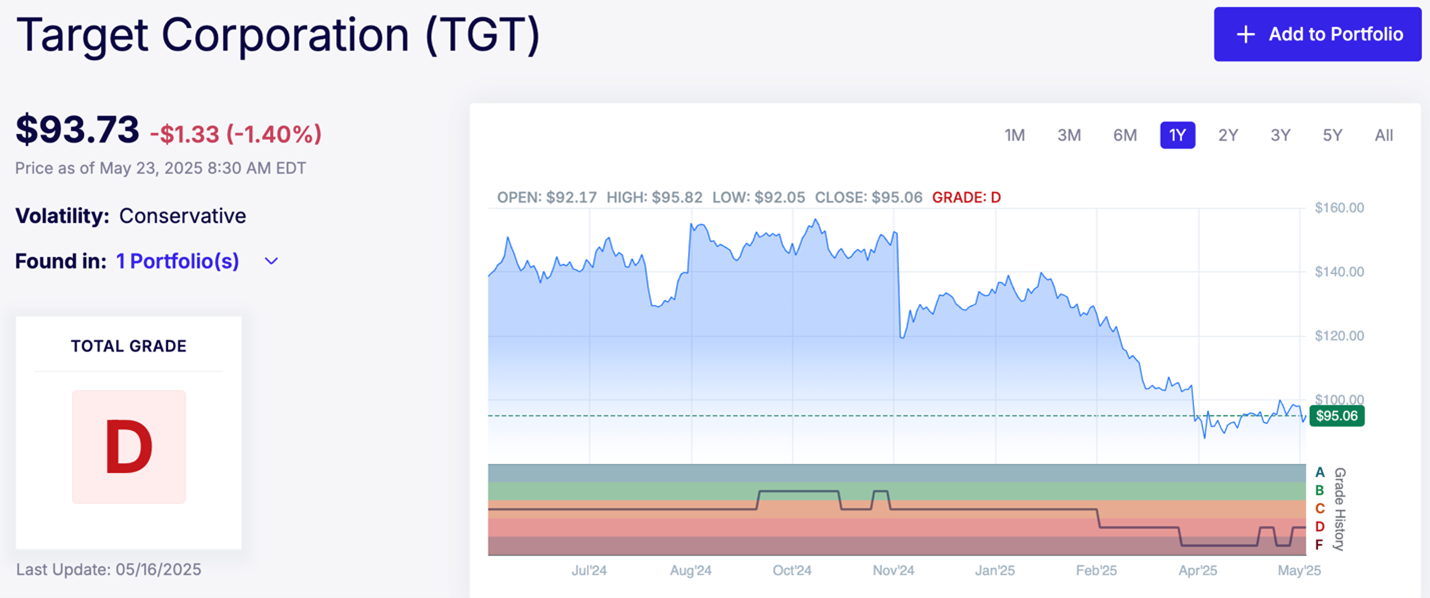

Last Tuesday evening, Target Corp. (TGT) reported earnings… and they basically missed the broad side of the barn.

That’s unfortunate. Target was once a great company and a fantastic stock. Maybe it will be again someday… but I don’t think that’s coming anytime soon.

They’ve lowered their guidance and analysts are slashing their estimates.

While some investors might’ve been surprised by the results and the stock’s subsequent drop, I knew weak numbers were in the offing. My quantitative Stock Grader system tells the tale…

For its Fundamental Grade, Target gets a “C” grade… not good, but not terrible either. But when it comes its Quantitative Grade, it gets an “F.”

That “F” means nobody’s buying TGT… at least nobody with real money. Even if folks are still spending some at the register, there’s no cash from investment banks, pensions, or hedge funds flowing into the stock.

And that gives Target a Total Grade a big, fat “D.”

Naturally, management blamed President Donald Trump’s tariffs for Target’s terrible earnings. And they’ve got a point. Target imports a full 30% of its products from China, where tariffs may be down from their heights, but they’re nowhere near zero… and they’re not going back there either.

But Target’s got a lot more problems than tariffs.

It lost conservative customers in the Obama/Biden era by going too “woke”… and it’s losing liberal customers now after abandoning its DEI ways. Target has alienated customers on both sides of the aisle.

It hasn’t rated well in my Stock Grader system for three years now.

But as investors, the main thing with Target we should be aware of is their same-store sales declined 3.8%. Same-store sales at Walmart Inc. (WMT), by comparison, rose 4.5% in its latest earnings report.

To put it bluntly, Walmart is beating Target. And Walmart, of course, is the largest grocery retailer in America right now, and that’s bringing in a lot of middle-class shoppers.

Plus, Walmart remains the best positioned of its peers to withstand any lingering trade war. Two-thirds of what Walmart sells in the U.S. is “made, grown, or assembled in America,” Chief Financial Officer John David Rainey noted at a recent investor event in Dallas. And much of its imports come from Mexico, which will end up escaping most tariffs.

As you might expect, WMT scores an “A” in Stock Grader… and I recommend it to my paid readers in some of my services.

You might say Target is a victim of Trump 2.0.

Now there will be plenty of winners in the new Trump era. After all, the tariffs were just one part of a broader new policy and economic framework.

And it’s already in motion, even though the media has been playing catch-up. I’ve been calling it Liberation Day 2.0.

And it favors 1) Tax liberation, 2) Tech liberation and 3) Energy liberation. Plenty of stocks are going to benefit from that.

So, in today’s Market 360, I want to give you an idea of what to expect in this new economic regime.

But Trump 2.0 will produce plenty of losers as well.

So, I’ll share the details on one more well-known retailer that my system does not like right now..

A Dramatic Economic Shift Is Coming

There was a time for a few weeks this year when I started to feel like a broken record.

I had been saying for months that President Donald Trump’s tariffs were being used as a negotiation tool to make better trade deals and push the onshoring of manufacturing to the U.S.

In short, I said that most of them wouldn’t be permanent, and that we shouldn’t worry too much.

Once this reality became clear to the rest of the market, we saw one of the sharpest reversals in market history. (Though, like we just saw with Target, there will be some victims.)

Now, while everyone else is digesting what just happened, it’s important to prepare for what’s next… Liberation Day 2.0.

Essentially, we’re talking about a dramatic shift toward economic policy that favors domestic production, strategic resources, and U.S.-centric infrastructure – particularly in areas like energy and AI tech.

That’s great news for those corners of the market. But the truth is some companies are dangerously misaligned with the way things are heading. They’re tied to outdated globalist business models, razor-thin margins, or subsidy pipelines that are drying up.

With the help of my Stock Grader system, I’ve started building a short list of stocks that look especially vulnerable right now. These are not obscure microcaps. Some are well-known names that still carry “blue-chip” reputations – but under the surface, the fundamentals are deteriorating.

Based on what my Stock Grader system is picking up, I believe investors should be especially cautious around four key risk profiles…

The Four Danger Zones

1. China-Dependent Supply Chains

These companies depend on low-cost overseas manufacturing – often centered in China. In a world where tariffs are sticking and reshoring is accelerating, that’s a recipe for rising costs, geopolitical risk, and supply disruption. Margins get squeezed, operations get slower, and valuations often can’t keep up.

2. Low-Margin Consumer Brands

Retailers and consumer-facing names with razor-thin margins are facing a profitability cliff. They don’t have the pricing power to absorb tariff-driven cost increases. And as inflation continues to bite, consumer demand is softening. My system is already picking up on flagging operating margins, declining earnings revisions, and negative trend scores across several of these names.

3. Subsidy-Dependent “Green” Stocks

Companies that depended heavily on environmental, social and governance (ESG) mandates or government subsidies to make their business models work are falling out of favor. With the policy agenda shifting toward energy security and domestic resource extraction, clean-energy names are losing their tailwinds.

4. Globalist Business Models

These are service firms – consulting, logistics, financials – that were built around open-border economics and global integration. But the new policy focus is on American manufacturing, domestic infrastructure, and national resource independence. Many of these “international” operators are starting to look like relics of the last cycle.

Now, let’s take a look at one stock caught in these crosshairs…

Stock to Sell Before Liberation Day 2.0

The company I’m talking about is a perfect example of what I mean when I talk about “Danger Zones” – specifically, the “Low-Margin Consumer Brands” category.

Sure, it’s a well-known name with brand recognition and thousands of retail locations. But under the surface, the picture isn’t nearly as reassuring. My Stock Grader system recently gave it a “F” rating, and for good reason.

Kohl’s Corp. (KSS) has an operating margin of about 3.5%. Profit margins are less than a percent.

Not much room for error when things are that tight, folks.

The company is operating in one of the toughest spots in retail. It lacks the pricing power of premium brands, and it doesn’t have the volume advantage of discount chains.

That leaves Kohl’s squeezed in the middle – and with tariffs potentially driving up input costs, the pressure on margins is only going to get worse.

Even before tariffs entered the picture, the company was struggling with declining same-store sales, falling foot traffic, and ongoing margin compression. The latest earnings report showed a steep drop in profitability, and forward guidance didn’t inspire much confidence either.

I should also add that the company has had some trouble retaining its leadership recently. Essentially, they’ve had a revolving door in the C-suite.

Even worse, institutional demand for the stock is fading. Along with weak revisions, deteriorating cash flow metrics, and a bad macro setup, it’s no wonder the stock earns an F-rating.

In short, Kohl’s is caught in the wrong place at the wrong time – and investors would do well to steer clear.

Don’t Miss What’s Coming Next

Now, I believe most of the changes that will happen will be for the good of the country. But there’s no denying that there will be casualties.

Kohl’s is just one of them. I’ve identified a handful of others that will be caught in the crossfire, too.

The point is the markets are already adjusting. Capital is moving. And the old leaders? They’re being left behind.

That’s why it’s important to get up to speed on what’s coming.

If you want to make sure that you’re well positioned to profit from what’s coming, I hope you’ll join me for my Liberation Day 2.0 Summit on Wednesday, May 28, at 1 p.m. Eastern. You can reserve your space for that free event now by going here.

During this summit, I’ll walk you through:

- The three sectors I expect to dominate during the next phase of Trump 2.0 – and a top-ranked “buy” pick for each sector.

- The sectors I believe will suffer the most as we transition to the new Trump economy – and 10 stocks my Stock Grader system and I say to avoid and/or sell now.

- The strategy I’m using to help my readers target $2,500… $5,000… even $10,000 paydays.

- And details on the Stock Grader system that’s helped me beat Wall Street at its own game for nearly five decades.

If you care about what happens to your money… if you want to stop guessing and start positioning yourself for what’s coming now… Make sure to be there on Wednesday.

Go here to reserve your spot right now.

Sincerely,

Louis Navellier

Editor, Market 360

The Editor hereby discloses that as of the date of this email, the Editor, directly or indirectly, owns the following securities that are the subject of the commentary, analysis, opinions, advice, or recommendations in, or which are otherwise mentioned in, the essay set forth below:

Walmart Inc. (WMT)