One of the brightest names on Wall Street last year was Shopify Inc (NYSE:SHOP), and for good reason. E-commerce is simply the name of the game in the retail business, and Shopify’s platform is one of the best. However, SHOP stock is no longer looking like the market killer it once was.

Since the close of March 20, Shopify stock is down a stunning 20%.

It couldn’t make any progress on Monday following China’s retaliatory tariffs and fears of an escalating trade war. But prior to this geopolitical drama, several analysts were concerned about the broader markets getting overheated. Now, those concerns seem more than justified, especially in the technology sector.

To be fair, SHOP stock is still one of the top names on Wall Street. On a year-to-date basis, SHOP is up 20%, a resounding performance given the circumstances. And while the recent selloff is dramatic, it’s not the first time that the company has fought back from trouble.

Last year, between Oct. 2 and Oct. 10, Shopify stock tanked more than 22%. Citron Research analyst Andrew Left, a noted short-seller, aggressively questioned Shopify’s business model. The notoriety hurt for a little bit, but shares quickly brushed off the pain. The company went on to return more than 133% for that year.

The lesson is clear: doubt SHOP stock at your own risk! However, I think Shopify could face sharper challenges this time around. For one thing, the China trading dispute could escalate. So far, the Chinese response has been measured, but calm rationality is a luxury for this administration.

What does that have to do with Shopify stock? Many successful Shopify businesses are in the apparel and fashion business, which often utilize Chinese goods and services. Moreover, just the escalation fear is worrisome.

It’s Not just China or the Markets Pressuring SHOP Stock

Unfortunately, the China tariffs and the broader market troubles aren’t the only pressure points. Citron’s Left is back at it again, this time claiming that Facebook, Inc.’s (NASDAQ:FB) recent controversy will taint SHOP stock. Shopify depends heavily on Facebook’s goldmine of two billion active users.

For full disclosure, I genuinely believe that the social media giant’s scandal will blow over. If you look at the finer details, the company is guilty of facilitating a privacy violation. It’s a serious issue, but nothing worth hysteria, in my opinion. Still, Left is correct: poor investor sentiment could turn around and hurt Shopify stock, especially if the government regulates the social media industry.

But the biggest headwind could be Shopify’s

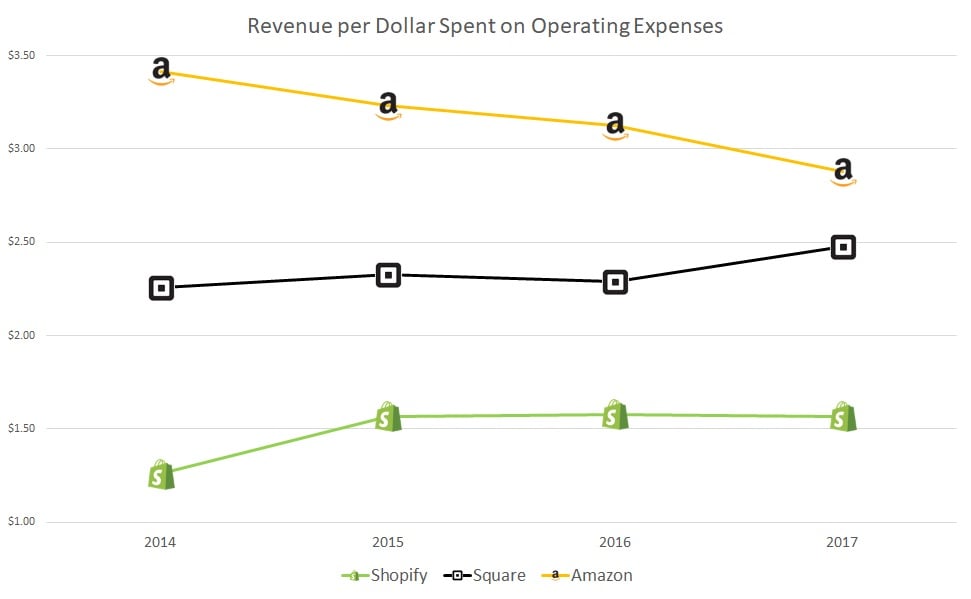

fundamentals. Over the past four years, the company’s revenues have skyrocketed from $105 million to $673.3 million. But in order to obtain that growth, management of course needs to constantly invest in their business. Obviously, expenses have also skyrocketed.

Click to Enlarge

For instance, Square Inc (NYSE:SQ) has a similar business to Shopify. Its revenue per dollar spent last year was $2.48, which is significantly higher than SHOP. In addition, this metric has been largely growing over the past four years. Consequently, SQ is a high-flyer in the markets, and no one’s questioning its business practices.

You can also look at Amazon.com, Inc. (NASDAQ:AMZN), which offers a robust e-commerce platform. Last year, its operational dollar generated $2.88 of top-line sales, which decreased significantly from years back. However, it’s the alpha dog fighting to keep first place.

Shopify Stock Has Run Up Too Far, Too Fast

Shopify is in the completely opposite role relative to Amazon. It’s an upstart that should be experiencing rapid growth, like comparing an adolescent to a mature adult. Instead, it has growth metrics that are weaker than long-established names.

To me, that doesn’t make much sense. A company’s younger years benefit from the law of small numbers. A $2 million year from $1 million is a 100% growth increase. A $100 million year from $99 million is only a 1% growth rate.

I’m not the only one that feels this way. Two months ago, our own Lawrence Meyers railed against SHOP stock, calling its rally “sheer lunacy.” Meyers wrote:

“A billion dollars in revenue and only break-even? I’m sorry, I don’t get it. Actually, I do. SHOP stock has a business model that is essentially selling business opportunities through affiliate marketers, and depends on affiliate marketing for growth. Sound familiar? Yes, I agree with Andrew Left at Citron Research.”

From what I can see, break-even is probably the best the company can do right now. Management is very ineffective at generating growth relative to the competition. I think the difference right now is that more investors are catching on. Combine that with all the other potential pressures for Shopify stock, and this situation is easy to call: I’m out.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.