Once a dominant leader in the semiconductor space, Intel (NASDAQ:INTC) has suddenly found itself trailing its peers. The company is starved of growth and the performance of Intel stock reflects as much.

Over the last year, shares are down about 6%. In 2020, Intel stock is off almost 19%. Not only does that badly lag some of Intel’s largest peers, but it dramatically lags the overall market.

For instance, the Nasdaq is up 42% and 28% over the same periods, respectively. Intel’s underperformance is startling, and quite frankly, “cheap” just isn’t a good enough reason to be a buyer.

All the Wrong Catalysts

Here’s my issue with Intel stock and it’s a problem that extends beyond the struggling chipmaker. Bulls keep championing the same things: A low valuation, a nice dividend and a legacy semiconductor producer.

I don’t want legacy anything unless there is growth. I want cutting edge with strong and sustainable growth. The low valuation argument is good on paper, but in the real world, it doesn’t hold water. In other words, the higher-valuation stocks are those that are in demand from other investors. That’s because they have growth and the allure of future growth. That’s what Intel lacks. Therefore, Intel stock trades with a low valuation.

The dividend is a nice thing to chew on, with shares kicking out a 2.5% yield. But that 2.5% in annual performance could come in one day’s performance from another stock. The income is decent but that’s not what I’m looking for out of my tech holdings.

I am looking at tech stocks to add growth to my portfolio, not income. If I want the latter, we can fish for it via bonds or utility stocks.

Breaking Down Intel Stock

For all this talk about growth, what does it actually look like for Intel?

Analysts expect 4.4% revenue growth this year, followed by a 2.2% decline in fiscal 2021. The earnings front is even worse, with analysts expecting declines of 0.4% and 2.9% this year and next year, respectively.

If the forecasts are right, 2021 earnings are going to be lower than 2019, while revenue will be up by roughly $1.5 billion or about 2%.

For a tech investor focused on growth, that’s hardly acceptable. Compared to others in its space, it makes Intel look non-existent. While Intel has declining growth, its peers not only have growth, but accelerating growth.

At the end of the day, shares trade at just 11 times earnings, but so what? We need something in the story to give us a reason to buy. Shedding assets isn’t doing it. Buying Mobileye a few years ago wasn’t bad, but it’s not spurring the type of growth we’re seeing in other areas.

While Intel has opportunities in key growth segments — like cloud computing, edge computing and the data center — it’s not capitalizing to the extent I want to see. Meaning that, either companies that operate directly in these segments or Intel’s competitors are reaping the growth from these end markets.

We need to see Intel fire up that revenue growth, but it’s simply stuck in neutral. Gross margins are trending in the wrong direction, although free cash flow and its balance sheet have been improving.

The Bottom Line on INTC Stock

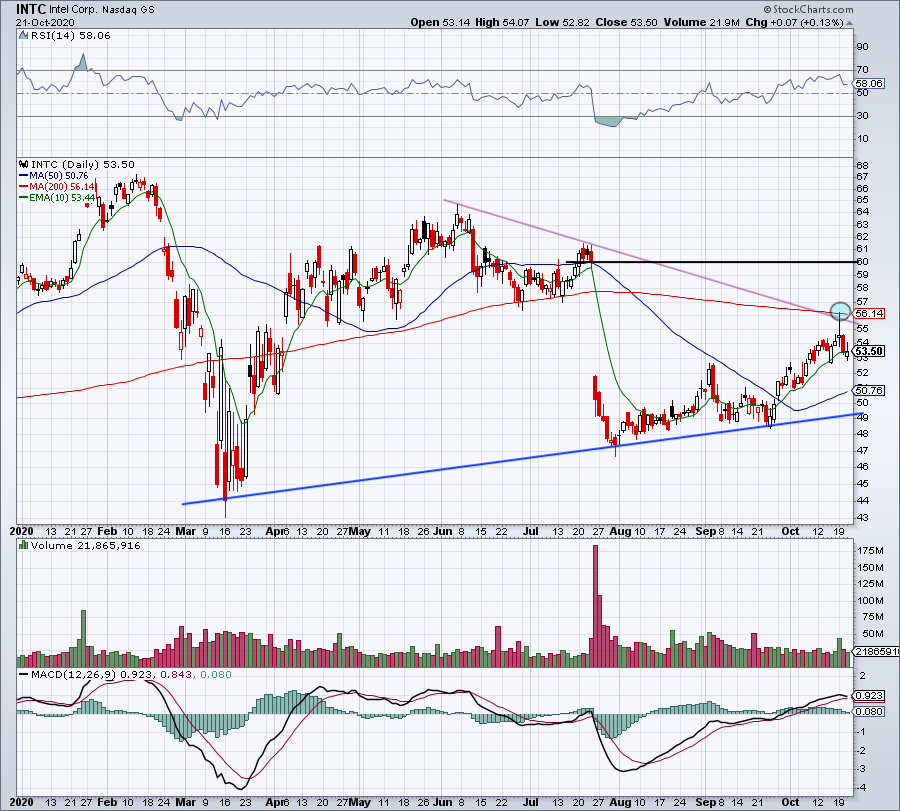

Click to Enlarge

Are there worse picks than Intel stock? Absolutely. Particularly after Intel has already suffered a major pullback in its stock price. At the same time though, there are better picks than Intel out there and that’s where we run into problems.

Not every stock is a buy, but that doesn’t automatically make it a sell, either.

The charts show a similar takeaway as the fundamentals: It’s improving but not attractive. Intel stock is working off that hideous gap, where shares plunged from $60 to almost $50 in a single day. It then proceeded to fall for the next five days before bottoming.

It’s been improving, having filled about half of its gap, but how far can it really go without a catalyst? We’ll see if earnings can change the rhetoric with this one or if it just makes things worse (like last quarter).

On the date of publication, neither Matt McCall nor the InvestorPlace Research Staff member primarily responsible for this article held (either directly or indirectly) any positions in the securities mentioned in this article.