Most people think Silicon Valley was built by entrepreneurs.

Garage tinkerers. Venture capitalists. Risk-taking founders chasing consumer demand.

It’s a comforting story … because it makes America’s greatest tech boom feel accidental… almost inevitable.

But the truth is more useful for investors: Silicon Valley was built on government necessity.

In the early Cold War, Washington couldn’t “wait for markets” to produce the electronics, computing power, and communications systems national security required. So it did what it always does when it can’t afford to lose.

It stepped in … as the first customer, the biggest check-writer, and the ultimate accelerator.

And once that federal demand ignited a feedback loop (guaranteed revenue, clustered talent, scaled manufacturing), entire industries were born… and a handful of early investors didn’t need to guess which stocks would “moon.” They simply followed the flow of government capital.

Now the same playbook is back.

Six decades after John F. Kennedy declared America would go to the Moon – not for science, but supremacy – the United States is launching a new moonshot: the Genesis Mission, a push to fuse America’s top supercomputers, scientific data, and research labs into a unified AI platform.

The signal is unmistakable. We’ve seen five strategic investments in five months:

- Intel (INTC): Revitalizing America’s semiconductor backbone

- MP Materials (MP): A bid for rare-earth magnet control, essential for motors, missiles, and robots

- Trilogy Metals (TMQ): Copper, cobalt, nickel – the nervous system of electrification

- Lithium Americas (LAC): Battery sovereignty

- xLight: Strategic optics play to break foreign supply chain choke points

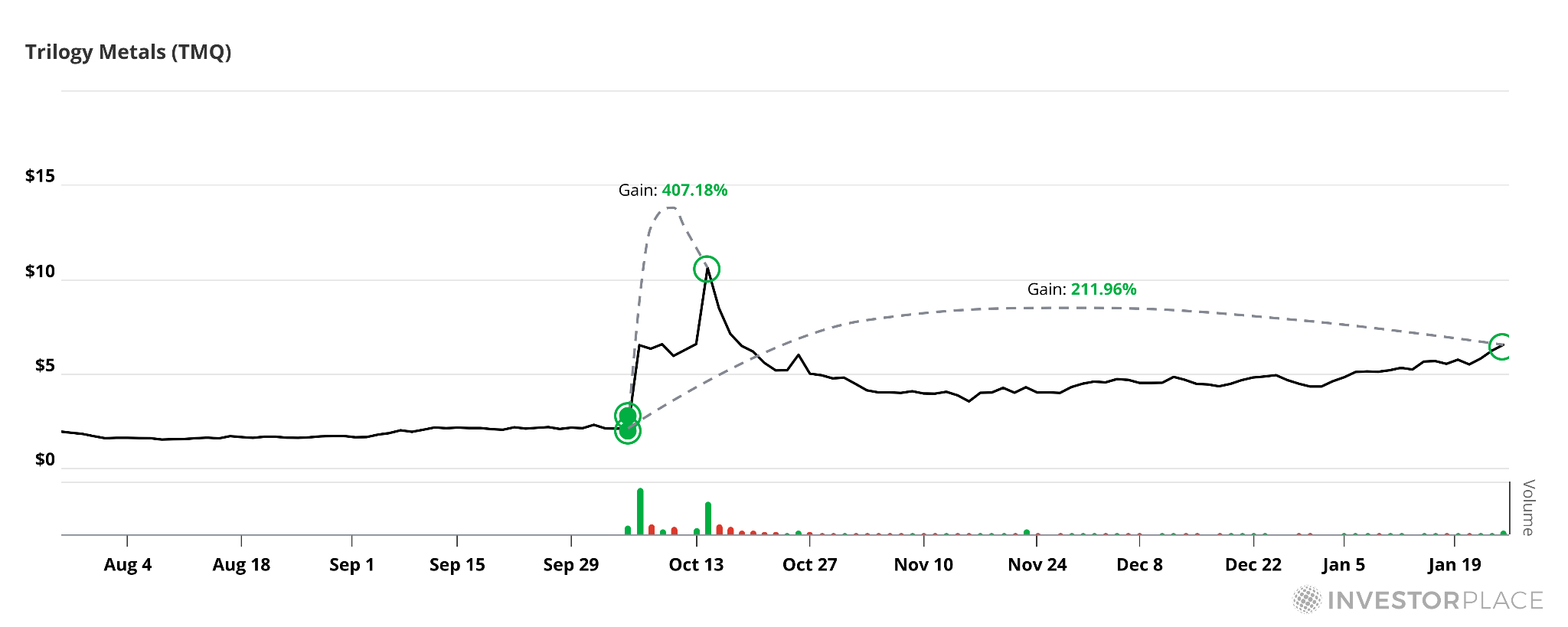

Just have a look at TMQ before and after the Trump administration invested $35.6 million in the company:

From October 6, 2025, when the government invested in TMQ, to October 14, 2025, the stock shot up 407%! Even if you missed that initial surge, it’s still up 200%-plus since.

Industrial policy has become industrial warfare. And it’s shining a spotlight on an industry set to dominate Wall Street in 2026.

Because here’s what they’re not saying out loud…

AI without robots is just ChatGPT.

Control of supply chains, physical production, and the technologies that turn software intelligence into real-world power – that’s the actual endgame. When you map these investments onto the Genesis Mission’s strategic pillars, the government’s grand plan becomes undeniable.

The Genesis Mission: Why Robotics Is the Real Endgame

Here’s the brutal truth the White House has now internalized: AI without robots doesn’t reshuffle global power.

Robots without AI are just basic machines. But AI + robots = production dominance.

Every major Washington priority is tied to robotics. If it hopes to:

- Reshore manufacturing

- Compete with China’s labor scale.

- Offset labor shortages without igniting wage inflation

- Optimize defense logistics, infrastructure security, port automation, warehouse throughput

- And turn America’s AI lead into physical output…

Robots are essential.

And according to recent reporting from Politico, the administration is actively discussing a stand-alone executive order to support the U.S. robotics industry in 2026.

Robotics is being elevated from ‘footnote’ to ‘pillar.’

Robotics as a Core Pillar in the Genesis Mission’s Six Strategic Industries

The Genesis Mission centers on six core industries:

- Semiconductors

- Energy (nuclear + grid + storage)

- Critical minerals

- Advanced manufacturing

- AI

- Robotics / physical automation

And if you’ll notice, robotics is the only one that physically integrates the other five.

Robots need chips, energy, magnets, copper, lithium. They automate manufacturing. They’re AI embodied – the connective tissue of the entire Genesis strategy…

Which is why the idea of a robotics-specific executive order in 2026 matters so much. It’s a declaration that Washington wants a domestic robotics champion class – and is willing to help create one.

And it’s acting with urgency because it’s acutely aware that political time is dwindling. Midterms are looming. Control of committees, budgets, and investigations shifts fast. So, the administration’s incentive is simple: Do as much as possible as quickly as possible.

Lock in programs. Commit capital. Anchor private investment to public support.

Genesis is about irreversibility.

Once factories are built, robots are deployed, contracts are signed, and ecosystems are funded, even a hostile Congress has a hard time unwinding them.

That’s why the pace has accelerated – and why robotics is taking center stage right now

The Robotics Companies Best Positioned to Benefit

If Washington is serious – and the signs say it is – here’s where the upside consolidates.

The Flagship Narrative Name

- Tesla (TSLA): Like it or not, Tesla sits at the intersection of AI, manufacturing, robotics, and American optics. More than just a humanoid demo, Optimus is a political symbol. It’s a robot designed to work in U.S. factories, built by a company already reshoring aggressively.

If the administration wants a visible win – a ‘this is what an American automation looks like’ story – Tesla fits the script perfectly.

Warehouse & Logistics Automation

- Symbotic (SYM): Symbotic is one of the most important robotics companies in America: AI-driven warehouse automation, already scaled, already deployed, already saving labor.

If Washington wants to harden domestic supply chains without blowing up inflation, this is exactly the type of technology that gets subsidized, accelerated, or quietly favored in federal logistics contracts. - Teradyne (TER): Through Universal Robots, Teradyne dominates collaborative robots (‘cobots’): the kind of small- and mid-sized bots American manufacturers can deploy without rebuilding entire factories. If the goal is broad-based adoption, cobots are the fastest way there.

Service & Labor-Substitution Robots

- Serve Robotics (SERV): Serve creates last-mile delivery robots solving real economic problems: labor shortages, urban congestion, service-sector inefficiency. Practical automation.

- Richtech Robotics (RR): Hospitality and service robots to deploy in hotels, restaurants, casinos, and senior living facilities. We see this as the politically palatable version of automation: ‘robots doing the jobs nobody wants.’

Security & Infrastructure Robots

- Knightscope (KSCP): This company builds autonomous security for malls, warehouses, transit hubs, infrastructure, etc. If robotics starts flowing through DOT, DHS, or infrastructure budgets, this category could benefit fast.

The Picks-and-Shovels Layer

Now, here’s where ‘smart money’ often hides: within the critical supplies and materials that a technology needs to function.

Robots need components, like sensors, cameras, actuators, control and safety systems…

Companies like Cognex (CGNX), Keyence (KYCCF), and industrial automation backbone providers such as Rockwell Automation (ROK) quietly ride the wave when robot counts rise – regardless of which brand names win the headlines.

Why 2026 Marks the Inflection Point for America’s Robotics Industry

For years, robotics have been too early. Too expensive. And too clunky.

But the world is different now.

AI is powerful and widespread. Hardware costs are falling. Labor is scarce and expensive. And importantly, Washington is done waiting for markets to self-correct. It’s realized that if the state doesn’t shape the next industrial era, someone else will.

So, yes … 2026 looks like the year robotics breaks out of niche status and into a national priority asset class…

Because power, productivity, and geopolitical leverage demand it.

And when Washington decides something is too important to leave to chance, markets break out.

The smart money doesn’t wait for the official announcement. It positions before the market reprices the entire sector…

The same dynamic is unfolding right now.

The Genesis Mission is reshaping the AI economy behind the scenes … directing capital, accelerating timelines, and backing the companies that matter most to national strategy.

That’s why my team and I have put together a free Genesis Mission broadcast, where I break down how this buildout is unfolding, where the real constraints are, and how investors can position before Wall Street fully prices in what’s happening.

Silicon Valley was not an accident.

And the next great technology ecosystem won’t be either.