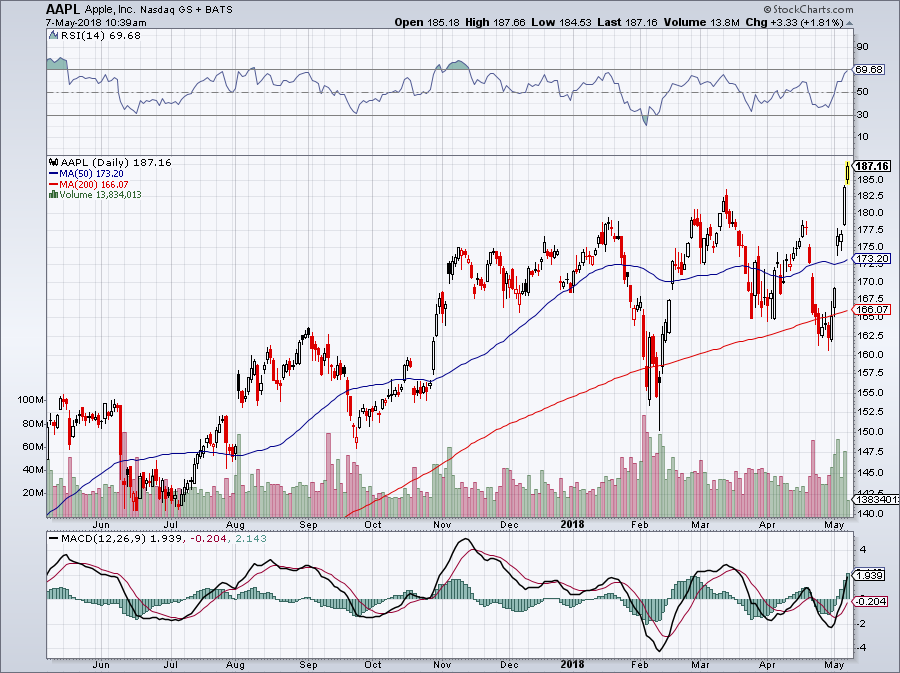

Last week, Apple Inc. (NASDAQ:AAPL) beat on earnings per share and revenue expectations. Unlike a number of companies, Apple stock actually rallied on the good news, rather than falling. Shares have been moving higher ever since, climbing about $20 apiece through the end of the week.

While it’s a big move, investors can bank on even more upside, because Apple’s market cap is heading to $1 trillion. Currently, it stands at about $933 billion. Although the move to $1 trillion represents just over 7% upside, let’s not act as if there weren’t other times to buy Apple over the past few years, or heck, months, before it hit new all-time highs on Friday.

With that in mind, here are a few reasons why Apple is heading higher.

Big Buyers of Apple Stock

Aside from Apple stock being the largest holding in the SPDR S&P 500 ETF Trust (NYSEARCA:SPY) and PowerShares QQQ Trust, Series 1 (ETF) (NASDAQ:QQQ), Apple is also a big buyer of its shares.

Last week, management announced it would buy back $100 billion worth of stock, following previous announcements of $50 billion over the past few years. That puts a natural bid under the stock price, as the company is constantly accumulating its stock.

Remember, business remains strong and as a result, Apple will continue buying back stock in the future as it generates more cash. It’s not as if this is a one-time repurchase program.

Also don’t forget other fund managers. Warren Buffett recently announced his Berkshire Hathaway Inc. (NYSE:BRK.A, NYSE:BRK.B) recently bought another 75 million shares of Apple stock. The conglomerate now holds more than 200 million shares of Apple, good for a ~5% stake in the company.

He’s not the only one buying either, but when Buffett is buying it inspires a lot of confidence. Whether it’s other fund managers or retail investors, there is optimism behind his actions.

AAPL Valuation

One skyrocketing stock with a ballooning market cap is

Amazon.com, Inc. (NASDAQ:AMZN). But unlike Amazon, Apple’s valuation is much more reasonable. AAPL now trades at just under 16 times this year’s earnings and about 14 times next year’s estimates.

While that’s a higher valuation than the tech giant has traded at in recent quarters, it’s still not expensive. Consider that Apple has one of the most recognizable brands, a fortress balance sheet and is still growing.

Analysts expect Apple’s earnings to soar 24% this year before jumping another 15% in 2019. On the revenue front, analysts are looking for growth of 14% and 4% this year and next, respectively.

Click to Enlarge

In essence, we have above-average growth and a below-average valuation to go along with an unprecedented capital return program and an incredible business. It might be a stretch to call Apple stock a bargain at this point, but it’s hard to argue that it’s a poor stock to own.

Not that it’s huge, but also consider that AAPL pays out a 1.6% dividend yield.

Apple’s Business Remains Strong

The valuation would be meaningless if not for the health of Apple’s business. We’re entering the “slow” period of Apple’s sales year, as consumers have had two quarters to gobble up its new devices and as many start holding out for new releases later in the year. Yet Apple’s mid-point revenue guidance of $52.5 billion came in above consensus estimates of $51.6 billion.

Apple selling more than 52 million iPhones in the quarter is the obvious sales driver for the company. But the number that stood out most to me came from Services. The high-margin segment saw sales surge 31% year-over-year to $9.2 billion, crushing estimates of just $8.4 billion. Last quarter, Apple’s Services unit grew “just” 18% YoY.

If we broke out Apple’s Services business, it would be a massive company on its own. I mean, the unit had more than $9 billion in sales this quarter!

As this segment continues to gain momentum, its high margin profits continue to bolster the bottom line. Services revenue can’t grow without high engagement on Apple products, which based on its sales, is doing pretty well.

The bottom line is pretty simple: business is going well, Apple stock is reasonably priced and management is gobbling up a ton of shares. Why shouldn’t we?

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held a position in AAPL.