The skies just aren’t that friendly anymore to airline stocks. Near the start of the decade, the airline industry was one of the S&P 500‘s top sectors. Between 2012 and the end of 2014, the Dow Jones U.S. Airlines Index skyrocketed over 250%. The most obvious cause was the grinding recovery from the 2008 financial crisis.

But since the beginning of last year, airline stocks — in particular, discount airlines — have hit significant turbulence. For speculative traders, airline stocks have provided plenty of excitement.

The problem with the gains in airline stocks is that they’re unsustainable. Even more telling, the technical chart of the airliner index shows a net bearish decline over the past two years. The softness in airline stocks, particularly those from low-price leaders, may perplex some. After all, we’re witnessing record low levels in energy markets. That should allow discount airlines to aggressively promote their services.

There’s no doubt that while key economic metrics like the labor market have recovered on paper, Americans are still feeling the pinch. That translates into a reduced consumer base, even if fuel costs are low. Ultimately, no one among airline stocks is immune — everyone is out for themselves in a dog-eat-dog world.

The cannibalization that’s occurring isn’t doing any favors for the industry. However, the low price leaders are most at risk due to their commoditized business strategy. Here are three discount airlines to avoid:

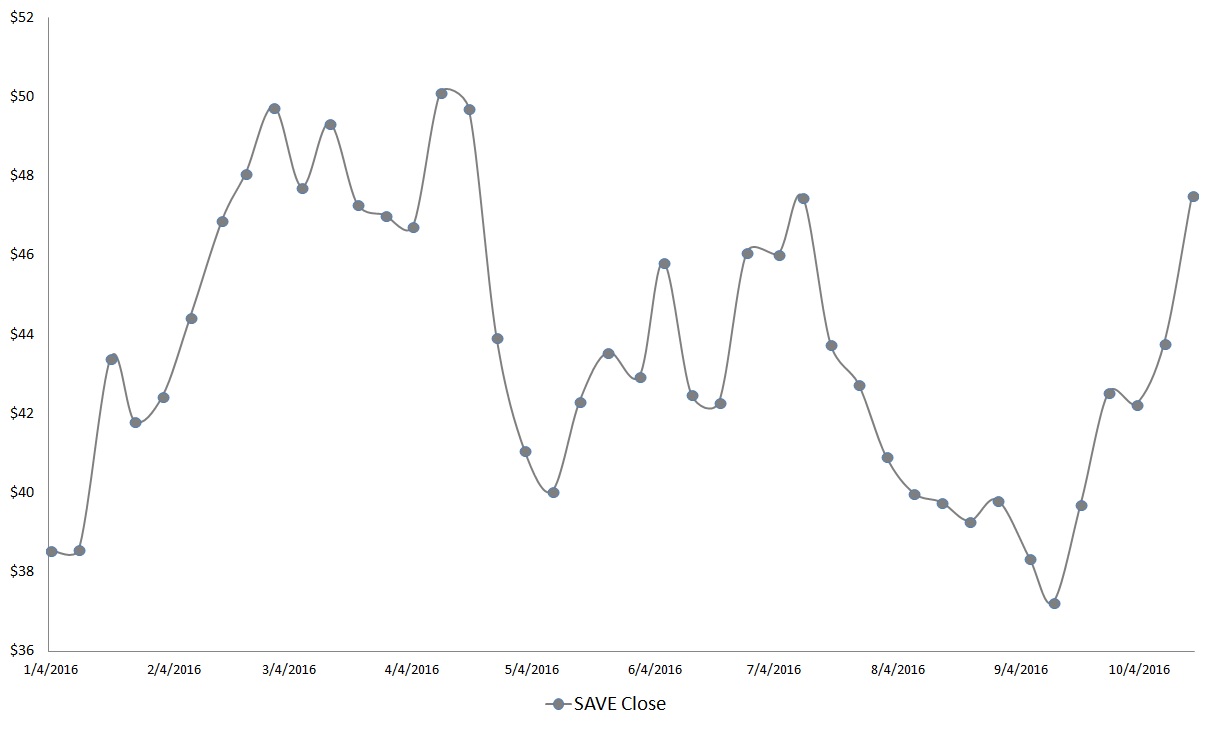

Discount Airlines to Avoid: Spirit Airlines (SAVE)

Click to Enlarge

In a little more than a month, SAVE will offer flight routes into Cuba, a first for American companies in over 50 years. But with lucrative business comes intense competition. Whether SAVE can withstand the pressure is a bit of a question mark.

On one hand, Spirit has consistently met or exceeded earnings expectations over the past three-and-a-half years. Sure enough, SAVE pulled off another earnings beat this past Tuesday. The Street pegged per-share earnings at $1.17, which is 15 cents lower than the year-ago level’s consensus. Spirit surprised with EPS of $1.24. In addition, SAVE has industry-beating profitability margins and revenue growth.

But on the flip side, strong fiscal performances have not translated into market gains. Sure, SAVE is up more than 20% year-to-date. At the same time, it’s been a rough and tumble ride. If you bought shares this past spring, there’s a good chance that you’re either underwater or just barely breaking even. And against the highs of last year, SAVE stock is currently down 42%.

Even though the financials look good now, the company is headed for an increasingly competitive environment. It’s probably best to SAVE this for another time.

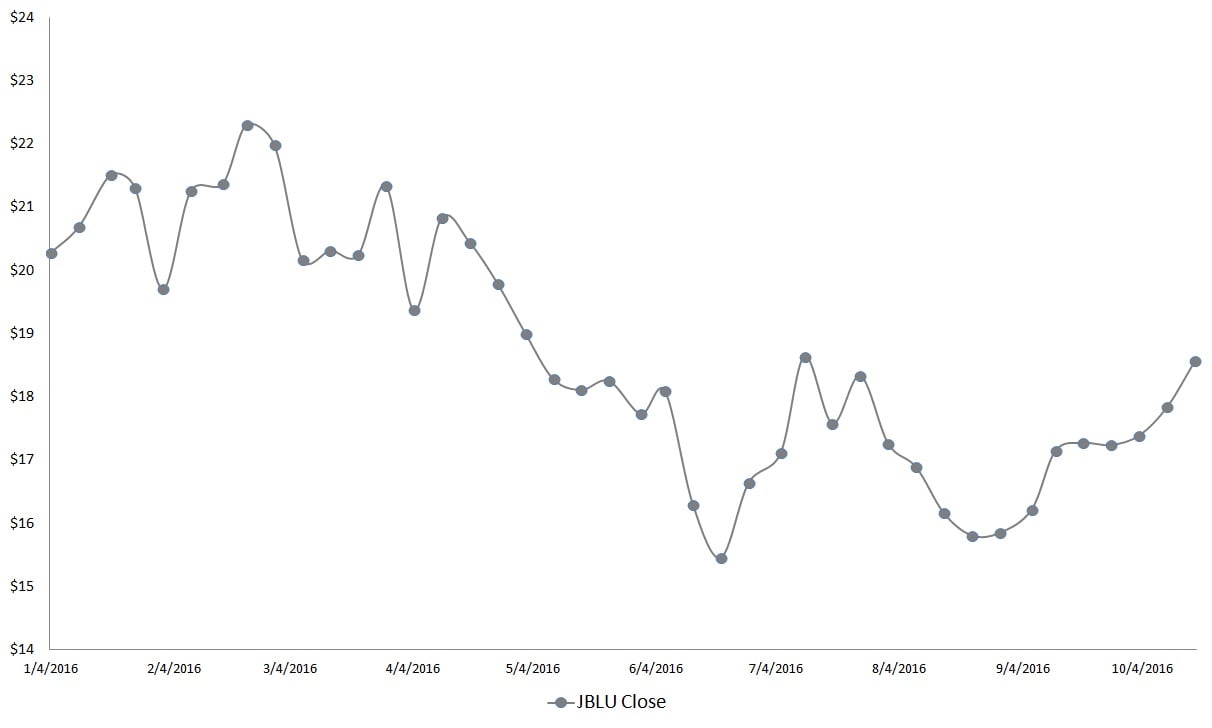

Discount Airlines to Avoid: JetBlue (JBLU)

Click to Enlarge

That discipline has clearly carried over into the income statement, which features outstanding operating margins, and significantly better-than-average net margins. JBLU is also trading at eight times trailing earnings, which would be considered one of the bargains among discount airlines.

So why won’t people buy JBLU stock? Like any investment, the point is to consider where the asset will be, not where it is. Right now, airline stocks look challenged, and the problems down the road don’t appear to be any easier. That’s best reflected by the revenue trend for JBLU. From 2007 through 2011 annual sales growth averaged 14% despite a 3% loss in 2009 for obvious reasons. In the last four years, however, JBLU has mustered only 9% growth — a significant decline.

Over the past year-and-a-half, JBLU has turned in fairly consistent — and positive — earnings results. It’s hard to see Wall Street getting too excited about desperate competition and market saturation, though.

JBLU will definitely benefit from tailwinds like Cuba, but so will other airline stocks. That’s probably the biggest reason why JBLU has floundered this year, down 18% in the markets.

JetBlue is a bargain, but only because of its price tag. With steep obstacles ahead, it’s one to skip.

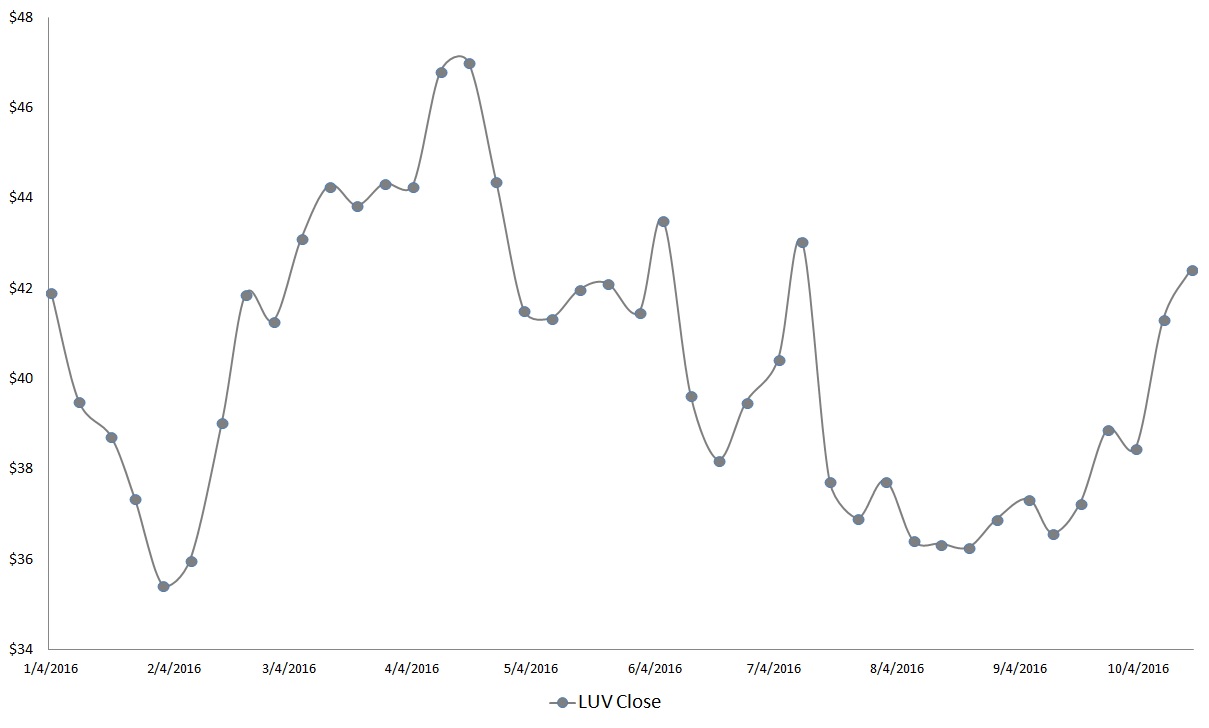

Discount Airlines to Avoid: Southwest Airlines (LUV)

Click to Enlarge

Thanks to quirky and memorable commercials, LUV was able to rake in the dough. On paper, the company is just another name among discount airlines. But there’s no denying that LUV has a public appeal that’s missing from its competitors.

Popularity is only going to take you so far, though. Like other airline stocks, LUV has had a bear of a time duplicating prior successes. From 2007 through 2011, sales growth averaged a healthy 12%. But from 2012 onwards, LUV slid to a shocking 6%. I don’t think it’s a coincidence that since the beginning of last year, shares have rocked back and forth in a broad, sideways trend channel. Investors are still trying to feel out the discount airlines industry.

At this point, the only rational approach is to be cautious. LUV stock should be able to beat its third-quarter earnings target, which stands at 88 cents. This is four cents below the prior year’s consensus forecast. Outside of a rare miss in Q2 of this year, LUV has turned in consistently strong reports. However, none of that has brought shares above the nagging $50 resistance level.

Unfortunately, there’s no LUV for airline stocks in general, and that could be the downfall of Southwest.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.