Typically, producing a solid, earnings performance sparks a boost in the markets. But with a company the size of Alphabet Inc (NASDAQ:GOOG, NASDAQ:GOOGL), nothing is ever typical. A host of reasons, from less-than-inspiring guidance to investor fears, can trigger an illogical selloff. For GOOGL stock bears, I’d warn them not to go too crazy with their shorting adventures.

As InvestorPlace writer Tom Taulli reports, second-quarter results for GOOGL could be characterized as anything but disappointing.

He writes, “Alphabet’s revenues came to $26 billion, up 21% year-over-year and better than expectations of $25.6 billion. Meanwhile, earnings of $3.5 billion, or $5.01 per share, were down 28% year-over-year, but still far better than estimates for $4.44 per share.”

Yet the day after Q2, GOOGL stock opened the session 2.7% lower than the prior close. Fast forward a few more days to the present, and Alphabet shares are 5% below the price shortly before earnings. That’s quite a remarkable shift against the report’s implications. Still, some method to the bearish madness exists.

First, I think traders got spooked from Alphabet shares’ inability to decisively break resistance at $980. Indeed, as fellow contributor Chris Tyler points out, GOOGL stock formed a bearish double-top formation. Second, investors balked at the 6% quarter-over-quarter, and 23% year-over-year cost-per-click declines. Recall that many analysts, for better or for worse, consider Alphabet to be a one-trick pony. Seeing anything endanger that one trick creates anxiety.

Finally, adding 9,000 employees over the past year is a mixed blessing. Such human resource acquisitions indirectly affirm future growth. Simultaneously, that’s a lot of folks for whom to provide healthcare; however, that mess is going to play out.

But those that are abandoning GOOGL stock clearly lack long-term perspective.

Have Your Cake and Eat It With GOOGL Stock

One of Alphabet shares’ underappreciated attributes is that the underlying company is a play on the future and the present. Many technology-centric organizations must sacrifice a critical component of their business to achieve their ultimate end game. As Sizemore Capital Principal Charles Sizemore mentioned, Amazon.com, Inc. (NASDAQ:AMZN) used to be mocked as the “river of no returns.”

As we all know from its planned Whole Foods Markets, Inc

. (NASDAQ:WFM) takeover, Amazon eschews earnings for growth. Fortunately, Alphabet doesn’t have to eschew either component, and they don’t. Their profitability margins rank among the highest of global internet content and information companies. And while their three-year trailing revenue has softened, the metric is still firmly above average.

GOOGL stock is a rare opportunity for investors to have their cake, and eat it, too!

For starters, I’m not at all worried about the one-trick pony perception. Alphabet, and the Google brand, is a cultural phenomenon. It has entered our lexicon as both a noun and a verb. The lone ace up the sleeve is likely impenetrable, perhaps perpetually so. Its search-engine dominance gives new meaning to the word “dominance.”

But the scary thing is that GOOGL stock has legitimate growth opportunities.

Click to Enlarge

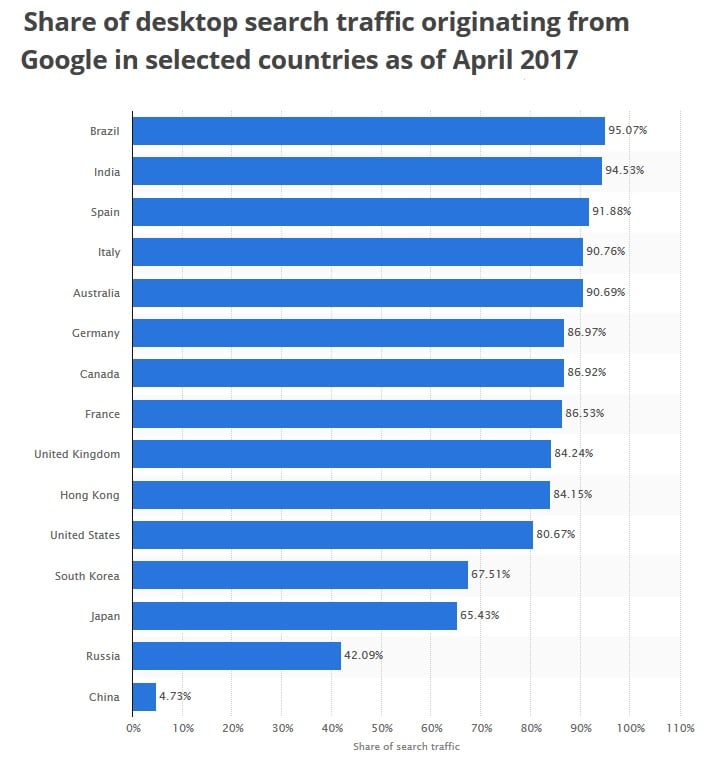

For example, although the Google search engine is the undisputed king, this superiority is largely a western trend. In the east, which includes Russia, Google isn’t nearly as dominant.

As DailyMail.com reported a few years ago, Yahoo! Japan Corp (OTCMKTS:YAHOY) has a stronghold on the Japanese internet market. However, “Japanese Yahoo” is shockingly anachronistic. I really think it’s a matter of inevitability before Google takes over this market, and notches another major country.

Don’t Worry, Alphabet Is in Control

Investors should be careful about reading too deeply into Alphabet’s recent earnings report. True, some of the metrics, as I have mentioned, are not necessarily great. But that by itself isn’t a reason to go bearish on GOOGL stock.

Frankly, you’ll never find a perfect investment. That being said, Alphabet, and a select group of elites, are as close you’ll get. Finding faults in its expenditures and acquisitions, and overanalyzing quarterly engagement trends aren’t helpful. Even worse, they might inspire you to ditch a fundamentally and technically sound security.

Alphabet rarely hits a bum note, whether in the strategic realm or in the markets. So I need to have an extraordinary reason to abandon ship. While recent technical momentum isn’t encouraging, it’s likely the result of the weak hands being flushed out. Once Wall Street gathers itself, I expect bullish continuation.

So please don’t overreact to the latest GOOGL stock news. After a solid, double-digit performance for the year so far, Alphabet shares are taking a breather. You can choose to panic or you can choose to stay calm. History and the forward-looking fundamentals recommend the latter.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.