling. The selling pressure has died down recently, but it is still a little concerning.

Click to Enlarge

Regardless, upside potential remains immense. In addition to an initial U.S. launch, Joby is pursuing lucrative opportunities like cargo delivery for the U.S. military and air taxi service in Dubai.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.