After coming off a decidedly bullish report in which the value of China’s exported products in March exceeded expectations, April stunted any pretense of optimism. Describing the disappointing results as “grim,” a Reuters article cited a near 2% drop in Chinese exports year-over-year.

In contrast, March results showed an 11.5% increase in export value, handily beating consensus estimates of 2.5%. But isn’t just a one-time deal, the latest data portends a potentially long-term bearish shift in Chinese markets.

In contrast, March results showed an 11.5% increase in export value, handily beating consensus estimates of 2.5%. But isn’t just a one-time deal, the latest data portends a potentially long-term bearish shift in Chinese markets.

First, there is the desperation by mainstream policymakers to paint a pretty picture on an ugly canvas. The International Monetary Fund sang China’s praises, stating that the Asian giant was a rare glimmer of hope in an otherwise bleak global economy. In fact, the IMF warned that international markets faced a “synchronised slowdown” unless they got their act together. Now, it seems that China will add its name to the long list of economic laggards.

Aside from the slide in exports, April imports dropped sharply by almost 11%, against a forecast of a 5% decrease. That marks 18 consecutive months in which imports fell. It also is an indictment on Chinese consumer sentiment, which was hoped to carry some of the burden of a slowing economy.

Worse yet, China has been rapidly expanding its credit market, but it has yet to show desired results. Although the country has shown success in circulating loans throughout its financial system, there’s no guarantee the money ends up in productive places.

This flaw is rearing its ugly head at an inopportune time. In the first four months of 2015, Chinese exports totaled $690 billion. In 2016, that figure dropped to $637 billion — a near 8% decline. With China having dropped to single-digit growth in terms of gross domestic product, it’s going to take a herculean effort to get things back on the right track.

Unfortunately, there are not too many places in the global economy where the lost ground can be made up. Here are three stocks that will likely be the most negatively impacted.

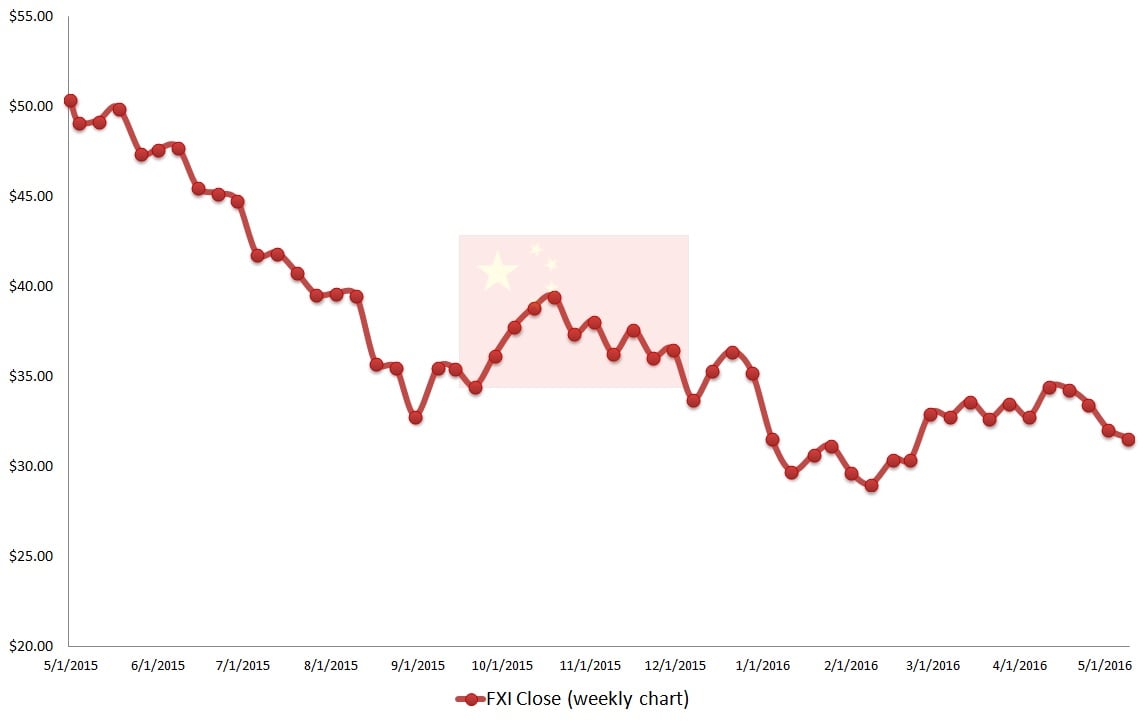

Chinese Stocks to Sell: iShares China Large-Cap ETF (FXI)

Click to Enlarge

With average trading volume in excess of 24 million, the benchmark exchange-traded fund iShares China Large-Cap ETF (FXI) is sure to feel any reverberations from the Chinese markets.

The FXI absorbed a near 2% hit after the exports data was released, adding more pain to an already dour season. Year-to-date, FXI is in the red by 9%. This is well below western benchmarks like the SPDR S&P 500 ETF Trust (SPY) and iShares MSCI Germany Index Fund (ETF) (EWG). FXI is also more than twice as bad as the iShares MSCI Japan ETF (EWJ

) — that alone tells quite a bit about China’s woes.

Another factor to consider is FXI’s sector holdings. Although it covers a broad range of industries, the overwhelming majority is weighted towards financial services. Despite numerous efforts by The People’s Bank of China to gin up the economy, the banks have certainly not been a major beneficiary — otherwise, the market value of FXI likely wouldn’t be as deflated as it is.

On a technical note, FXI is down some 38% from last year’s peak price. Disturbingly, the Chinese market fund is persistently falling inside a step-down pattern. This is characterized by sharp corrections after previous recovery rallies have failed. In this case, the contrarian trade may be a risky one since the fundamentals are quite bearish.

Until broad stability is introduced into the Chinese economy, FXI may suffer volatility due to its heavy exposure to the financial sector.

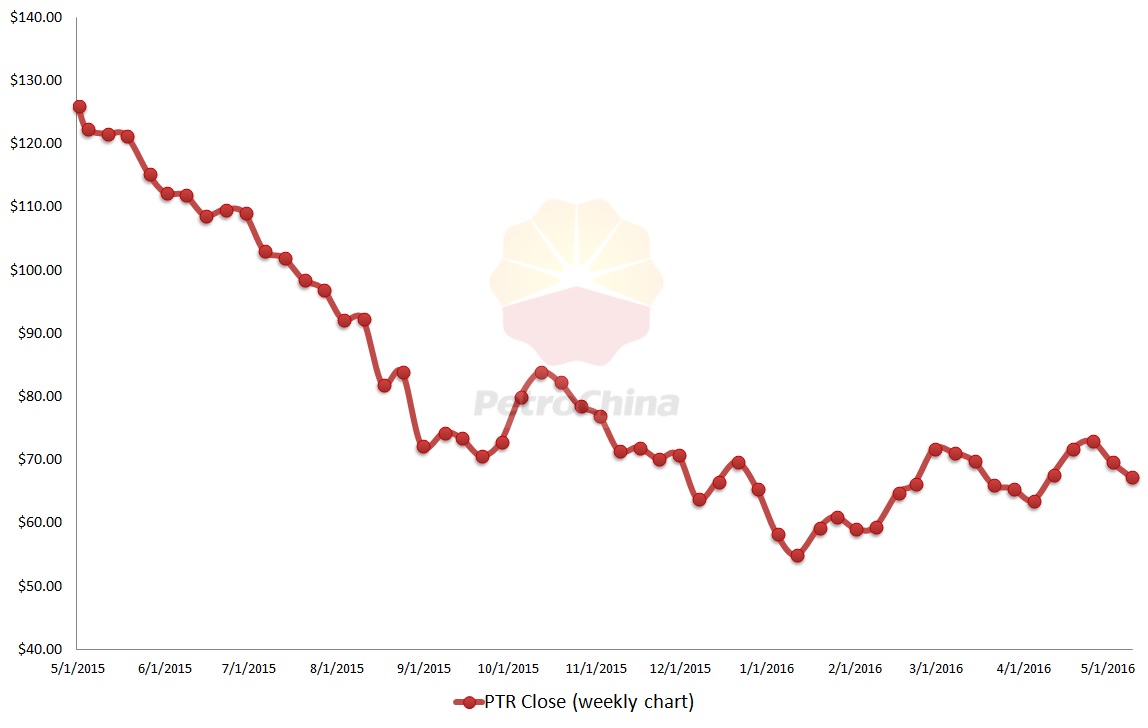

Chinese Stocks to Sell: PetroChina Company Limited (ADR) (PTR)

Click to Enlarge

The long-term rout in the oil markets combined with pensive attempts at a recovery spells double trouble for PetroChina Company Limited (ADR) (PTR).

On one hand, the sudden deflation in energy markets sent virtually all oil producers tumbling as once lofty profit margins were immediately slashed. However, China is especially desperate to gain positive traction and has pumped money into PTR and regional producers. The results, though, have been less than satisfying.

PTR reported its “first-ever” earnings loss when it released its results for the first quarter of fiscal year 2016. Net income dipped $2.1 billion, in stark contrast to the $943 million PTR brought in from the year-ago quarter. On an earnings per share basis, PTR slid to -$1.23. The primary contributor to the malaise was an $11.5 billion gap in Q1 revenue compared to last year.

Despite relatively strong margins in recent years, the sudden drop in sales was too much to overcome.

Moving forward, the situation is even murkier. Domestic demand for oil is down. Other key markets are trimming their expenses. Even without these challenges, PTR faces an uphill climb with a global energy supply glut that will pressure margins in the foreseeable future. If technical performance is anything to go by, PTR stock has been almost exclusively negative since its Q1 earnings release.

As things currently stand, PTR faces a number of harsh headwinds that make it a less than desirable investment.

Chinese Stocks to Sell: Industrial & Coml Bank of China Ltd(ADR) (IDCBY)

Click to Enlarge

The summer of last year was a particularly rough period for Industrial & Coml Bank of China Ltd(ADR) (IDCBY).

In July of 2015, IDCBY was usurped by Wells Fargo & Co (WFC) as the world’s biggest bank by market capitalization. If that wasn’t enough, IDCBY went on to lose nearly 30% of equity value. In contrast, Wells Fargo lost a much more palatable 14% over the same time period.

The biggest concern for investors is that IDCBY doesn’t appear to have found bottom yet.

Similar to FXI, IDCBY is locked into a step-down pattern. Not only has the Bank of China failed to engineer a sustained rally, the bottom of each correction is acting like resistance for future price action. IDCBY is still down more than 15% YTD, despite seeing a 16% swing up between mid-February and mid-April.

On the fundamental side, there’s a feeling among potential buyers that IDCBY is “tapped out.” Revenue for FY 2015 was $108 billion, or less than 2% growth from the prior year. This is the worst year-over-year growth rate for IDCBY since 2009.

Additionally, it’s well off the average 20% revenue gain over the past decade. This largely explains why IDCBY stock is so cheap relative to both trailing and forward earnings — there’s simply no confidence in the bank’s potential.

Overall, the financial sector is a hot mess, but the troubles in China are only exacerbating the bearishness in companies like IDCBY.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.