It seems like Fitbit Inc (FIT) can’t get any respect. Despite being overwhelmingly profitable for the first quarter of fiscal year 2016 — trouncing earnings expectations by over 257% — Fitbit stock dropped a shocking 19% the following day.

What makes the panicked selloff all the more remarkable is that FIT has always produced solid earnings reports.

Counting the latest result, FIT stock averages an earnings surprise of more than 150%. In fact, Q4 fiscal year 2015 has been the only time so far that the wearable technology company has failed to beat consensus by triple-digit margins.

So, What’s Going on With Fitbit Stock?

While FIT continued to impress in both earnings and revenue, Wall Street was rather disheartened by the guidance for the current quarter. Management disclosed their own expectations for Fitbit stock to earn between 8 cents and 11 cents, far below analysts’ consensus of 26 cents.

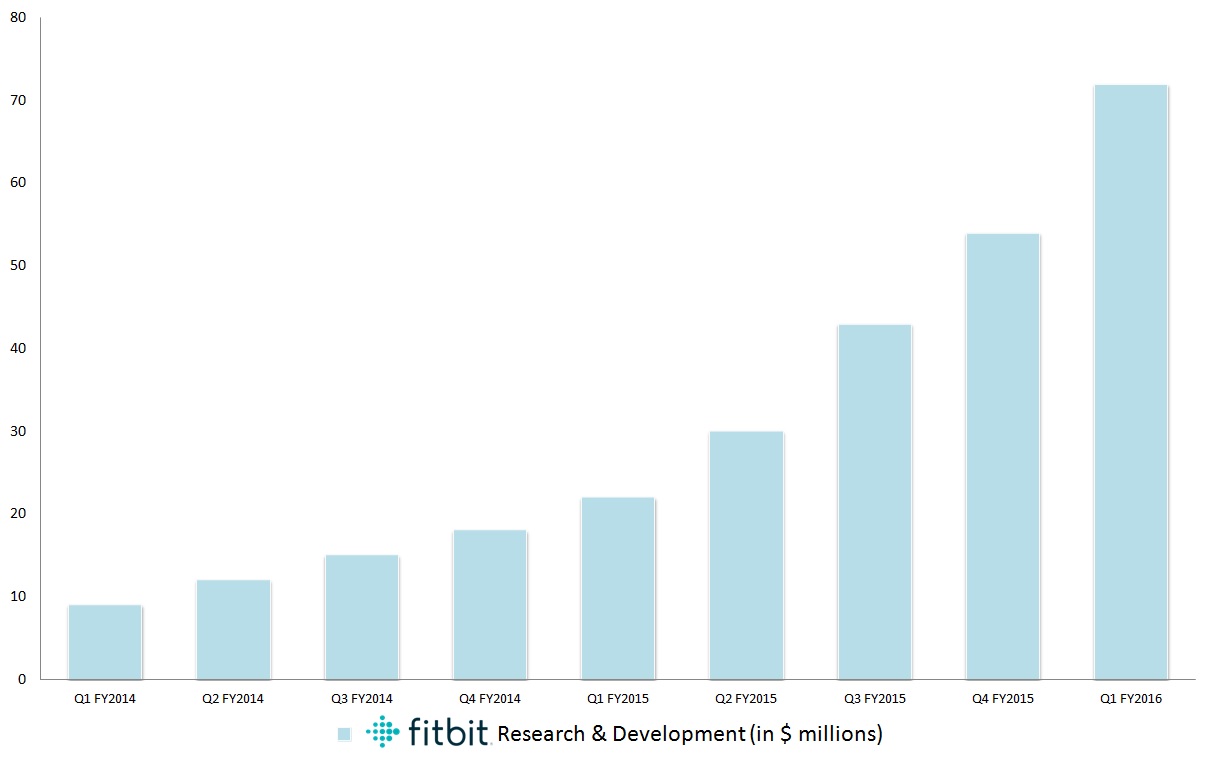

However, what traders apparently failed to acknowledge was why the outlook was negatively adjusted. FIT is ramping up its research and development, and that will drive down margins through increased costs. However, in order to stay competitive in a cutthroat industry, this is a smart move — and Fitbit stock should be the ultimate beneficiary.

What’s just as surprising as the bearish response to FIT stock was why so many investors were caught off guard.

Click to Enlarge

It’s no secret that CEO James Park has a long-term strategy for the tech company. And he practices what he preaches. Over the last four years, Fitbit stock has seen a 115% growth rate in R&D costs. Within the same time frame, we’ve also seen a 194% increase in revenue. You can’t have your cake and eat it too.

That aphorism is particularly appropriate when we consider gross margin. One of the primary reasons why people should consider Fitbit stock is the organization’s ability to charge a healthy premium over real and perceived differences against competing products.

Since 2012,

gross margin has jumped to 49% from 35%, or a 40% increase. Simply put, FIT is able to dictate terms when it comes to pricing. That’s the beauty of being a market leader. But to stay there, it costs money.

Just look at Apple Inc. (AAPL). Apple has revolutionized the digital era, introducing the iPhone, iPad and a slew of other addictive electronic products. But as an innovator and disruptor, AAPL knows better than anyone what it takes to stay on top.

Since 2010, Apple’s R&D costs grew an average of 35%. Sales, on the other hand, grew at 34%. Generally speaking, revenue increased by the largest margin when Apple amped up their innovation expenses. Mr. Park is taking cues from the best in the business — and it doesn’t make sense that Fitbit stock should suffer because of it.

This isn’t just about analyzing the financials. FIT stock also has technical strengths that one should consider.

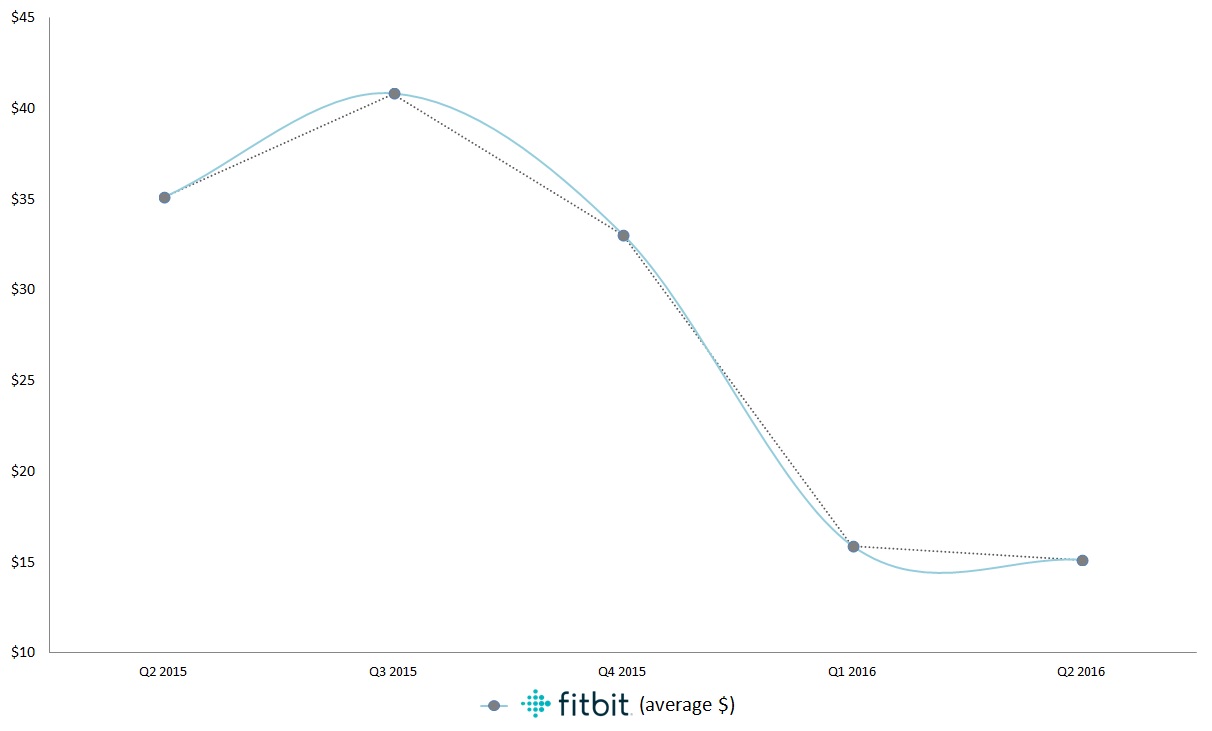

Click to Enlarge

The most obvious bullish factor is that shares have yet to breach critical horizontal support decisively at $13. There have been a few trades where Fitbit stock ended up in $12 territory in late-February of this year. Yet FIT stormed quickly upwards and those that timed the move made a handsome profit.

On a longer-term scale, it seems like the worst of the volatility is behind Fitbit stock. Between Q2 and Q4 of last year, FIT stock averaged $36.33. For the first half of this year, shares are averaging $15.50 despite a number of steep selloffs.

With new products down the pipeline, the risk appetite could change drastically for the company, especially if they continue to outperform against commonly viewed financial metrics. Needless to say, this would be a net positive for Fitbit stock.

In some ways, the harsh treatment of FIT shares is understandable. They’re a very young company in a competitive and whimsical industry. To some, Fitbit stock hasn’t yet earned respect. However, those that feel that way may not be seeing the bigger picture.

Rather than chasing pretty statistics, the company is aggressively investing in itself. That’s turning off fair-weather investors that want a big jump right now. But for those with a little patience, FIT stock could be a serious winner.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.