Nvidia (NASDAQ:NVDA) stock has been on a mission, surging higher from the March lows. While the novel coronavirus sent the stock market — and NVDA stock — into a tailspin, that wasn’t enough to keep this stock down.

Simply put, Nvidia is a best-in-class company with too many secular growth levers to ignore. The stock has come roaring back because its business remains robust. On its own, that’s enough to justify a surging stock price. But during this climate, it’s even more of a reason.

Some investors will argue that, given our current economic climate, NVDA stock shouldn’t trade with such a full valuation. I would argue the opposite. Because Nvidia continues to churn out magnificent growth, it’s worth an even higher premium as there are fewer growth stocks to choose from.

Let’s look at the company.

Nvidia’s Secular Growth

America watched on as the coronavirus wreaked havoc on China and then on Europe. Once it got here, we were forced into a state of lockdown in most areas, as businesses closed up shop. The stock market plunged as we were in a recession and uncertainty — if measurable — had to be near an all-time high.

The result? Most companies are seeing plunging revenue and a powerful punch to earnings. Think companies like automakers, restaurants, airlines, cruise lines, travel companies and retail.

Nvidia and Advanced Micro Devices (NASDAQ:AMD) are not though, which is why they deserve to be trading so well.

In fact, FY 2021 estimates (this year’s expectations) are actually accelerating. That’s as Nvidia’s end markets like gaming, cloud, edge computing, data center, A.I, etc. are ballooning. The growth here cannot be contained, global pandemic or not. In same cases, like gaming and data center, the company is seeing an acceleration.

Analysts expect revenue to jump 34% this year to $14.64 billion, before growing another 17.5% next year. On the earnings front, consensus expectations call for profit of $8.12 per share. In-line results would translate to 40% earnings growth this year, with estimates calling for another 21.7% growth in FY 2022.

Morgan Stanley analysts

recently downgraded NVDA stock on valuation concerns, although they increased their price target to $380 from $363.

Admittedly, Nvidia trades at a very full 45 times this year’s earnings estimates. But like we said earlier, this stock deserves a premium valuation, because it is a premium company with superior growth.

This isn’t a one-time bump in sales and earnings either, like we see with some coronavirus-related companies. While estimates call for a deceleration next year, this growth is long term and secular, not short term and cyclical.

Trading NVDA Stock

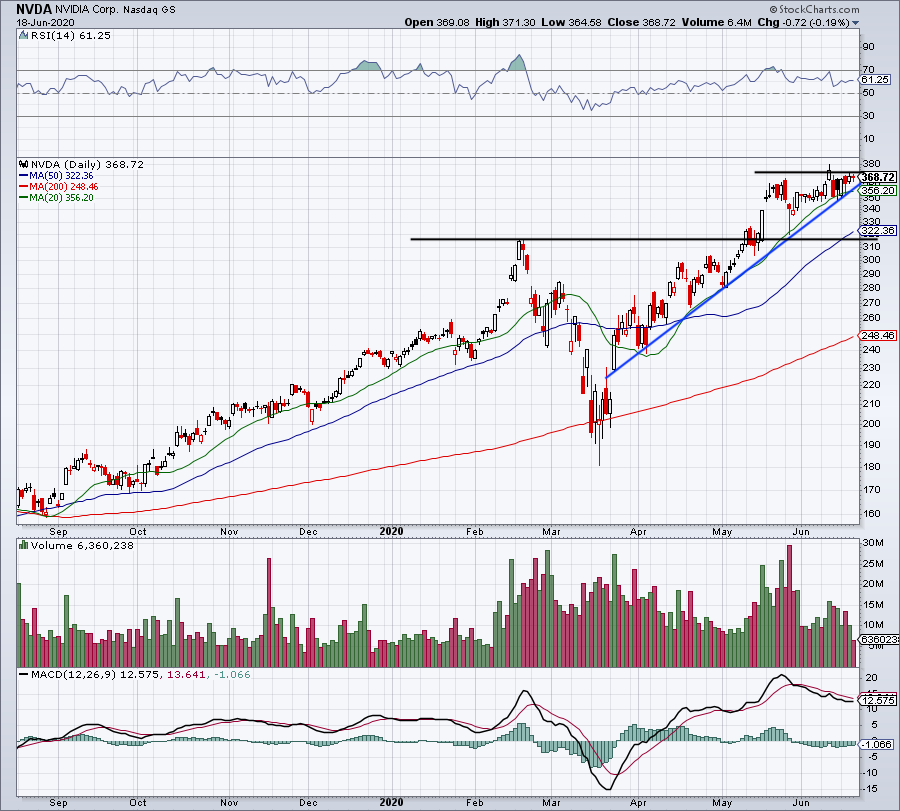

Click to Enlarge

I think investors forget this about Nvidia’s stock. The company reported earnings in mid-February, and the quarter was robust. Shares broke out over $300 for the first time and quickly ran to new all-time highs. That was just before the overall market rolled over due to Covid-19.

Now think about this for a minute: If NVDA stock was ripping to new highs before the coronavirus, why shouldn’t shares be trading even higher while growth is accelerating?

This stock was an absolute steal below $200, as Nvidia has now doubled from its lows.

Shares are percolating just below the $370 level. A rotation over this mark puts the prior all-time high in play at $380. Above that puts the $400 mark on the table. Not only is that a level investors will be gunning for should Nvidia take out the prior high, but it’s also where the 161.8% extension comes into play, at $399.66.

Like every stock, Nvidia is susceptible to a market-wide decline. I mean, just look at what happened in February and March, despite the stock ripping to record highs at the time. But should we get a pullback in the stock, I would view it as a buying opportunity, not a selling opportunity.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.