I’m a big fan of Israeli stocks. First and foremost, Israelis are essentially the world’s most educated people. You can’t progress as a society unless rationality and science reigns, and they have it in droves. I also love the fact that Israeli companies do things differently. While westernized markets relish growth through debt, the Jewish culture eschews such mechanisms. I can go on and on about Israel. Sadly, though, Teva Pharmaceutical Industries Ltd (ADR) (NYSE:TEVA) is testing my loyalty.

Oy vey! You don’t have to look far to see what a disaster TEVA stock has become.

Retrospectively, Teva Pharmaceutical just never found its footing throughout all of 2016. I, along with other bulls, were hoping that the company could leverage its enormous assets. Instead, it just kept gently moving lower until late September — that’s when the big drop happened. From there, TEVA stock just couldn’t lock things up.

That’s not surprising given that Teva Pharmaceutical is hemorrhaging bad news. As InvestorPlace Contributor Chris Lau neatly summarizes, the “CEO is leaving, Copaxone’s patents were invalidated by the U.S. courts, and generic drug manufacturers are out of favor. These and other headlines have driven TEVA down by about 45% over the past year.”

But just like the ancient Chinese never said, in every crisis, there is an opportunity. Should investors give the stock another twirl?

The Cautious Bull Case for TEVA Stock

Lau is an optimist, and for good reason. For starters, the market price for TEVA stock is at levels not seen since late 2013. As a result of the massive fallout, the forward-price-earnings ratio for Teva Pharmaceutical is less than eight. That’s absurdly below the pharma industry’s median forward P/E ratio of 14.7.

This isn’t a case of buying a cheap company at a cheaper price. That much is obvious when you look at TEVA stock’s dividend yield of nearly 4%. It’s starting to approach AT&T, Inc. (NYSE:T) territory, with the exception that there’s much more potential with TEVA. Of course, I’m not sure if that’s going to hold up given the bearish circumstances. Still, at the present rate, it’s a lot more generous than the average global drug manufacturer, which yields only 1.6%.

Let’s also consider that when Teva Pharmaceutical CEO Erez Vigodman stepped down, it wasn’t exactly a Captain Schettino moment. Although the optics looked terrible — leaving right before the company’s fourth-quarter earnings report — the results were good. TEVA stock beat on the bottom line, and revenue got a nice boost from its acquisition of Actavis Generics. Formerly a unit of Allergan plc Ordinary Shares

(NYSE:AGN), the Actavis deal was completed on Aug. 2 of last year.

Also, what was said during the earnings conference call was particularly reassuring. Despite TEVA’s unfavorable ruling regarding its Copaxone drug — a treatment for multiple sclerosis — by the U.S. legal system, the company didn’t downgrade its 2017 outlook. Furthermore, it’s going to take some time before rivals like Mylan N.V. (NASDAQ:MYL) and Pfizer Inc. (NYSE:PFE) can offer generic alternatives.

Teva Pharmaceutical Is the Comeback King

Normally, when a corporation loses nearly half its market value in a one-year time period, investors run away. It’s no surprise that analyst the consensus shifted significantly in recent months, accentuated by TEVA stock downgrades from major firms. But at the same time, I find it curious that The Wall Street Journal is seemingly pushing for a Teva Pharmaceutical rebound. They’re supposed to report the news, not become it.

Click to Enlarge

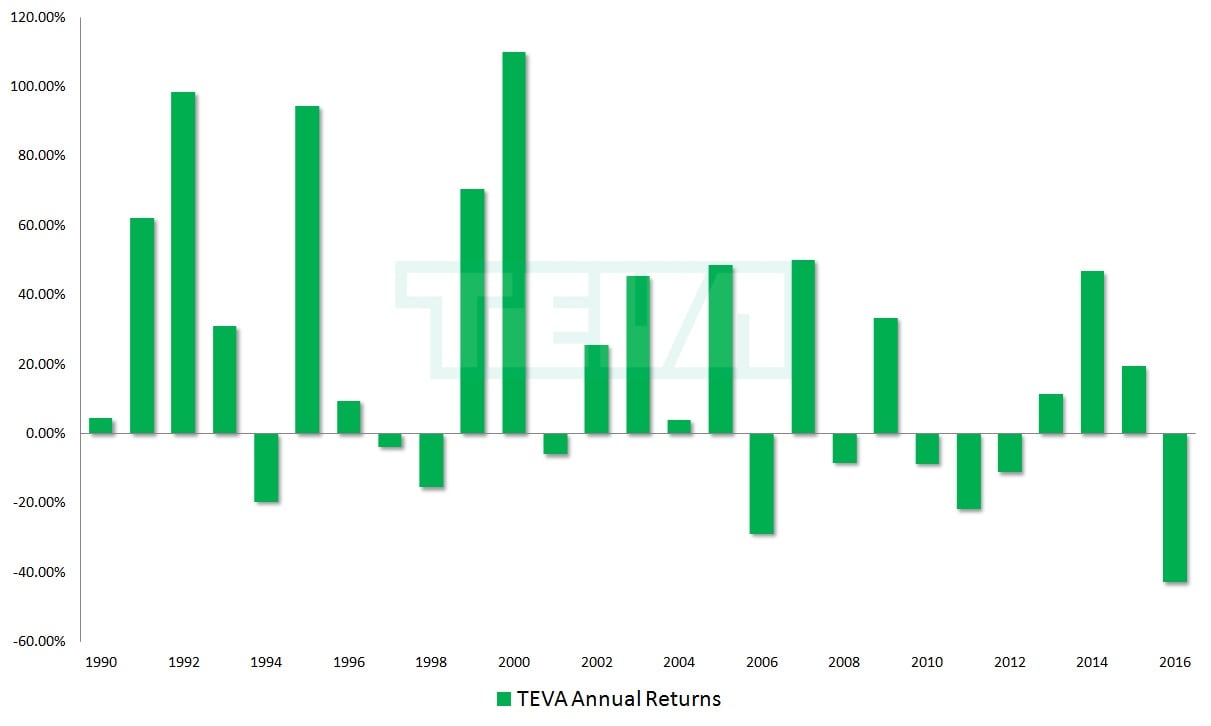

So I don’t consider myself crazy in joining the contrarian “bandwagon.” Plus, I have the technicals to back me up. Generally speaking, TEVA stock is an investment that knows a thing or two about comebacks.

Including 2016 data, the average annual loss for TEVA is just under 17%. Yet its overall lifetime average return is more than 22%.

TEVA stock also has a tendency of rebounding strongly off a bum year. Of the times when shares incurred double-digit losses, the average follow-through is a very sweet 43%. Now, it’s true that last year was the worst annual performance registered by Teva Pharmaceutical. So where does that leave us?

It’s a classic case of the glass half-empty or half-full. In my opinion, I’d be inclined to show a little chutzpah for TEVA stock. This goes against standard investing principle. However, you have to look at the broader context. TEVA is still the world’s biggest manufacturer of generic drugs. It’s innovating like crazy, and most importantly, it can take a beating and come back twice as strong.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.