The economy is accomplishing what Prohibition failed to do — stopping people from drinking. For the first time since official records were kept, global alcohol sales dropped.

According to research firm Euromonitor International, the volume of alcoholic drinks consumed dropped by 0.7% last year. The last time people sobered up on a mass-scale was back during the Asian financial crisis of the late 1990s. Can an industry long considered recession proof overcome these latest challenges?

It’s important not to understate what just happened. In the nearly two decades tracked by Euromonitor, we have experienced a banking crisis, a housing crisis, a commodities crash and a global economic meltdown. Yet, in the years that these events unfolded, alcohol consumption rates remained positive. There is, however, evidence of a cumulative effect. Alcohol consumption peaked in 2006, and has trended sharply downward. Rather than being a one-off incident, the 2015 drop-off is the culmination of a long building trend.

However, the news isn’t completely bearish for alcohol stocks. Top-shelf drinks, such as premium English gin, have risen sharply in popularity. These refined drinks happen to be popular with millennials, a demographic that will continue to grow in purchasing power. That means two things — first, alcohol stocks as a broad sector are in trouble. However, those that are positioned to advantage shifting consumer trends have an opportunity to do well.

Here are four alcohol stocks — two to tap, and two to avoid.

Alcohol Stocks: Ambev SA (ADR) (ABEV)

Of all the alcohol stocks traded in the markets, Ambev (ABEV) is likely the best suited to tackle any challenge affecting the broader industry. Although headquartered in Sao Paulo, Brazil, ABEV has a vast product portfolio that is difficult to ignore.

In addition to distribution rights to several popular beer brands, it also offers carbonated soft drinks under household names such as Gatorade, Monster and Pepsi. In fact, Morgan Stanley and especially UBS voiced their approval of ABEV.

When you look at Ambev’s financials, it’s easy to see why Wall Street analysts are pumped, despite underlying problems in Brazil. With sales being challenged everywhere, ABEV has been focused on profitability and internal efficiencies. Their double-digit operating and net margins beat out a vast majority of alcohol stocks. Over the past few years, ABEV has been cutting down on its capital expenditures to combat a slowing global economy. Finally, ABEV runs an asset and cash rich balance sheet — an increasing rarity these days.

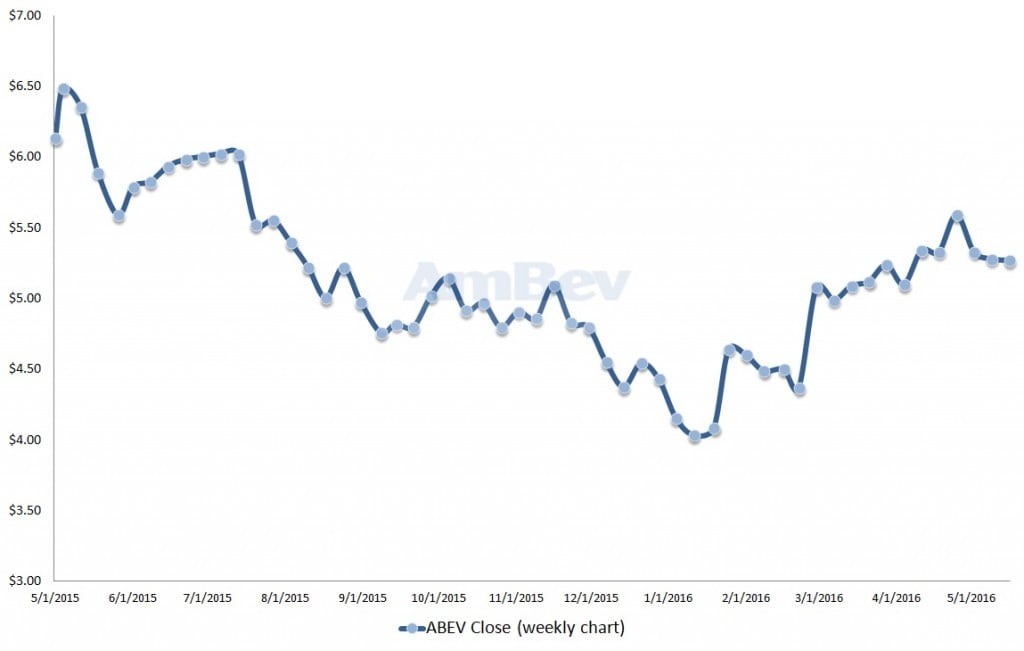

If there’s any doubt to the strength of ABEV, you just need to look at the technical picture. Year-to-date, shares are up 15%. That’s a significant boost from the presently lackluster U.S. markets. Better yet, ABEV is a stock in recovery mode. Three years ago, shares were chasing the $9 level. Theoretically, that suggests ample room to run for ABEV before it would be considered overbought.

With a vast chunk of investors freaked out about anything to do with Brazil, ABEV is a contrarian trade that fundamentally makes a lot of sense.

Alcohol Stocks: Brown-Forman Corporation (BF.B)

Whenever an industry faces a sales headwind, it’s usually a good idea to think big. Smaller companies simply won’t have the capital resources to weather a persistent storm. Industry leaders, on the other hand, have a range of options, including unloading less desirable businesses.

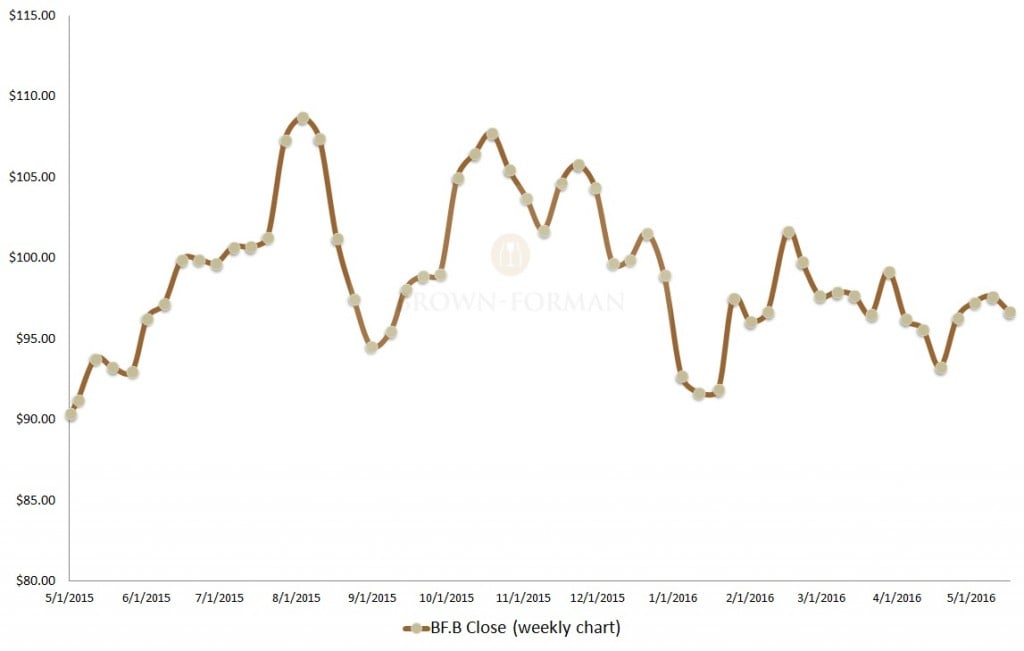

That’s one of the primary selling points for Brown-Forman Corp. (BF.B). With premium brands such as Jack Daniels and Woodford Reserve under its belt, BF.B is here to stay — regardless of what happens to other alcohol stocks.

Aside from its portfolio, smart management is what really separates BF.B from the crowd. According to insiders, Brown-Forman is considering selling its vodka brand Finlandia. The move would make sense for a number of reasons. Vodka is a crowded, competitive market. Whiskey, however, is Brown-Forman’s forte. Selling Finlandia shores up some cash, and allows better streamlining for the core business of BF.B.

In addition, vodka isn’t quite what it used to be. The Russians are apparently drinking less of it. Whiskey also became the most popular spirit globally last year, according to Euromonitor. For BF.B specifically, the company reached an agreement to buy The BenRiach Distillery Co. for approximately $415 million. The purchase will add three Scotch whiskey brands under the BF.B umbrella, further solidifying the company’s reputation as the king of whiskeys. At this point, Finlandia is an unnecessary third wheel.

Among pure alcohol stocks, BF.B has the right product mix to continue pouring profits.

Alcohol Stocks: Compania Cervecerias Unidas S.A. (ADR) (CCU)

When it comes to alcohol stocks to avoid, Compania Cervecerias Unidas S.A. (ADR) (CCU) comes readily to mind. It’s not so much that CCU is a poorly run organization — clearly, there are many more names that would fit the bill.

But one of the first rules in business is location, location, location. To that end, CCU worries me. Judging from the mixed reception by Wall Street analysts, I’m not alone.

The problem comes down to exposure to specific Latin American markets, from where CCU primarily generates revenue. For example, in Compania’s home country of Chile, long-term alcohol consumption is trending downward. In addition, on a per-capita basis, Chileans drink less than neighboring Brazilians and Argentineans, according to data from the World Health Organization. That’s great news if you’re a street preacher. But it’s not so great if you’re invested in alcohol stocks that depend on these drying markets.

The plight of CCU is fairly evident when you look at both its financials and technicals. Although sales for CCU are trending up, each dollar is working much harder to move inventory. Operating margins are good, but are off from prior highs. Net margins are marginally better than the competition. Wall Street has taken notice and responded accordingly. CCU is down 4% YTD after a promising rally in late-February. Even worse, CCU is down 7% so far in the current month, and its trajectory suggests further pain down the road.

Alcohol stocks already face an uphill struggle. CCU just makes that journey unnecessarily more difficult.

Alcohol Stocks: Boston Beer Co Inc (SAM)

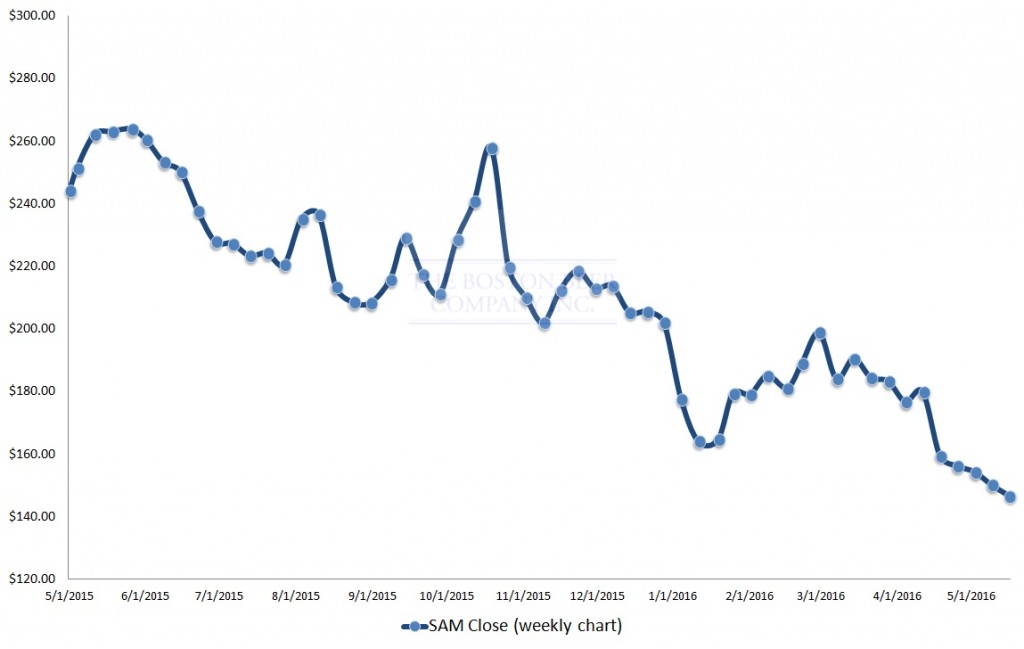

This is the one that hurts. On paper, Boston Beer Co. (SAM) seem to have all the right components to make it a strong contender among alcohol stocks. A well-run, cash-rich and focused company, SAM has won multiple industry awards for its Samuel Adams brand.

Company founder Jim Koch is also a true American patriot who has long resisted buyout talks from foreign conglomerates. He even testified before a Senate Committee regarding the challenges faced by American businesses due to onerous taxation laws and the multinational redcoats exploiting them.

Jim Koch and SAM are the good guys. Of course, Wall Street doesn’t give two cents about any of it. They just want to see stupendous growth. Unfortunately, this is one area where SAM is starting to show some vulnerabilities. Between 2007 and 2014, revenue growth for SAM averaged 16%. In 2015, sales were just shy of $960 million, or a comparatively small 6% increase from the prior year. Also, the most recent two quarters saw a decrease in year-over-year sales growth.

The sudden underperformance against historically high standards, along with the general bearishness affecting alcohol stocks, was simply too much for SAM. Shares are down sharply from last year’s record highs, and the negative sentiment continues unabated. On a YTD basis, SAM is down 27%. Not surprisingly, on the day of the global alcohol sales news release — on Friday the 13th, no less — SAM stock dropped nearly 4%.

Investor panic toward SAM is, in my opinion, overdone. That said, arguing with the herd will get you run over.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.