As I’m sure you’re well aware now… we’re delving deeper into my favorite time of year: earnings season.

And this week is a busy one, with 165 S&P 500 companies reporting this week alone.

Remember, earnings season is where we find out which companies are growing… and which are not. A good report can boost shares higher, while a bad one can send shares falling…

We’re seeing this trend play out this week. Yesterday, Alphabet, Inc.’s (GOOG) and Microsoft Corporation’s (MSFT) post-earnings declines dragged stocks down on the heels of their lackluster reports, knocking the tech-heavy NASDAQ down 2%.

In today’s Market 360, we’re going to take a look at two big earnings reports this week: Microsoft and The Coca-Cola Company (KO).

Then tomorrow, we’ll review the much-anticipated FAANG earnings, with the last of these stocks set to report today after the closing bell.

Let’s jump right in.

Microsoft Corporation (MSFT)

Microsoft reported its first-quarter results in fiscal year 2022 on Tuesday afternoon.

The company did beat on the top and bottom lines: Earnings of $2.35 per share and revenue of $50.12 billion beat analysts’ expectations for earnings of $2.30 per share and revenue of $49.61 billion.

However, Microsoft missed on revenue forecasts for its cloud divisions and lowered forward-looking guidance.

Regarding the cloud divisions…

Microsoft’s Intelligent Cloud business segment, which includes the Azure and other cloud services, generated $20.33 billion in quarterly revenue, up 20% year-over-year but less than the $20.36 billion estimated.

Microsoft expects $52.35 billion to $53.35 billion in revenue for the fiscal second quarter, which would be 2% growth. This missed analyst expectations for $56.05 billion.

On the earnings conference call, CEO Satya Nadella said that cyclical trends are affecting Microsoft’s consumer business. CFO Amy Hood noted weak demand for PCs in September will continue to hit the company’s consumer segment.

Bottom line: The decline in PC sales and the dollar’s strength – as MSFT is a multinational company that is adversely affected by a strong U.S. dollar – continued to weigh on its profits and growth.

Microsoft shares declined 6.7% in after-hours trading Tuesday and have trended lower since the company’s disappointing results.

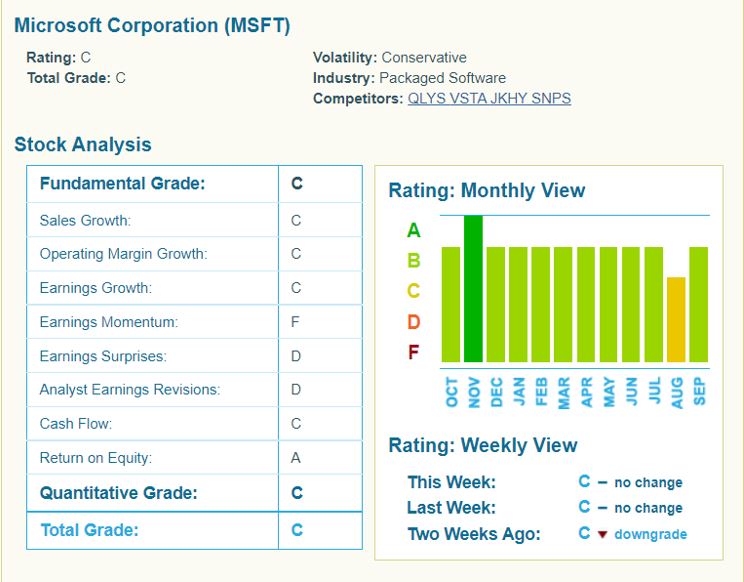

Taking a look at Portfolio Grader, Microsoft was recently downgraded to a C-rating, or a “Hold.”

While my Portfolio Grader isn’t telling investors to run for the hills just yet, it did anticipate caution, as it downgraded MSFT to a hold two weeks ago.

Shares of the tech giant have fallen roughly 25% this year, compared to the S&P 500’s 19% drop. As I shared yesterday in a Special Market Podcast to my Growth Investor readers, the fact is we are seeing a shift away from tech. As such, I would remain focused on companies with growing earnings that are not subject to the affects of the strong dollar.

The Coca-Cola Company (KO)

The Coca-Cola Company (KO) also reported on Tuesday. Coco-Cola reported third-quarter earnings for its fiscal year 2022.

The company reported adjusted earnings per share of $0.69, compared to estimates for earnings per share of $0.64. KO also announced that revenue increased 10% year-over-year to $11.05 billion, beating analysts’ expectations for revenue of $10.52 billion.

Coco-Cola noted that it has had to hike prices to keep up with rising commodity costs and shipping expenses. Expenses are expected to continue to climb in 2023 due to inflation. The company’s executives indicated that more price hikes might be in store in the next 12 months. As a multinational company, the company warned that the strong dollar and foreign currency may way on earnings and revenue next year.

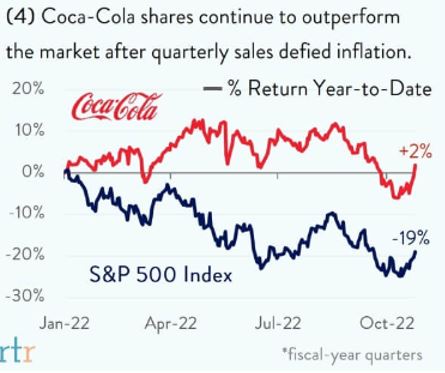

That said, KO’s earnings were certainly a bright spot. Shares closed up 2.3% on Tuesday.

In fact, year-to-date, the company’s shares continue to outperform the S&P 500…

The company currently sports a B-rating in Portfolio Grader and has been in buy territory for the last 10 months.

Investors who acted could have road shares higher… beating the broad market.

The fact is that earnings are working. You just need to position yourself with the companies that will beat in times of inflation and a strong dollar like we’re experiencing now.

This Quarter’s Market Leaders

My Growth Investor stocks are breaking out as market leaders amidst this quarter’s earnings season.

My average Growth Investor stock is characterized by 64.2% annual sales growth and 473.9% annual earnings growth, yet trade at just only 7.2 times median forecasted 2023 earnings.

Furthermore, my average Growth Investor stock is cash rich and boosted their dividend 152% in the past year. In the previous quarter, the average earnings surprise was 31.5%, so I am anticipating another spectacular earnings announcement season for my Growth Investor stocks!

You see, the Growth Investor Buy List stocks largely represent an anti-ESG (Environmental, Social, and Governance) portfolio. CNBC’s Andrew Ross Sorkin and Jim Cramer helped to push ESG stocks, which capitulated last year after Wall Street did a “pump and dump” for the

Rivian Automotive, Inc. (RIVN) and Lucid Group, Inc. (LCID) IPOs that were briefly worth more than Ford Motor Company (F) and General Motors Company (GM), respectively.

Unfortunately, the prices of lithium, nickel and cobalt soared, so electric vehicles (EVs) are now luxury items due to soaring battery costs. It’s questionable if Rivian and Lucid can even find enough batteries to reach profitability. Even Tesla, Inc. (TSLA), with booming EV sales, has been punished for having lowered fourth-quarter sales expectations due somewhat to battery supply complications.

Wall Street’s anti-fossil fuel and ESG push drove energy stocks down to less than 2% of the S&P 500 a year ago.

Today, energy stocks are the best performing sector and now represent approximately 6% of the S&P 500. Within two years, I expect energy stocks will be 30% of the S&P 500 and appreciate 100% per year for the next couple years!

My Growth Investor Buy List stocks are well positioned to continue to profit from the energy and commodity inflation that has enveloped the world. The Federal Reserve is increasing key interest rates to try to squelch inflation, but energy and food inflation continues to rise from ESG policies that are inherently inflationary due to the attacks on fossil fuels and chemical fertilizers.

In this month’s Growth Investor issue, which I will release tomorrow evening, I’ll be sharing an exciting energy stock with a high dividend yield that also sports an AA-rating (meaning it has an A-rating in Portfolio Grader and Dividend Grader), so it offers a solid blend of income and growth. I will also reveal my Top Stocks to act on that are also great bets for new money right now.

To access the issue the moment it’s released, simply click here.

Sincerely,

Louis Navellier

The Editor hereby discloses that as of the date of this email, the Editor, directly or indirectly, owns the following securities that are the subject of the commentary, analysis, opinions, advice, or recommendations in, or which are otherwise mentioned in, the essay set forth below:

Ford Motor Company (F), Microsoft Corporation’s (MSFT), Alphabet, Inc.’s (GOOG)