The “official” start of the fourth-quarter earnings season is now just a few short days away, with the big banks – Bank of America (BAC), Citigroup (C), JPMorgan Chase (JPM) and Wells Fargo Corporation (WFC) – set to kick off the earnings season before the market opens this Friday.

So, in today’s Market 360 I’d like to preview each big bank’s quarterly reports and discuss if they’re good buys before their earnings are released.

Bank of America

Bank of America is expected to announce earnings of $0.77 per share, down 6.1% from earnings of $0.82 per share in the same quarter of last year. Revenue is estimated to rise 10.1% year-over-year to $24.41 billion, up from $22.16 billion a year ago. Analyst earnings estimates have been revised lower by 9.4% in the past three months.

Citigroup

Citigroup is also anticipated to post weak fourth-quarter results: Earnings are forecast to decline 19.2% year-over-year to $1.18 per share, down from earnings of $1.46 per share in the same quarter of last year. Revenue is expected to rise just 5.3% year-over-year to $17.93 billion, up from revenue of $17.02 billion last year. Earnings estimates have fallen by about 7.1% in the past 90 days.

JPMorgan Chase

JPMorgan’s earnings and sales are also shaping up to be relatively lackluster. Analysts are projecting earnings per share of $3.09 and sales of $34.31 billion, compared to earnings per share of $3.33 and sales of $30.35 billion in the fourth quarter of last year. So, earnings are expected to slip 7.2% year-over-year, while sales are expected to rise 13.1% year-over-year. Earnings estimates have been revised higher by 6.6% in the past three months, though analysts have cut their earnings estimates over the past 60 days (from $3.13 per share to $3.09 per share).

Wells Fargo Corporation

Wells Fargo Corporation is forecast to announce the weakest earnings and revenue fourth-quarter numbers. Earnings are expected to drop 49.6% year-over-year to $0.63 per share, down from earnings of $1.25 per share. Revenue is projected to decline 4.2% year-over-year to $19.98 billion, down from revenue of $20.86 billion in the same quarter of last year. Earnings estimates have been revised lower by a whopping 50.9% lower over the last 90 days.

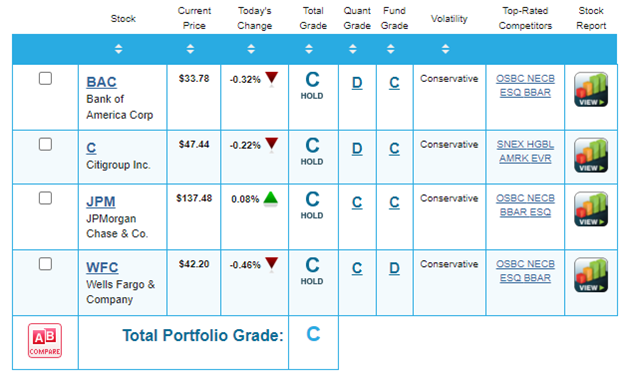

So, should you buy the big banks ahead of earnings? Not according to my Portfolio Grader

. As you can see in the Report Card below, they all hold C-ratings, making them “Holds” right now.

The truth of the matter is the big banks aren’t lining up to report stellar fourth-quarter results, and institutional buying pressure is also drying up, as evidenced by the C- and D-ratings for the big banks’ Quantitative Grades.

The fact that analysts cut their earnings estimates on these big banks is also a red flag, as downward revisions means that earnings misses could be in the cards. And if the big banks’ earnings fall short of analyst expectations, they could get hit hard by Wall Street. I should also add that, according to FactSet, the big banks’ lowered earnings revisions are weighing on the S&P 500’s earnings estimates. The S&P 500 earnings are now expected to fall 4.1%, down from a 3.3% decline last week.

Now, I’ve never been a fan of the big banks. I used to work for a division of the government that is now part of the Federal Reserve. During my time there, I saw how they essentially “cook their books” – and that scarred me for life!

Instead, I’m pounding the table on the energy sector, and for good reason: The energy sector is forecast to report an earnings growth rate of 62.7% in the fourth quarter. Revenue is forecast to come in at 11.5%. Compare that to the S&P 500’s revenue growth rate of 3.8%.

Strong earnings results are important this quarter because we’re in a 15% stock market. Essentially, only 15% of the overall stock market will emerge as market leaders – and those leaders will be the stocks with the strongest earnings and sales growth. As a result, the stock market will grow very, very narrow. Given where the big banks’ earnings estimates stand now, they should not be the leaders. It will likely be energy stocks that lead the market higher.

This is why I’ve been loading up on energy stocks in Breakthrough Stocks. I’ve overweighted my Breakthrough Stocks Buy List with crude oil, natural gas and coal stocks in the past 12 months because the energy sector remains one of the only S&P 500 sectors that doesn’t have negative forecasted earnings growth. As a result, my Breakthrough Stocks Buy List remains characterized by superior fundamentals: 32.3% forecasted sales growth and 182.4% forecasted earnings growth.

I remain so bullish on energy stocks that I am adding another fundamentally superior energy stock to my Breakthrough Stocks Buy List this Thursday, after the market closes. The analyst community is estimating that this energy company will post 101.2% earnings growth in the fourth quarter. And in the past three months, earnings estimates have been revised nicely higher, so a big earnings surprise could be in the cards. The company is slated to release its fourth-quarter earnings results in early February, and positive earnings results could dropkick and drive the stock higher – giving folks who invested in the stock early a nice profit.

Sincerely,

Louis Navellier

P.S. Last week, I released my brand-new Breakthrough Stocks report, The Energy Hypergrowth Portfolio: Five Small-Cap Stocks for Incredible Wealth. In this report, I explain why we are still in the early innings of an incredible rally in energy stocks, and I share the five best energy stocks my system tells me are poised to post extraordinary returns in this energy bull market. Click here for full details.

The Editor hereby discloses that as of the date of this email, the Editor, directly or indirectly, owns the following securities that are the subject of the commentary, analysis, opinions, advice, or recommendations in, or which are otherwise mentioned in, the essay set forth below: