Often, companies complain about not having enough time. For Ambarella Inc (NASDAQ:AMBA), they have too much of it. Unfortunately, that’s not a positive development. In prior years, investors jumped on AMBA stock because the underlying firm had the right mix of performance and potential. Now, it’s just potential, and the markets clearly aren’t liking it.

I don’t know how else you can explain the sudden shock to the system Ambarella stock represents. We’ve barely closed out the first month, and already shares are down 15%. The saving grace is that AMBA is a technology play, and there’s plenty of tech to exploit. For instance, global commercial drone revenues are projected to hit $12.6 billion by the year 2025.

But will these long-term projections be enough for investors to gamble on AMBA stock? I have my doubts.

By the year 2020, analysts forecast drone revenues to hit just under $2.4 billion. That’s a 113% increase from the $1.1 billion in expected revenues this year. While significant, it’s going to be a tough task for AMBA, which just lost its primary customer GoPro Inc (NASDAQ:GPRO).

Actually, the aforementioned statement is not quite accurate. GoPro simply imploded as its action camera and drone sales fell sharply. Worse yet, management announced that it will exit the drone business entirely. Of course, this news is mighty problematic for AMBA since most of its drone demand came from GoPro. Hence, the sharp decline in Ambarella stock.

To be fair, many analysts, such as our own Chris Lau, predicted that drone sales would be disappointing. The real money, as he states, is in the company’s advanced driver-assistance systems (ADAS) and computer vision (CV) technologies.

But can this tech get to market quickly enough to save AMBA stock?

Investor Patience Is an Issue for AMBA stock

I completely agree with Lau and others that CV represents a major leap in terms of driverless technologies. With this new tech, cars don’t just avoid obstacles; they recognize and distinguish several objects (and pedestrians) on the road. Theoretically, that’s a big draw for AMBA.

Lau also points out that CV technology has uses beyond automotive functions. Again, I agree. The ability for the CV-equipped camera to identify people presents obvious utility for military and law enforcement agencies. Government contracts are especially lucrative, which is another big plus for Ambarella stock.

However, as an investment opportunity, I side with MoneyWire editor and InvestorPlace contributor Matt McCall. Last December, he recommended that investors avoid Ambarella stock in the interim, and he was proven correct. More importantly, when you’re dealing with longer-term potential, you’re also inviting longer-term problems.

A major issue with AMBA is competition, especially from the likes of Intel Corporation (NASDAQ:INTC) and Qualcomm, Inc. (NASDAQ:QCOM). McCall states:

“That’s never a good sign for a small player as it is difficult for them to compete with the money behind the big guys. The competition has led to falling margins, which have in turn hurt the company’s bottom line.”

Along that same line, I’m concerned that any shortcomings of ADAS, CV or any other smart tech will disproportionately impact a smaller firm like AMBA. While the CV demonstration at the most recent Consumer Electronics Show was impressive, it was also largely a controlled study. Throw the CV into a truly dynamic, long-term study and then get back to me.

For example, as much as I love Tesla Inc (NASDAQ:TSLA), the media has reported failures of its Autopilot technology. Clearly, critical bugs still need to be eradicated in this next-gen innovation.

Just Like Ambarella Stock, You May Have to Wait

Overall, I’m hesitant to get involved with AMBA stock. However, if you’re thinking about speculating on this company, you have time working in your favor.

Needless to say, Ambarella stock currently stands on precarious technical ground. Given the nature of the company’s challenges, I expect significant downside risks.

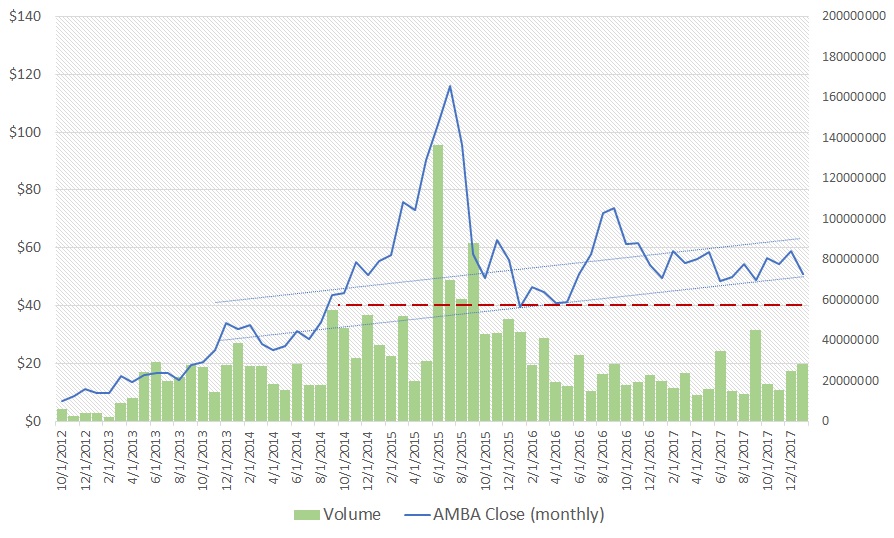

The longer-term picture for AMBA is enticing but only if rising support holds. Should shares drop below $40, I’m not interested in catching a falling knife. Thus, if you want to take a risk, I’d carefully watch this level and proceed with caution.

Click to Enlarge

It’s best if you wait out the markets. I don’t anticipate AMBA stock to suddenly jump up out of nowhere. Wait and see if shares develop some kind of horizontal support. At that time, it may be ideal to speculate. For everyone else, I don’t think Ambarella has enough exciting developments to go all in.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.