Recently reported by Bloomberg Business, hedge fund managers have made significant coin on the crude oil markets since mid-summer of this year.

Unfortunately for struggling oil stocks, much of Wall Street profits were accrued from shorting the “black gold” industry. Worse yet, the bearish sentiment shows no sign of abating.

Unfortunately for struggling oil stocks, much of Wall Street profits were accrued from shorting the “black gold” industry. Worse yet, the bearish sentiment shows no sign of abating.

Short traders catapulted their activity in West Texas Intermediate by 18% in mid-October, the highest percentage jump since July, according to the Commodity Futures Trading Commission.

The ugliness in the energy markets comes down to pure fundamentals. Crude inventory in the U.S. has skyrocketed by 22.6 million barrels over the past month, hitting a multi-decade record despite several oil firms cutting production by more than half.

The excess supply is augured to pressure crude indices (and in turn, oil stocks of varying market capitalization) through 2016 should the International Energy Agency prove prescient.

Still, crude production and drilling companies are attempting to make the most of the deeply unfavorable markets. The SPDR S&P Oil & Gas ETF (XOP) pared some of its 27% year-to-date loss with a 6% lift for the month of October. Many individual oil stocks have found similar surges in performance as contrarian investors push back against the heavy headwind.

The nagging question, however, is will it be enough to save a pummeled industry? For three of the major oil companies set to release their earnings results later this week, uncertainty hangs in the air.

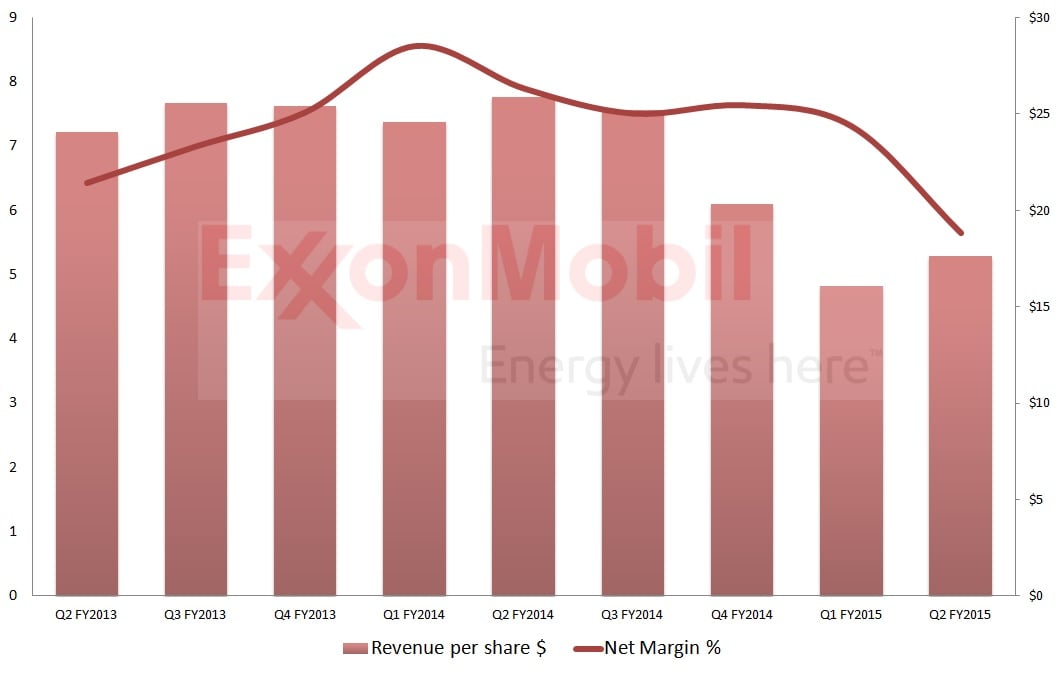

Crude Oil Stocks to Sell: Exxon Mobil (XOM)

Click to Enlarge

While much of the media’s attention has been focused on the trials of oil stocks, futures contracts for natural gas have tumbled to multiyear lows due to excess inventory and unusually warm weather patterns that have delayed demand for winter fuels.

The result has been equally deadly for natural gas producers as it has been for oil stocks. Magnum Hunter Resources Corp. (MHR) investors saw their portfolio decline by nearly 12% on Oct. 26, while Chesapeake Energy (CHK) — the biggest natural gas producer in the U.S. behind only Exxon Mobil — saw similar bearishness on the same day, closing down 9%. While not escaping entirely unscathed, XOM stock investors were hardly flustered, losing a relatively small 2%.

The tricky part about XOM stock is whether it can meet Wall Street’s downgraded expectations in a veritable bear market. The consensus estimate for XOM stock’s earnings per share is 89 cents for the third quarter of fiscal year 2015, which sheds a full dollar from Q3 FY2014.

However, net margins this year are down an average of 18% against last year’s results, making it a greater challenge to hit the EPS target when Exxon’s report is released on Oct. 30.

And although XOM stock surged forward nearly 9% this month, long-time shareholders are still behind the ball by 12% YTD. In the past week-and-a-half, XOM stock has pushed against its 200-day moving average, but has yet to convincingly move past this resistance barrier. The longer this pensiveness holds out, the higher the probability that the bears will gain leverage.

XOM stock will certainly not get dethroned in the foreseeable future, yet it still faces the volatility — albeit to a lesser extent — that has struck its weaker brethren in the throat.

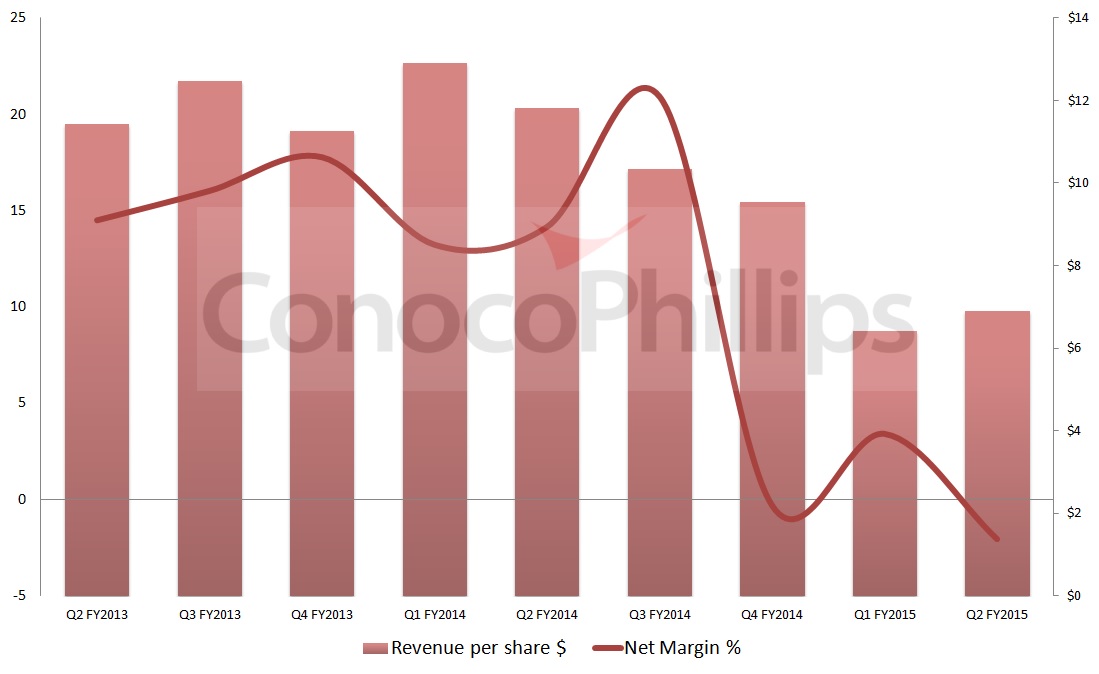

Crude Oil Stocks to Sell: ConocoPhillips (COP)

Click to Enlarge

Emblematic of the recent malaise striking oil stocks, ConocoPhillips made two high profile headlines in which the company announced its sale of its equity stake in a Norwegian gas-pipeline network, as well its intention to unload a 40% ownership in an Indonesian oil and gas field.

Analysts have not been too keen on ConocoPhillips’ desperate bid to stay solvent, where COP stock’s consensus EPS target for Q3 FY2015 is in the red by 37 cents. This sharply contrasts with the Q3 EPS estimate for last year, which came in at $1.20 and was effectively beaten with an 8% earnings surprise. This year, however, net margins are down to 0.7%, a far cry from the 10.5% average between FY2010 and FY2014. Exacerbating matters is COP stock’s revenue trend, which has declined sharply — combined sales in the first two quarters of this year were only 4% above Q1 FY2014 sales.

Further questions are asked of COP stock’s technical posture. While shares are up 8.5% in October, it’s difficult to overlook the fact that ConocoPhillips shares have lost more than 24% YTD. Unlike its bigger brother Exxon Mobil, COP stock has yet to touch its 200-DMA and is sandwiched between that and the 50-DMA below. Additionally, COP stock has failed to attack a descending resistance line that has been in place since the summer of last year.

Until there is a more compelling reason to invest in ConocoPhillips, the likelihood of an imminent recovery in COP stock is very much muted.

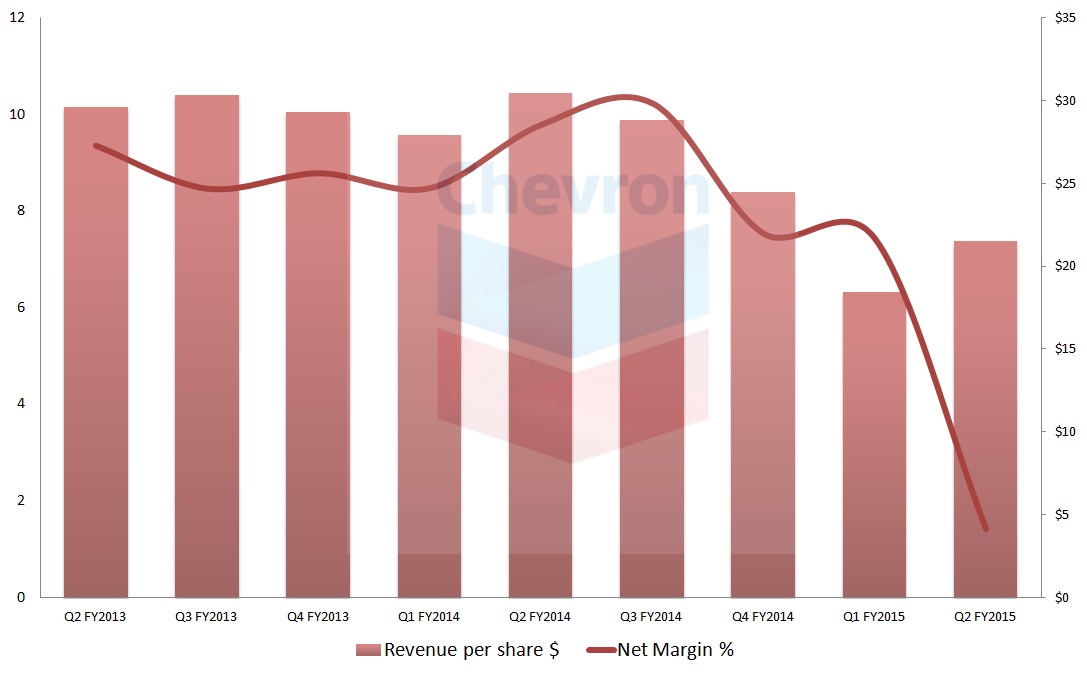

Crude Oil Stocks to Sell: Chevron (CVX)

Click to Enlarge

As Bloomberg Business reports, Chevron is the most vulnerable oil firm to price fluctuations in the benchmark Brent Crude Oil index, with each dollar change impacting CVX stock’s cash flow by around $330 million.

Of course, this is hardly problematic when crude oil is in a bull market. When crude indices are down 40% or more over the past year, however, things can get ugly quickly.

With CVX stock having gained only about 5% in the past five years — essentially averaging 1% returns a year — investors will find little solace in the 12% run up for this month. Unless CVX stock can break into triple-digit territory like it has for much of this decade, odds are against a continuation of recent momentum.

With its Q3 FY2015 earnings set for a Friday release date, there is very little to suggest that CVX stock will beat its consensus EPS target of 76 cents. Not only is this well below that of the $2.95 target from a year-over-year basis, net margins fell off a cliff for Q2 of this year, following a descending trend since Q3 FY2014.

CVX stock’s EPS trend is slightly worse, which has been steadily shedding points since Q2 of last year. All of this points to the unfortunate conclusion that further cuts may be necessary to keep shareholders happy.

It’s a tough set of cards dealt to CVX stock, one which management will find extremely difficult to play without getting severely burnt.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.