Diversification is the lifeblood of any investment strategy. Since no one can predict the markets with absolute certainty, diversification allows us to hedge against the unexpected. It’s a wise course of action for almost any circumstance. But too much diversification can also be a problem. By hedging against everything, you deny yourself a chance to move forward. This is the unique problem afflicting General Electric Company (NYSE:GE).

For as long as I was assigned to write about GE stock, I’ve maintained a generally bullish perspective. General Electric is an industry stalwart, a company whose roots are older than my grandparents.

Over the centuries, the firm picked up numerous assets and businesses. And despite its rickety old ways, GE demonstrated a willingness to integrate current trends and phenomena. All in all, the American icon conveyed dependability in confusing times.

Unfortunately, GE stock has been dependably disappointing. Rather than using its vast resources as assets, management somehow found a way to make them de facto liabilities. General Electric committed several direct errors while incurring opportunity costs. At the same time, those that kept believing that the energy/manufacturing/utility/aviation/technology/healthcare/whatever company would come through with a jab from anywhere were badly let down.

The final nail in the coffin was the competition. Somehow, Honeywell International Inc. (NYSE:HON) and Koninklijke Philips NV (ADR) (NYSE:PHG) managed to keep things on the up and up. Both are looking at double-digit returns on a year-to-date basis. In a perfectly inversed contrast, GE stock is down 19% year-to-date.

I had to

switch allegiances, and so I did.

Solid Earnings Can’t Mask Problems for GE Atock

On the day that my last General Electric write-up was published (July 6), shares dropped nearly 4%. Over the next few days, GE stock enjoyed the benefits of a dead-cat bounce. But soon enough, the charade was over. The company’s own second-quarter earnings report called BS.

As InvestorPlace market strategist Anthony Mirhaydari noted, the actual figures were solid. GE managed to beat both its consensus earnings per share target and its forecasted revenue. Renewable energy and power divisions were the standout performers, demonstrating strong growth. General Electric also produced a great report in Q1, proving that it’s building off its momentum.

But Wall Street was having none of it. On a year-over-year basis, the industry stalwart incurred a 12% decline in sales. So while management confirmed that some of its businesses are winners, others are losers. Even worse, as an aggregate, General Electric could not come close to the numbers they pulled last year. As a result, the markets brutalized GE stock’s post-earnings report.

The silver lining is that Q2 was the last report for the soon-retiring CEO Jeff Immelt. Current President and CEO of GE Healthcare, John Flannery, will take over next month.

Even the much-needed transition of power may not be enough. Jack DeGan, chief investment officer at Harbor Advisory, stated the following: “Usually when a new CEO comes in, especially after a long-standing previous CEO, they want to lower the bar because that’s where their starting point begins.”

I sincerely hope that this will not be the case because it’s such a Millennial thing to do. GE desperately needs strong leadership, clear vision and the capacity to deliver. Anything short of 100% is simply not acceptable.

As It Stands, GE Can’t Walk the Walk

Click to Enlarge

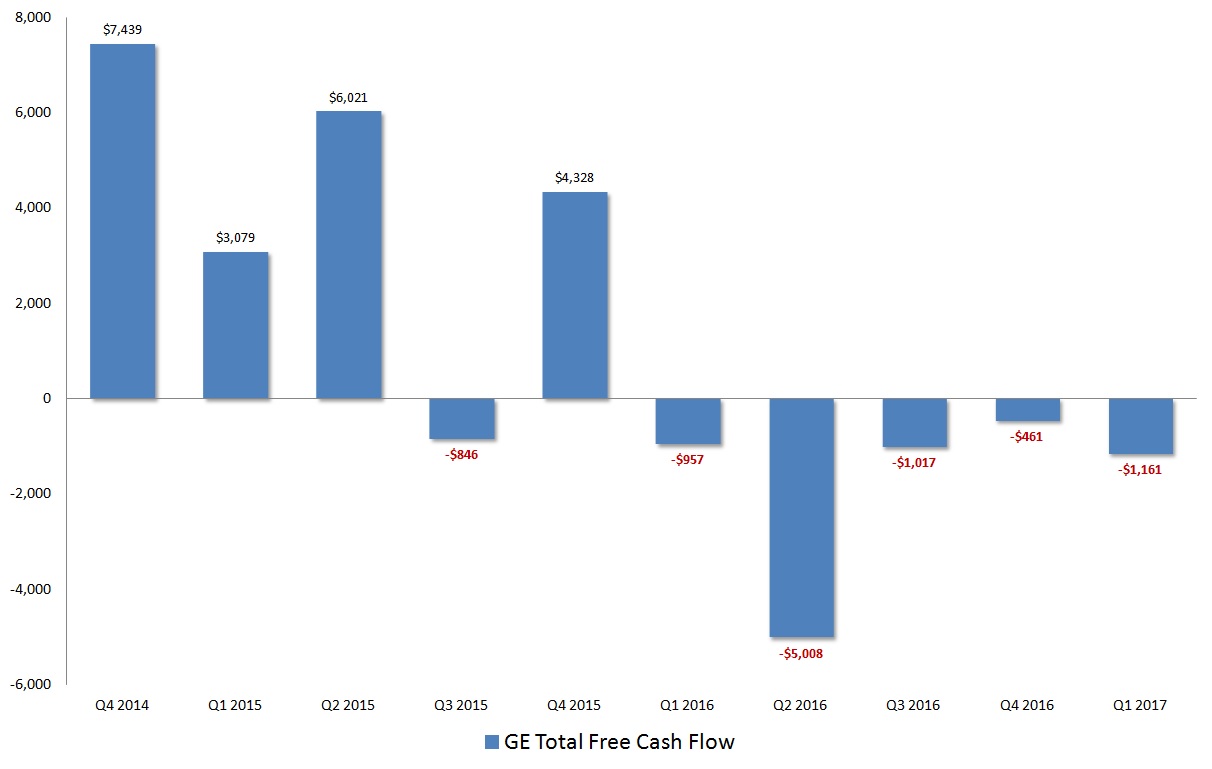

One of the metrics to watch carefully to determine if General Electric is able to do anything they say is free cash flow. In a nutshell, FCF is the money a business can use after it pays off its capital expenditures. No matter how you look at it, FCF is critical towards increasing shareholder value.

But GE stock has a critical problem. Ever since Q3 FY 2015, the company’s FCF has never looked the same. Outside of a positive blip in Q4 FY2015, cash flow is awash in red ink. For anyone to be remotely interested in the stock at this point, this metric has to change significantly.

But again, we run into our initial dilemma. General Electric is so spread out that it has essentially diversified against itself. It’s the classic situation of winners being weighed down by the losers. Since GE is probably not going to divest further — it probably likes being a weird, complicated organization — it’s going to need to find some crazy way to boost valuation.

I’m not going to hold my breath. GE stock is in bearish trend channel for a reason — the markets don’t believe it can legitimately recover. I believe it can, but it will require tough decisions that General Electric doesn’t want to make.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.