The retail sector was a big surprise last week as several department stores exceeded earnings expectations. As a result, companies like Macy’s Inc (NYSE:M) jumped substantially in the markets. With the civilian unemployment rate down to 4.9%, circumstances are favorably set for big-box retailers.

However, several of these all-in-one shops had a rough time last year. Can the big-box titans definitively regain credibility by pulling off another earnings surprise?

While bullishness among department stores is always a positive, an earnings beat won’t be automatic for big-box stores. For one thing, revenue growth has been a problem overall for retailers. Even luxury brands — which obviously cater to a more affluent clientele — are hurting. Many are threatening to pull out of department stores, putting a black eye on otherwise solid earnings beats.

In addition, big box stores face tough challenges in e-commerce. Public enemy No.1 is Amazon.com, Inc. (NASDAQ:AMZN). AMZN has eaten away market share for both specialty goods and normal, everyday purchases. Worse yet, Amazon has significantly reduced foot traffic across multiple retailers, thereby reducing the potential for impulse sales.

However, nothing beats the convenience — and sometimes necessity — of in-store purchases. Also, economies of cost prevent e-commerce channels from being the “go-to” choice for groceries. Therefore, big-box locations are still a relevant part of the American retail landscape.

The question, then, is how relevant? Three of the largest big-box stores are about to clue us in.

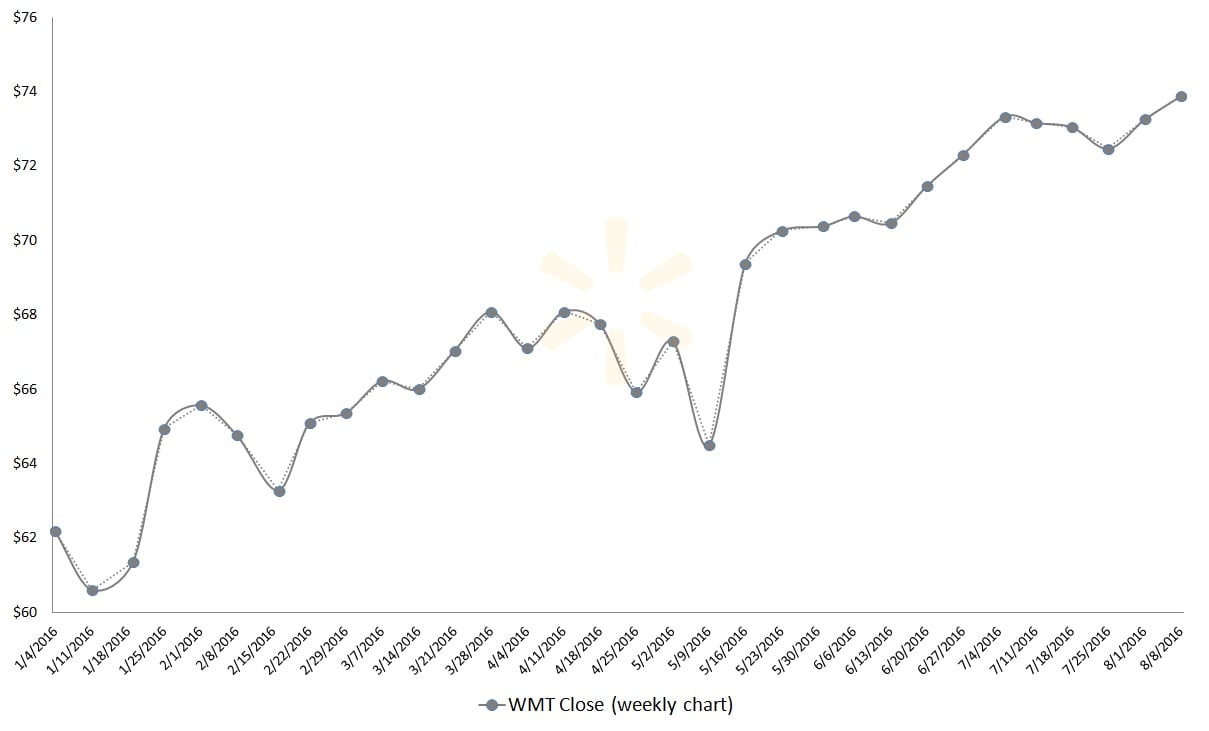

Big-Box Retailers Earnings Preview: Wal-Mart Stores, Inc. (WMT)

Click to Enlarge

It’s no secret that Amazon has been taking Wal-Mart Stores, Inc. (NYSE:WMT) to task for not being competitive in e-commerce. Last year, the big-box giant sold $13.7 billion worth of products online, comparing extremely unfavorably to Amazon’s $107 billion.

WMT hopes that its $3 billion purchase of Jet.com will change everything. In one year, Jet has already stolen some market share from Amazon through lower prices and swift logistics. That potentially plugs a major gap for WMT, which otherwise runs a dominant business.

The immediate challenge is its upcoming second quarter of fiscal year 2017. Wall Street consensus pegs earnings per share for WMT at $1.02, which is 9% below the year-ago quarter’s estimate. In recent history, WMT has been fairly shaky, missing five earnings targets in the last three years. The big-box retailer saw a slight uptick in revenue for Q1, and a modest boost in gross margin. However, generally declining profit margins are still an ongoing concern.

Based on these trends, I wouldn’t put too much hope on a massive earnings beat. However, among the featured big-box stores, WMT stock is by far the strongest performer in the markets, up 19% year-to-date. Aside from a scary dip in May, WMT has been steady as a rock throughout 2016. Unless something dramatic happens to offset that sentiment, shares could continue their upward journey.

The retail sector isn’t the prettiest, but the enormous size and reach of WMT shouldn’t be underestimated.

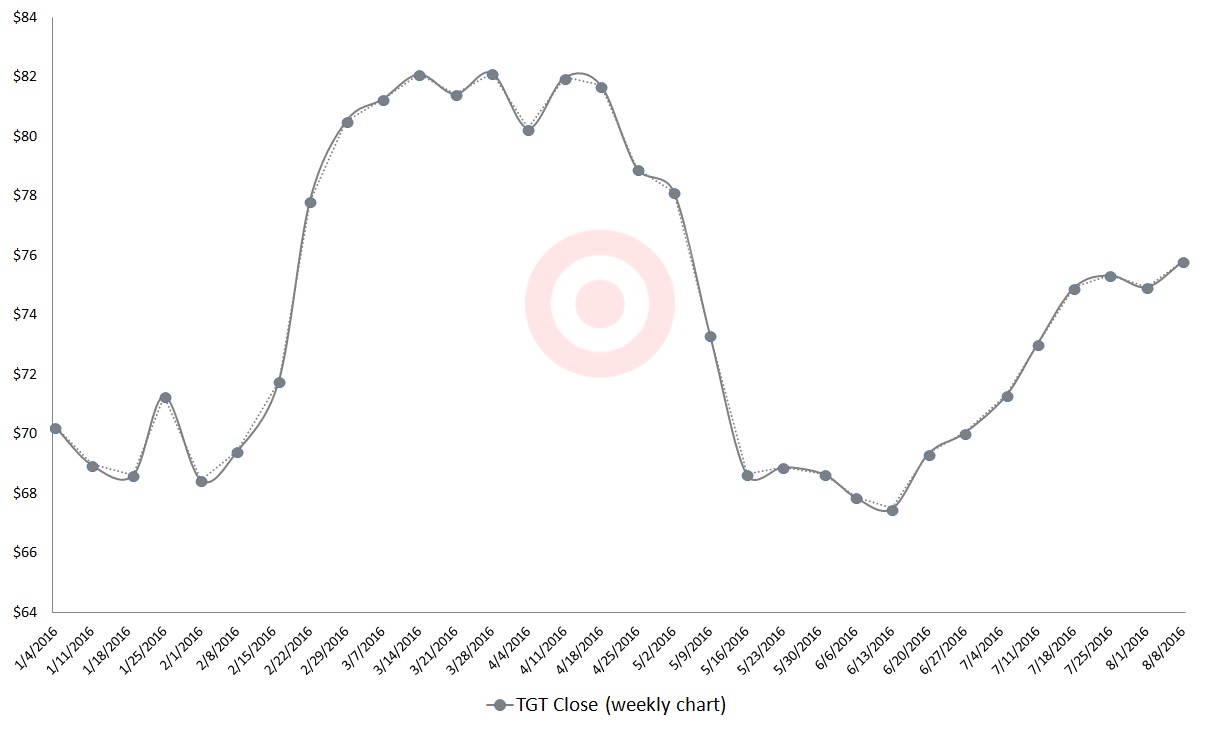

Big-Box Retailers Earnings Preview: Target Corporation (TGT)

Click to Enlarge

The biggest news item this year for Target Corporation (NYSE:TGT) is their transgender restroom policy. Immediately following the disclosure of the controversial policy, TGT stock absorbed a hammering in the markets.

The unnecessary drama — Target already had unisex-labeled restrooms in its stores — sparked heated debate. Luckily for shareholders, TGT has enjoyed a sharp rally since hitting the bottom in mid-June. Can tit overcome this ongoing distraction ahead of a critical earnings test?

Like its big-box rival, TGT earnings have been somewhat of a mixed bag in recent years. For Q2 FY2017, the consensus estimate for earnings-per-share is $1.12, a penny higher than the year-ago target. This is towards the higher end of the spectrum, which suggests the markets are optimistic for TGT. However, it won’t be a cakewalk. Gross and operating margins have generally moved southwards over the years. Also, rising inventory levels are a concern. In Q1, day’s inventory jumped 11%. That metric simply has to get better.

Overall, TGT stock is doing what it needs to do to stay afloat. Shares are up 4% YTD, well off the 7% gains of the benchmark SPDR S&P 500 ETF Trust (NYSEARCA:SPY). Currently, TGT is trading above its 50- and 200-day moving averages. So long as it doesn’t fall below technical support at $65, there shouldn’t be too much downside risk. However, upside potential could be limited due to fundamental and public relations challenges.

TGT has a solid chance of meeting expectations — just don’t expect too many fireworks.

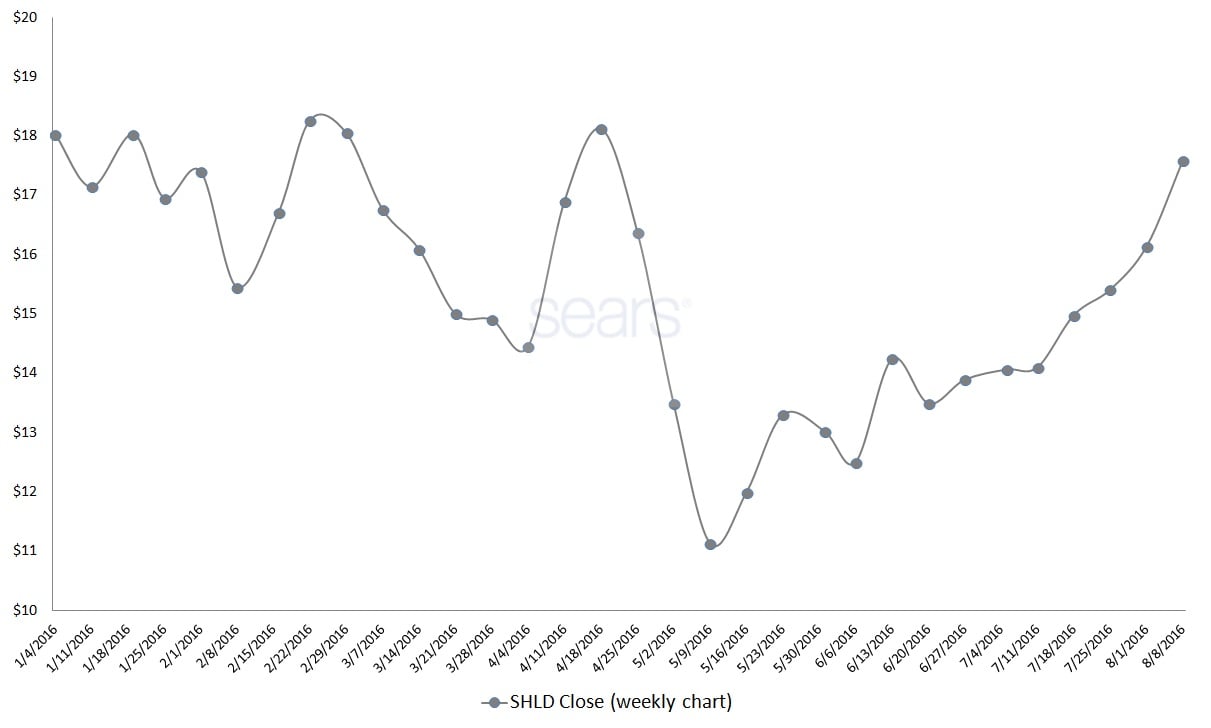

Big-Box Retailers Earnings Preview: Sears Holdings Corp (SHLD)

Click to Enlarge

Admittedly, Sears Holdings Corp (NASDAQ:SHLD) is the black sheep among big-box retailers. While its competitors have found new ways to cope under the e-commerce generation, SHLD has consistently floundered.

Shares are down 13% YTD, reflecting the outdated nature of their dominant business structure. Still, SHLD isn’t giving up without a fight, experimenting with the idea of an appliance-only store. Although it sounds inconsequential, SHLD stock is up 60% in the last three months. Can it keep momentum going?

In terms of raw numbers, it’s time for a reality check. SHLD only had one earnings beat in fiscal year 2016, getting trounced badly in the other reports. Although SHLD has a dreadfully low EPS target of a loss of $3.48 for Q2, that’s no guarantee of outperformance. Sears’ profit margins have gone from bad to worse. Its balance sheet is out of control. SHLD is bleeding cash, and it can’t turn over its aged and aging inventory quickly enough.

So what’s up with the SHLD buying spree? It all comes down to pure speculation. At a share price south of $18, SHLD is dirt-cheap. For example, the difference between Wal-Mart’s enterprise value and market capitalization is 20%. For Target, it’s slightly “better” at 23%. But for SHLD, the difference is 185%. By no means is this a sound justification for a long-term investment. However, Sears may have hit rock bottom, which makes it a compelling gamble.

It may be the worst of the big-box stores, but sometimes, bad news is good news.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.