If it wasn’t obvious before, it should be now. In the retail sector, you are either online or you are out of line. Although exceptions exist — Best Buy Co Inc (NYSE:BBY) is a prime example — the brick-and-mortar format is excruciatingly frustrating. In particular, Macy’s Inc (NYSE:M) is finding out that consumers are no longer willing to pay brand premiums.

Year-to-date, Macy’s stock is down 17%. Rival Nordstrom, Inc. (NYSE:JWN) is comparatively superior at 3% YTD.

Year-to-date, Macy’s stock is down 17%. Rival Nordstrom, Inc. (NYSE:JWN) is comparatively superior at 3% YTD.

However, JWN’s technical picture has been awfully volatile over the past two years. Any victory in the markets is likely short-lived. Luxury department store Dillard’s, Inc. (NYSE:DDS) is also experiencing similar woes, with shares down 7.4% YTD.

Here’s the scary thought about the luxury discretionary sector — consumption is up, way up. According to the U.S. Bureau of Economic Analysis, personal expenditures in the first quarter of 2017 jumped 4.8% from the year-ago quarter. In fact, this is the biggest jump we’ve seen in first-quarter consumption this decade.

These expenditure figures are a credibility boost for President Trump, but they’re worrisome for Macy’s and M stock investors. The American people are clearly opening their wallets again. The real issue is where they’re spending their money. If we look at the charts, it’s not at the iconic retailer.

To their credit, management has been working hard to return value to Macy’s stock. The company is shedding dead weight through store closures

, and they’re continuously improving their e-commerce channels. Will these efforts pay off for their upcoming earnings report?

Managing Expectations for Macy’s Stock Earnings

For the first quarter of their fiscal year 2018, M stock is expected to hit an earnings-per-share target of 34 cents. Given the bearish circumstances of the retail market, this is on the optimistic range. At the top end, analysts forecasted a 40 cent EPS target, while the bottom is pegged at 25 cents.

In the prior year Q1, M stock registered an EPS of 40 cents, beating the consensus estimate of 36 cents. However, any beat will be difficult to achieve this time around, especially one with a near-12% positive surprise. Particularly concerning is the declining trend of their holiday earnings. Although Macy’s beat Q4 estimates last year, its results were lower than FY2016 and FY2015 figures.

That compounds the problem created by e-commerce competitors — namely, reduction in foot traffic. And if consumers can’t be bothered with shopping at Macy’s during the holidays, where will M stock make it up?

The revenue side of the equation doesn’t help the overall picture. For Q1, analyst estimates range from $5.4 billion to $5.7 billion, with consensus landing at $5.5 billion. Based on prior sales results, Macy’s stock could very well hit the consensus. However, that’s all that the famed retailer has been doing. At some point, investors will want to see some productivity.

M Stock Might Be on the Road to Recovery

On a technical scale, I wouldn’t expect too many fireworks to erupt from the M stock earnings report. Over the last four Q1 reports, Macy’s shares averaged a loss of 1%, as a next-day response to the results. Therefore, the historical trend suggests a negative reaction, but a small one. This makes sense, considering that the “big one” is the retailer’s Q4 report.

Moving forward, the general sentiment towards Macy’s stock is obviously not pleasant. However, the bullish argument asserts that much of the bad news is already baked in. With a leaner, meaner Macy’s, it’s more difficult for Amazon.com, Inc. (NASDAQ:AMZN) to render appreciable damage.

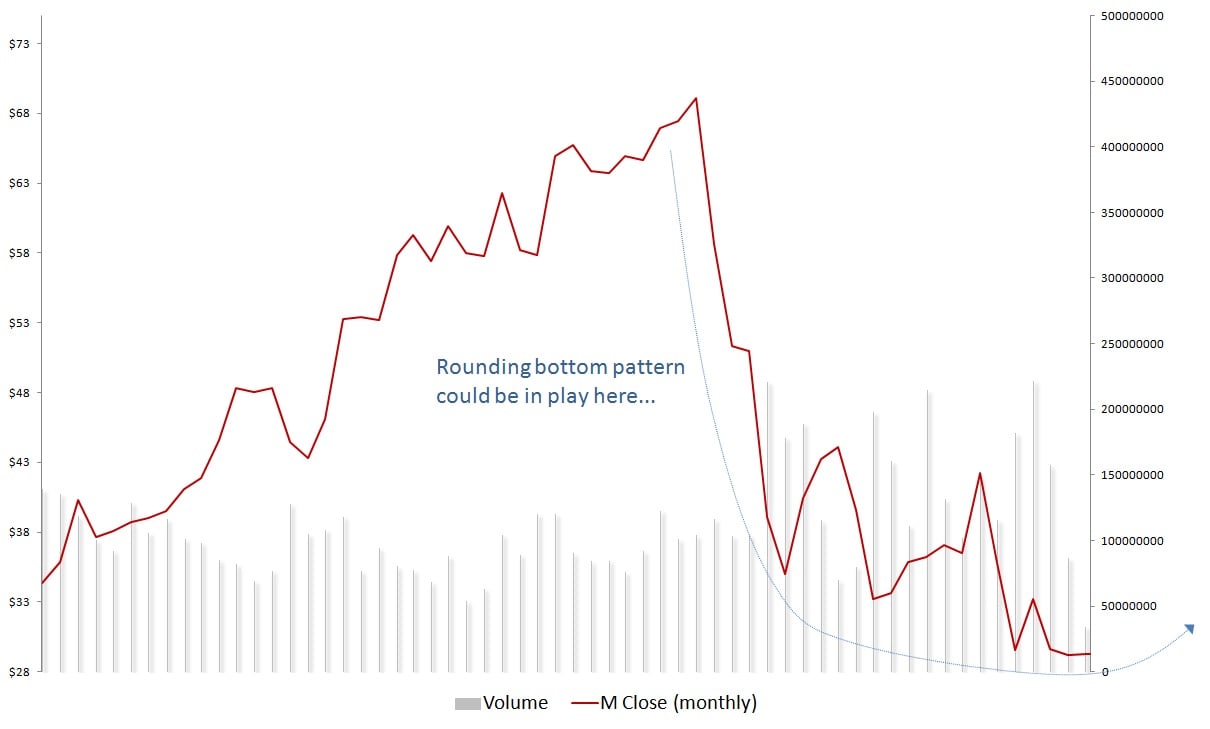

Click to Enlarge

Looking at Macy’s stock from a wider scale, I agree. M shares might be in the middle of forming a rounding bottom pattern. The volatility’s intensity has definitely subsided since the tumbling that began in July 2015. Subsequent selloffs were intense, but nowhere near what we saw almost two years ago.

This analysis doesn’t guarantee the stoppage of further pain. However, as a contrarian play, I think M stock offers a reasonable risk-to-reward balance. Wall Street is acclimated to the retail ugliness. If Macy’s management can further impress the markets through a solid recovery strategy, M shares could be a strong opportunity.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.