On Tuesday after the close, Micron Technology, Inc. (NASDAQ:MU) crushed earnings per share and revenue expectations. That explains the 11% rally in MU stock Wednesday and Thursday. But should investors pile in now?

Fourth-quarter revenues climbed an absurd 90% to $6.14 billion. Earnings of $2.02 per share came in 10% higher than consensus expectations. The low end of the guidance range for both metrics next quarter came in ahead of analysts’ estimates. This was in fact, a very good quarter.

It’s also why investors should consider buying despite the rising MU share price. Albeit, with an open eye to risk and acknowledging that they’re late to the game.

Under the Hood

What exactly is going here? On the surface, we have a stock that trades with trailing price-to-earnings (P/E) ratio of 16.5, but at just 5.7 times forward estimates. 5.7 times earnings seem a bit odd for a stock that just grew sales 90% year-over-year. And yes, this is the same company that had a net income of $2.37 billion last quarter compared to a $170 million loss in the same quarter a year ago.

So we have strong earnings and sales growth, but an ultra low valuation. Why? It’s because Micron continually goes through boom-and-bust cycles. Micron primarily deals in DRAM and NAND sales. Because the companies that use these products, ranging from smartphones to automobiles, continue to have strong product demand, demand for DRAM and NAND is through the rough. Supply is so, so tight. And as a result, this gives Micron plenty of pricing power.

Now that sounds like a good fundamental situation, right? It is. But when that supply/demand dynamic unravels, so too does MU share price, (which we’ll examine in a minute).

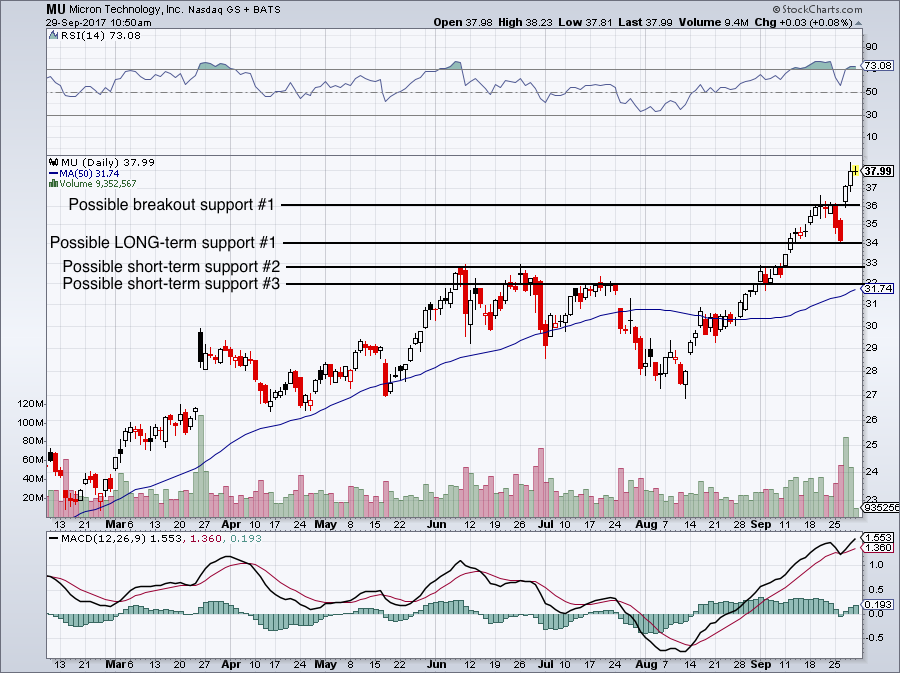

Click to Enlarge

Earlier this summer, despite another strong earnings report, MU stock fell from about $32 to $27 in just a few weeks. This is despite the strong forecast from MU management. As well as forecasts from buyers like Cisco Systems, Inc. (NASDAQ:CSCO) saying they don’t expect DRAM prices to fall anytime soon. Lam Research Corporation

(NASDAQ:LRCX), which makes the equipment to build DRAM and NAND, also said demand should remain strong.

Despite all this, investors ignored it, they had been down this road before. It’s like they already have one foot out the door. But the bears paid the price with MU stock rallying for $27 to more than $38 in just six weeks.

So Is MU Stock a Buy?

As long as the supply/demand dynamic remains in place, the MU share price should head higher. Micron’s valuation is too low and its growth is too strong to ignore. But buyers beware, this can get ugly in a hurry.

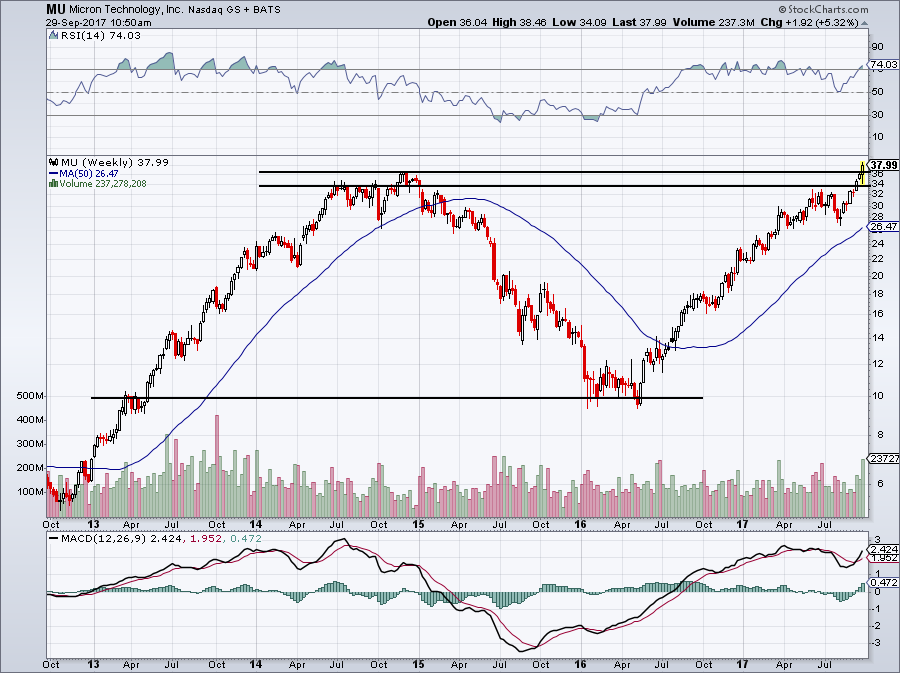

Click to Enlarge

Here’s a five-year weekly chart, as well as a short-term daily chart above. Shares went from $36 at the start of 2015, about where they are now, to $10 by January 2016. The 72% loss in about 55 weeks is not something that commands a premium valuation.

If MU stock traded with a forward P/E market multiple, it would trade around $160, give or take. It’s obviously not going to get a market multiple due to its more volatile business and stock. (Just imagine if the SPDR S&P 500 ETF Trust (NYSEARCA:SPY) went up 500% in two years, crashed 75% the next year, then tripled to current prices). That’s MU stock.

Anyway, new buyers should use caution. MU stock is overbought on the long-term weekly and short-term daily charts. However, there are very tradable levels to buy and sell at.

Investors buying today should certainly keep these levels in mind. $36 is a big, multi-year breakout level. As long it holds above there, investors should be fine. $34 should also act as solid support. If both of these levels fail, investors need to punch their sell tickets or at least pay extra attention to MU share price.

$32 could act as support too, but once MU stock has momentum — in either direction — it’s hard to slow down. For now, I would be long above $34 to $36 and on a break below, remeasure the sentiment around MU share price.

Any talk about new supply coming online could crush MU stock, because so many investors are worried about that situation arising. For instance, If Samsung (OTCMKTS:SSNLF) mentions upping production, it could hurt MU. Just be aware and know your risk.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.