Kroger Co (NYSE:KR) has been a tough stock to own, as it’s now caught in a battle with a number of foes. Digitization was an issue for traditional retailers, but it wasn’t supposed to become a problem for grocers. But while Amazon.com, Inc. (NASDAQ:AMZN) acquiring Whole Foods really soured that sentiment, it wasn’t as if Kroger stock was on fire before that mid-2017 announcement.

After nearly doubling from early 2014 to early 2015, KR stock has been dead money for a while. Although it did move slightly higher from $37 — as you’ll see on the chart in a minute — KR has been a mess for a while now. And it’s still down 9% following earnings.

I think most of this boils down to uncertainty, food inflation and concerns about the future of the grocery store. With a lack of food inflation — which admittedly could pick up pace — Kroger has a harder time raising prices in the store. If it can’t raise prices, it’s hard to expand, cover additional overhead and experiment with new initiatives. Of course, pricing pressure also comes from increased competition.

New delivery initiatives like the expanded grocery delivery from Walmart Inc (NYSE:WMT) and M&A moves like the one by Amazon certainly doesn’t help matters. Will they bankrupt Kroger? No, but they could certainly pinch margins and make life more difficult. If anything, it raises investors’ concern about the future of Kroger, which weighs on the stock price.

I will point out that the company recently tried to buy Boxed, an e-commerce wholesale/warehouse company, for $400 million. This actually would have been a solid move for Kroger, particularly as it puts more effort into its digital sales.

Valuing Kroger Stock

Despite margin concerns, competitive worries and long-term potential threats, KR stock remains profitable. Plus, it’s cheap — but for a reason.

Kroger stock trades at a meager 10.4 times forward earnings estimates. Analysts expect earnings growth of just 1.5% this year and 8.2% in the following year. As for sales, analysts are looking for revenue growth of 0.2% this year and 3.4% next year. Expectations are rather low for this year. But it’s quite possible that next year’s estimates remain too optimistic. Given the industry concerns, I personally would use a lower growth rate. Although it’s tough to say what it should be, being this far away from 2019. Again, this circles back to the uncertainty, which forces a lower valuation on the stock. Investors hate uncertainty.

Kroger stock also pays out a 2% dividend.

Here’s the issue, though. Kroger has sub-2% operating margins and profit margins of just 1.5%. So as competitive pressures heat up or the company ratchets up spending to expand growth initiatives, there’s not much wiggle room on the bottom line. That’s not a good situation to have, even if Kroger is a great operator.

Trading KR Stock

It’s a coin toss for investors on whether KR stock is right for their portfolio. For me personally, I don’t see enough of a reason to get long. It’s not because Kroger is a bad company; it’s because it’s stuck in no man’s land.

The growth and margins are too low to make it attractive vs. high-growth, strong-margin companies. Yet its valuation isn’t low enough and its yield isn’t high enough to make it attractive vs. other low-value, high-yield stocks. For instance, a stock like General Motors Company (NYSE:GM) is more attractive to me in this category.

That’s not keeping the analysts away, though. The last five reports have issued or upheld price targets between $26 and $31. Their average price target comes out to $27.70, roughly 18% above KR stock’s current price of $23.40.

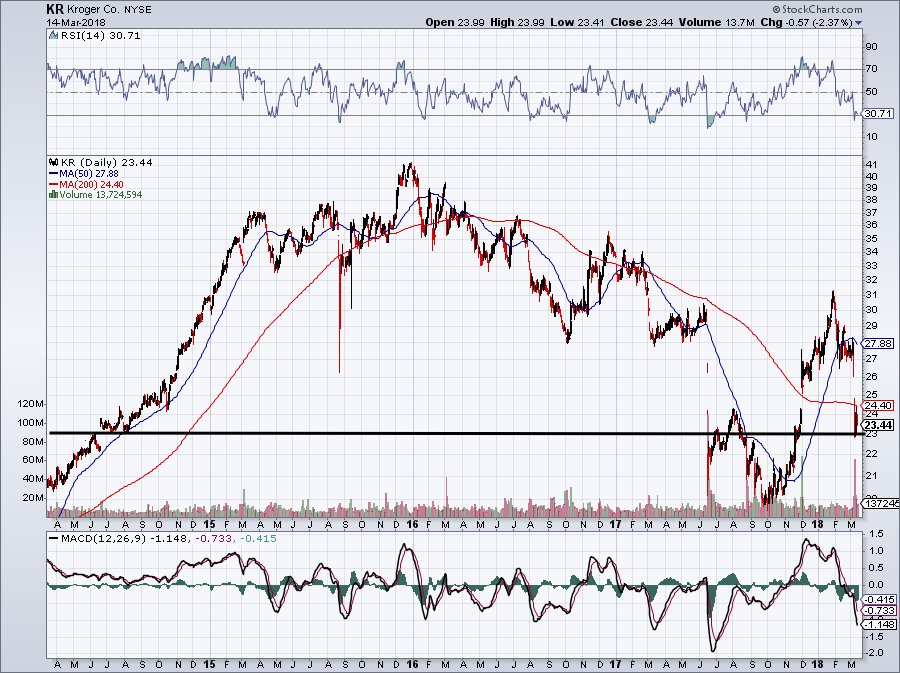

Click to Enlarge

Investors who want to take a shot on KR stock can do so with shares near current levels.

Roughly $23 should act as support for the grocery chain stock. If it holds, perhaps Kroger stock can rebound back toward $27. But if it fails, shares could drop back down to $20, its recent low. This at least gives investors a solid risk/reward setup as they can keep their losses small by exiting their position on a close below $23.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.