Nvidia (NASDAQ:NVDA) stock has gone through all of the market cycles. As shares went from $20 to $60, many investors thought it was too much too fast (aka: doubt). Then Nvidia stock eclipsed $100 and as the euphoria phase took hold, NVDA stock was close to $300.

However, that multi-year surge came to an abrupt end in the fourth quarter of 2018. It didn’t help that the Nasdaq was crushed (falling about 20% from peak to trough in less than three months) because of Nvidia’s connection to cryptocurrencies.

Never mind that Nvidia is so much more than just crypto. But at this point in time, it set up the perfect storm to absolutely crush this high-quality company. So with that in mind, let’s take a much deeper dive into Nvidia stock to see if it’s something investors should consider at current prices.

Crypto and Nvidia Stock

Bitcoin exploded back onto the scene in 2017. Prices went from sub-$1,000 in March to more than $18,000 by year end. That type of explosive performance drew in retail and institutional investors from around the world. But its lull hurt more than just crypto investors.

In order to “mine” cryptocurrencies like bitcoin, miners needed powerful computer systems. Specifically, they needed graphic chips from companies like Nvidia and Advanced Micro Devices (NASDAQ:AMD).

Astute speculators connected the dots that Nvidia’s management was either not on the ball with who its actual buyers were or they were not honest with its investors. For the record, I do not believe CEO Jensen Huang & Co. were intentionally dishonest with their investors. Although not being in touch enough to realize that crypto-miners were the real buyers for its graphic chips and not hardcore gamers isn’t exactly a compliment.

Where was the confusion?

Nvidia made crypto-specific chips for miners, separate from the chips intended for gamers. So when bitcoin prices peaked in December 2017 and trended lower throughout 2018, it became more expensive to mine bitcoin than to sell bitcoin. Therefore, miners stopped buying Nvidia’s crypto-specific chips and Nvidia thought they were okay from a revenue perspective.

However, management failed to account for miners buying chips that were intended for gaming but used for mining. Not only did the demand drop-off create a huge deficit in sales, but it also crimped profits, margins and inventory for multiple quarters. The company is still trying to recover from the fallout.

Future of Technology and Nvidia Stock

If you’ve never watched one of Nvidia’s keynote presentations at its GTC events, you’re really missing out. I’ve been fortunate enough to actually attend GTC in the past, so seeing them live really instills a sense of what Nvidia is working on, but they can still be viewed online. They’re usually lengthy, but worth it. (Here’s the keynote from GTC DC, which is only an hour long).

The company’s products play a vital role in the future of technology. Simply put, machine learning, artificial intelligence, data storage, robotics, cloud computing and processing power is changing the way we do everything.

Almost everything that is done today has hard data, whether that’s in autonomous driving, healthcare, ecommerce, agriculture, social media, you name it. In many cases, the data is growing and becoming even more specific. That not only creates demand for storage, but it also creates the need for A.I. to help sort it. Without machines, humans could never parse through this much data effectively.

Not only would humans fail to sort this much data at the rate it’s growing, but they wouldn’t make sense of it, either. A.I. can connect the seemingly random dots into a logical pattern, paving the way to thousands, if not millions of efficiencies.

Artificial intelligence applies computers to do the heavy lifting in a number of circumstances. Companies like Nvidia help power these applications, greatly increasing the efficiency. That efficiency relates to both the time it takes and how much power the application is consuming. Nvidia’s GPUs are vastly superior to its CPU counterparts, and because Nvidia makes the best GPUs, it is a go-to supplier for top tech companies.

Need some examples? There are plenty.

AI and Nvidia Stock

Take healthcare, an area that I am extremely optimistic about when it comes to implementing artificial intelligence.

A radiologist could see 8,000 images in a day. Sometimes the abnormalities they’re looking for are easy to spot, like a broken bone. Other times they can be very difficult. But say we could use an A.I. application to whittle down that list to 1,000 images or 500 images in a day. That not only makes the radiologist’s job easier but improves their accuracy as well.

That’s not to mention the fact that Nvidia’s GPUs can vastly improve image quality as well. Artificial intelligence applications go beyond medical imaging and radiology though. It leverages its power for genomics and bioinformatics, pathology and computational biology, and other fields.

Turning to agriculture, A.I. can be used to drastically cut down costs and boost crop yield. For instance, rather than blanketing the entire farm in harmful pesticides, farmers can use machines equipped with A.I. cameras to determine what’s a weed and what’s a plant. When it’s a weed, the machine can specifically target it with pesticide, resulting in a 90% reduction in pesticide use and giving a 10% boost to crop yields.

Autonomous drones can be used on farms as well, surveying large areas of land to determine what may need more or less of something (such as water). Autonomous drones help other companies too; oil rig operators for example. By using cameras to determine potential areas that need repair before major damage occurs, rig operators not only improve their inspection time by 25% but also reduce their maintenance costs by 25%.

Last but not least, A.I. plays a huge role in social media and e-commerce. I dislike ads as much as the next guys. But when they’re tailored to my tastes, hobbies and recent searches, they are much more relevant to me. We’re going to be served ads and services, so they may as well be applicable. A.I. is also used to connect people, ideas, services and products that are related to the specific user, their purchases, location and other factors.

No matter what the industry, A.I. is being used to improve efficiency and that’s a big benefit to a number of different parties. We need to be careful with A.I., which is still in its infancy and has a long way to go. That bodes well for a company like NVDA, which is powering this technological revolution.

Autonomous Driving and Nvidia Stock

Earlier I mentioned that I had previously attended Nvidia’s GTC events. I was there for the purpose of autonomous driving and seeing what the company was doing within the industry now. Further, I have met with Nvidia’s Danny Shapiro, senior director of automotive, numerous times, ranging from auto shows to autonomous driving conferences. It’s allowed me to glean a lot of information on the industry and specifically what Nvidia is up to.

Many investors and consumers don’t believe autonomous driving solutions will be here anytime soon. Admittedly, it will be some time before a car is capable of driving in any condition in any location completely on its own. But just as Alphabet’s (NASDAQ:GOOG, NASDAQ:GOOGL) Waymo has shown, self-driving functions aren’t all that far away; they’re here right now!

The progress Nvidia’s making in this industry is very important. It’s not just making GPUs or chips that can power an autonomous robo-taxi. The company’s building an entire suite dedicated to the success of autonomous driving and it will succeed for two very simple reasons.

The first? The industry of autonomous driving will succeed. There’s simply too many lives at stake and too much money. Roughly 40,000 people die per year in the U.S. alone from auto-related accidents. An estimated 94% of those accidents occur due to human error. The second reason Nvidia will succeed with autonomous driving? An even simpler answer than the first: It makes the best products.

Building a Suite for Autonomous Driving Products

Its suite includes everything that an automaker would need. Its Drive IX product allows for artificial intelligence in the cockpit. Mercedes-Benz began using Nvidia to power its new MBUX infotainment system in its A-Class and now drivers can find it throughout Mercedes’ line up.

The Drive IX can do more than just be your A.I.-driving assistant though. With eye-tracking, head position and gaze tracking, and facial and gesture recognition, it can incorporate tons of data into the driving experience.

For instance, does the driver turning left through an intersection see the oncoming car from the side? The vehicle can know now and it will be a building block in the future.

The Drive AB2X allows for level 2 driving capabilities. These types of features still require a human driver, but incorporate safety features like lane-tracking, emergency braking, self-parking, etc. These features may not get the love that the fully autonomous fantasy gets, but they are an important building block, as is the previously mentioned Drive IX.

That’s the tip of the iceberg.

Drive Pegasus is an incredibly powerful piece of equipment, allowing a vehicle to become a fully autonomous driving machine. Its power consumption is reasonable considering that it’s capable of generating 320 trillion operations per second.

That generates a ton of data though, doesn’t it? It does, especially when testing an entire fleeting for hours at a time over the course of months and years. That’s exactly what car companies are forced to do, if they want to solve the automation puzzle.

It’s also why Nvidia recently announced its SuperPOD product. The SuperPOD is now one of the world’s top 25 supercomputers and can be set up in roughly three weeks. That’s compared to six to nine months for similar systems. And for those wondering, 22 of the world’s 25 most powerful supercomputers are powered by Nvidia’s GPUs, just to give a sense of what type of high-quality company we’re talking about.

Last but certainly not least is Nvidia’s Drive Constellation. This product is perhaps my favorite given its level of safety and efficiency.

It’s costly, difficult, time-consuming and potentially dangerous to test an autonomous vehicle out on the open road. By using a simulation, companies can cut down all of those “expenses” and drastically improve their efficiency.

Explained simply, Constellation operates as a “hardware in the loop” system. One server runs a synthetic environment in virtual reality, where the tester can make an almost unlimited number of scenarios. Rain, snow, sleet or sun, in the desert or on the coast, during the day, at night or at sunset; it doesn’t matter.

Rather than waiting for the perfect opportunity to test in potentially rare conditions, i.e. with the sun setting at the perfectly uncomfortable angle that can last for just a few minutes, even in optimal testing environments, we can run it on a simulator. The second server runs Nvidia’s Drive Pegasus, which reacts to the simulated VR scenario exactly how it would in real life.

You can see why Constellation is such a promising product. Just earlier this year, Nvidia announced that Constellation is now commercially available.

Nvidia Stock and Autonomous Partnerships

The announcement for Constellation’s availability came alongside an announcement that Nvidia is partnering with Toyota’s (NYSE:TM) Research Institute-Advanced Development in Japan and Toyota Research Institute in the United States. It has continuously upped its partnership with Daimler’s (OTCMKTS:DDAIF) Mercedes as well, either for Robo-taxis or supercomputing vehicles.

Further, Nvidia just announced its deepest partnership yet, with Volvo trucks. The company is “using the NVIDIA DRIVE end-to-end autonomous driving platform to train, test and deploy self-driving AI vehicles, targeting public transport, freight transport, refuse and recycling collection, construction, mining, forestry and more.”

Daimler is working on autonomous trucking solutions as well. It wouldn’t surprise me one bit to see those ambitions being powered by Nvidia (although it’s not yet announced). Nor would it surprise me to see autonomous driving functions in Mercedes’ current consumer vehicles being powered by Nvidia given the work the two companies are doing on an autonomous robo-taxi service.

Only time will tell, but more partnerships are likely down the road as we get closer to making autonomous driving a reality.

Trade War Implications and Nvidia Stock

Coming into May, the trade war had nearly faded to an afterthought. The U.S. and China seemed like they were on a path to an agreement and that all would end well. At the start of May, an unexpected tweet from the President sent shockwaves through the market, as it became clear the two countries were not as close as it had been perceived.

Nvidia stock went on to shed almost 25% in just one month after that. A decline was to be expected, but losing a quarter of its value in just a few weeks was unreasonable. That’s even as Nvidia generates a fair amount of revenue from China and while the trade war is unkind to semiconductor companies in general.

At the G20 summit in June, President Xi and President Trump met to get talks back on track. While there was no trade agreement, none was expected. Instead, there will not be an escalation in tariffs and the U.S. ban on Huawei will be lifted. That initially gave a nice lift to Broadcom (NASDAQ:AVGO), Qualcomm (NASDAQ:QCOM), Micron (NASDAQ:MU) Skyworks (NASDAQ:SWKS) and others.

However, that newly-found optimism was quickly swatted back to reality. Economist Peter Navarro, who currently serves as the assistant to the president, and director of trade and manufacturing policy, provided a bit more insight into the so-called unbanning of Huawei on CNBC. In a nutshell, he said the ban on low-tech components would be lifted, which is good for names like MU, SWKS and Qorvo (NASDAQ:QRVO).

However, where does that leave proprietary, high-tech components? That leaves names like Broadcom, Xilinx (NASDAQ:XLNX) and others in limbo to some degree. Nvidia took a hit with some of its peers, as investors try to sift out what this means for each company’s top and bottom line.

At the end of the day, the trade war will drive the narrative for many semiconductor stocks. Whether it’s fair or not doesn’t matter. In the short to intermediate term, these headlines will matter and make life more difficult for companies like NVDA. But as long as talks don’t disintegrate, this group may be able to resist the urge to plunge lower.

Mellanox Deal’s Implications for Nvidia Stock

In March, Nvidia announced that it will acquire Mellanox (NASDAQ:MLNX) for $125 per share. The all-cash deal valued MLNX at roughly $6.9 billion, with management expecting the deal to close by the end of the year.

Of course, that’s dependent on China too. Many investors will recall that when the trade war was still in its infancy, Chinese regulators went mum on the Qualcomm-NXP Semiconductor (NASDAQ:NXPI) deal.

Qualcomm’s attempt to buy NXPI was a great deal but took forever to get approval. It secured approval from every party but China, a country that simply didn’t say anything about the deal. Eventually, the two companies parted ways and that was that.

The fear for Nvidia is that China will oppose the deal or pull another mime treatment. The hope is that, with recent progress made on the trade front and with the U.S. lifting some of its bans on Huawei, Chinese regulators will bless the NVDA-MLNX deal. Will Nvidia survive without Mellanox? Of course. But the deal is a good one for Nvidia.

Should it close on the deal, management expects that MLNX will immediately be accretive to earnings and free cash flow. An earnings boost is nice, but increasing free cash flow is even better. Further, management expects the deal to be accretive to gross margins.

Increasing profits, increasing profitability, and increasing free cash flow? Yeah, investors want this deal to go through. Not only that, but MLNX will help cement NVDA in the data center, helping build out one of its strongest business segments.

From Nvidia’s press release:

“With Mellanox, NVIDIA will optimize datacenter-scale workloads across the entire computing, networking and storage stack to achieve higher performance, greater utilization and lower operating cost for customers.”

From Nvidia CEO Jensen Huang:

“We’re excited to unite NVIDIA’s accelerated computing platform with Mellanox’s world-renowned accelerated networking platform under one roof to create next-generation datacenter-scale computing solutions.”

Valuing Nvidia Stock Price

For the year, consensus expectations call for earnings of $5.23 per share on revenue of $10.98 billion. Assuming in-line results, this would represent a year-over-year decline of ~20% and 6.2%, respectively.

That’s as the company works through some short- and intermediate-term headwinds. The trade war has caused some issues, as has the crypto hangover. As a result, it’s made NVDA stock seem quite expensive at 30.8 times current earnings. Who wants to pay 30 times earnings for a company that’s experiencing a top- and bottom-line thumping?

Investors are banking on the company recovering in the second half. If it doesn’t, then we may have to start calling management’s judgment into question. But if they do recover, my guess is that investors will flock back to this stock because Nvidia is without a doubt a best-in-breed company. Best of breeds command a premium valuation and for good reason: they have premium products.

If estimates are right, Nvidia will see revenue surge almost 20% next fiscal year to $13.14 billion, driving a 33% boost in earnings to $7.11 per share.

NVDA Valuation vs. Peers

How does that stack up to its competition? Let’s have a look:

| ’19 Rev Growth | ’20 Rev Growth | ’19 EPS Growth | ’20 EPS Growth | P/E | fP/E | P/S | |

| NVDA | -6.2% | 20% | -20% | 33% | 30.8 | 23 | 9.1 |

| INTC | -3.3% | 4% | -7% | 5% | 11.25 | 10.7 | 3.1 |

| AMD | 6.1% | 22% | 41.3% | 57% | 46.5 | 29.7 | 4.8 |

Above we have a look at earnings and revenue growth estimates for this year and next year, as well as a few valuation metrics. Intel (NASDAQ:INTC) lacks any real attractiveness here, at least from a growth perspective. It’s true that it has an attractive dividend yield of 2.6% compared to its peers, but its growth is simply disappointing.

AMD has a great growth profile as it turns free cash flow positive and cleans up its balance sheet. AMD has a long runway for success, but it simply doesn’t make the same caliber of product as Nvidia.

Trading Nvidia Stock

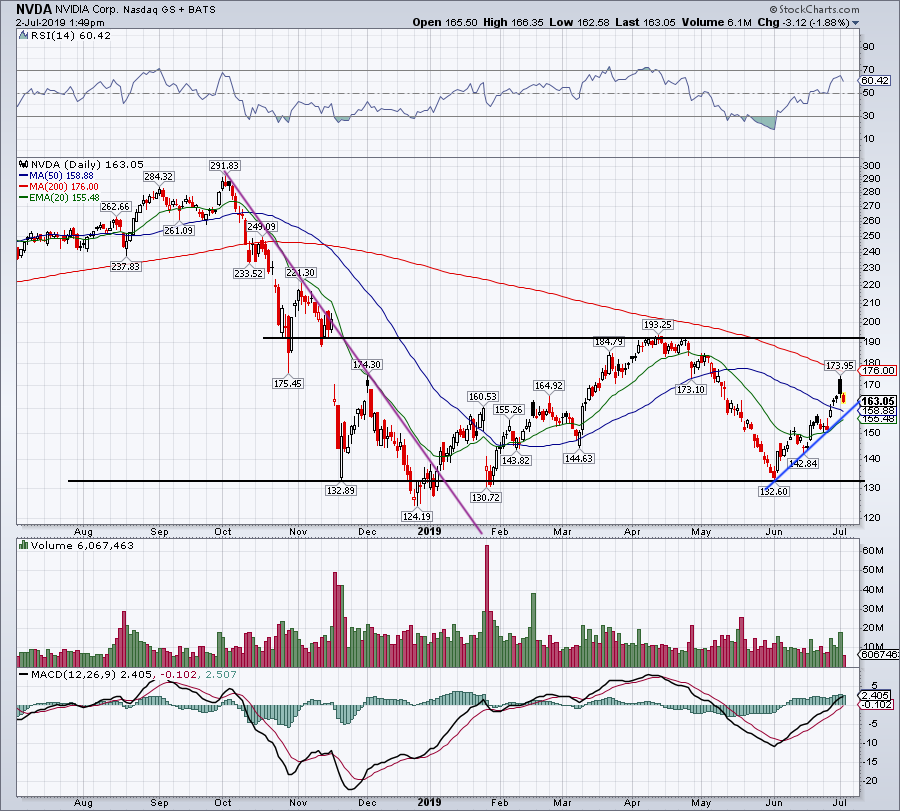

Click to Enlarge

Above is a daily chart of Nvidia stock. We can see how hard shares faded despite the positive G20 summit news. With Nvidia stock starting to pull back, it’s giving investors anticlimactic price action following what should be a more favorable operating environment.

In any regard, bulls will now want to see the 50-day moving average and uptrend support (blue line) hold as support. Should it fail and Nvidia stock falls below $155, a drop back down to recent range support may be in the cards. That comes into play near $132, and can also be seen on the weekly chart below.

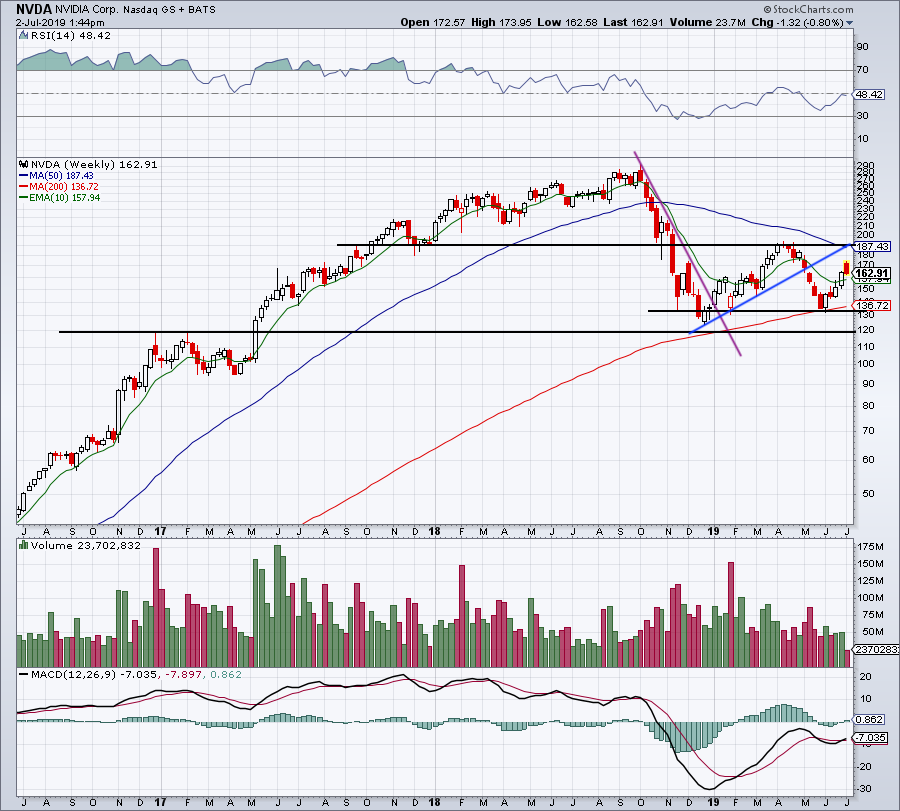

Click to Enlarge

The $190 price is proving to be resistance (noticeable on both charts) while support sits down in the low-$130s. However, on the weekly chart investors will also notice the 200-week moving average. I would expect this moving average to act as significant support should Nvidia stock price fail to hold above its 50-day moving average.

Further, the 10-week moving average is near $158. If NVDA stock can hold above this area, $155 to $158, and better yet, bounce on a potential test, we could see a retest of upper resistance.

On a rally, we need to see if Nvidia can push through the 50-week moving average currently at $187. Further, we need to see if it can get above $190 to $192, which was resistance throughout April. If it can, $200+ is possible, with upside targets of $208 and $228 on the table. Those prices represent the 50% and 61.8% retracement for the one-year range.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AMD, AVGO, GOOGL and NVDA.