Most every investor knows Amazon.com, Inc. (NASDAQ:AMZN) is the dominant name in e-commerce, yet makes most of its money by offering cloud computing services via Amazon Web Services, or AWS. Many owners of Amazon stock may not fully appreciate just how fruitful or unfruitful each of its divisions are. Nor do they realize how quickly each division’s relative contribution to the bottom line is changing.

No, actual profitability has never really been the point with Amazon. Mostly, Amazon.com CEO Jeff Bezos is looking to build a massive marketing machine, and infuse Amazon into every consumer’s daily life. The company can worry about profits after that happens.

But it remains to be seen how, or even if, the company can afford to get to that proverbial promised land.

Breaking It Down

Let’s cut to the chase … well, one of the chases anyway. Amazon.com is an e-commerce juggernaut, selling more and more stuff online every year. Most of that growth is being driven by North American consumers, although Bezos is pushing pretty hard into foreign markets as well. AWS is still a relatively small piece of the revenue pie, but it’s also the fastest growing. The graphic below tells the tale. It’s about as you’d expect.

Click to Enlarge

The question current and potential Amazon stock holders should be asking: Is the bottom line getting better for any of these three arms?

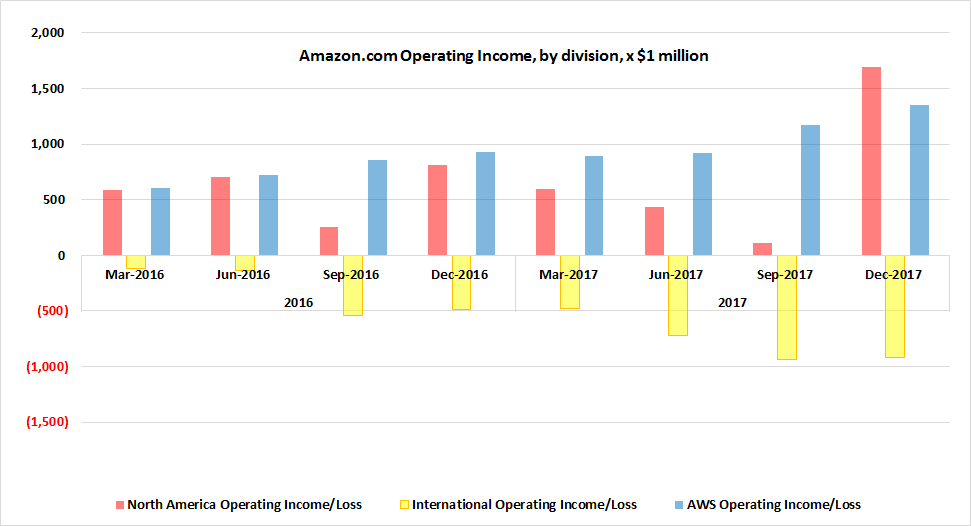

The following graphic answers the question, for better or worse, plotting the operating income for each unit. It won’t take long to see that, overall, Amazon Web Services is carrying more than its fair share of the profit-making weight.

Click to Enlarge

That’s not the only noteworthy nuance packed into the latter image though. As you’ll also see, the company’s overseas operations are not only losing money — the scope of that loss is growing.

It may be worth it. Amazon.com was a habitual money loser in North America as it was growing into the behemoth it is today. Now, Bezos may argue, the company needs to be just as willing to take losses on the international front as it seeks to take root there.

Competition Abroad for Amazon Stock

There is a difference, though. Namely, Amazon wasn’t really dealing with any formidable competition when it was reaching deeper into the North American market in the 1990s and early 2000s. It’s already running into tough competitors like Alibaba Group Holding Ltd (NYSE:BABA) and JD.Com Inc (ADR)

(NASDAQ:JD) in the increasingly important Asian market.

That’s the polite way of saying building a self-sustaining e-commerce operation outside of North America might be a lost cause.

The other curiosity on the graphic of Amazon’s divisional operating income: Until last quarter (which encompassed the usual holiday-shopping frenzy), North America’s e-commerce arm was decreasingly profitable. It’s not exactly clear why the fourth-quarter’s e-commerce business was suddenly so profitable. Most likely it was the combination of several levers the company had been pulling for months before the quarter ended.

Still, it remains to be seen if decent operating margins are the “new normal” for North America’s online-shopping business.

Looking Ahead for Amazon Stock

The overarching defense of Amazon generally starts with (and often ends with) pointing out that no matter what, AWS can carry the company. And for the most part, that’s been true — although that argument is coming into question now.

It’s not quite a convincing concern yet, but during the fourth quarter of last year, Amazon Web Services’ cloud market share fell from 68% to 62%. This was mostly thanks to a growing interest in what Microsoft Corporation (NASDAQ:MSFT) is offering to cloud computing customers.

One quarter does not make a trend, but all big trends start out as small one. And, it’s not the first time we’ve heard about Amazon’s cloud dominance finally being attacked in earnest. Last year, Amazon changed its pricing model for access to its EC2 servers, adjusting them in a way that ultimately translated into less revenue per customer. The move was made in response to pricing pressure from Microsoft, and others. But it was only a microcosm of the brewing cloud-pricing war that will further crimp Amazon’s cloud pricing power.

That’s just a couple of things to think about for Amazon stock owners who believe the company has enough money to remain self-funding for the foreseeable future.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.