Just days before reporting earnings, Yum! Brands, Inc. (NYSE:YUM) was hitting new all-time highs. But since hitting those highs, YUM stock has been in retreat. That’s despite rebounding from its post-earnings slump.

After the company beat on earnings per share and revenue expectations — and rather handedly at that — it’s got many investors wondering if this is an overreaction to Yum earnings.

Does it make Yum stock a buy?

A Look at YUM Earnings

Adjusted for a one-time item, earnings came in at 90 cents per share. That was vastly ahead of the 68 cents per share in earnings that analysts were looking for. On the revenue front, its $1.37 billion in sales beat expectations as well.

The company operates a trio of global restaurant chains, that being KFC, Taco Bell and Pizza Hut. That’s with the exception of China, which operates under Yum China Holdings Inc (NYSE:YUMC).

While the headline numbers looked good, same-store sales (SSS) were a disappointment, increasing just 1% globally. That’s below analysts’ estimates looking for 2% growth. Operating margins at KFC grew 5.3% to 33.6%, but both Taco Bell and Pizza saw declines.

Further, YUM got a boost from forex gains, which isn’t a bad thing by any means. But it’s not a gain from the business, which makes it feel temporary, rather than a tangible operational improvement.

I think the same-store sales figure is what hit YUM stock the hardest.

Valuing YUM Stock

It’s not that YUM is a bad company by any means, but I’m finding the catalysts for owning it from a fundamental perspective becoming more difficult to believe. For instance, what would Starbucks Corporation (NASDAQ:SBUX) stock look like if it had spun off its robust China operations?

Sure, the stock would likely gain over the next nine to 12 months (like YUM did), but then what? What would investors think of its now 3% SSS figure rather than the 5% SBUX used to churn out? What would they think without that big growth catalyst in China?

That’s the feeling I’m getting toward YUM. Here’s a company that had spun off its growth catalyst to create value for shareholders and now has a good, but not great global business (ex-China). Plus, other options seem more attractive.

As of March, Chipotle Mexican Grill, Inc. (NYSE:CMG

) is being run by Brian Niccol, who most recently served as the CEO of Taco Bell. And with that, CMG has the wind at its back, and the stock is surging. When it comes to Pizza Hut, no one is operating better in the segment than Domino’s Pizza, Inc. (NYSE:DPZ).

YUM doesn’t scream value either, trading at 24 times this year’s earnings estimates, which are set to grow about 11% year-over-year. It’s 1.8% yield isn’t a must-have either. From a fundamental perspective, I can see why investors aren’t tripping over themselves to buy YUM stock.

Trading YUM Stock

But what about from a technical perspective?

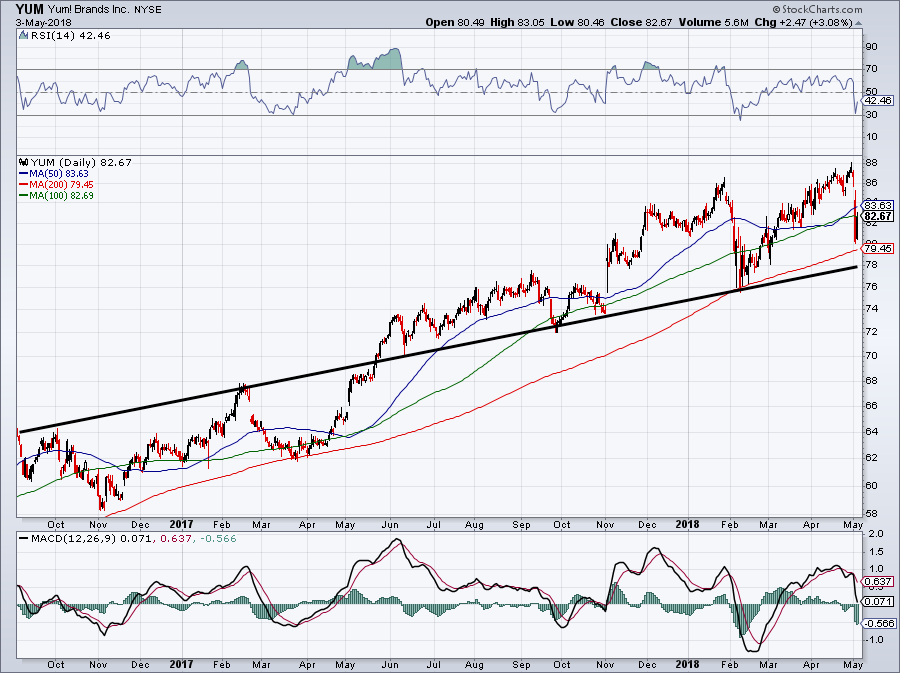

Each decline to the 200-day moving average has been gobbled up by investors. This trend has been going on for more than a year, and that latest retest (well, almost retest) could signal that YUM stock will bounce once again.

Click to Enlarge

Now shares are back to the 100-day moving average, and investors are likely scratching their heads on where the stock is heading now. Above the 100-day and 50-day moving averages and YUM stock will likely retest its former highs. Should shares fail to push through these levels, though, a retest of the 200-day moving average is more likely.

Will it keep bouncing if this level is tested again? Initially, it probably will, but remember that the more times a stock tests a level, the more likely it is to break. On the conference call, CFO David Gibbs talked about the upcoming second quarter being the worst of the year “most likely.” I believe he was only referring to KFC in the U.K.

But still, it got me thinking that perhaps YUM stock may tread water for a little while longer, as it lacks any major short-term catalysts.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held a position in SBUX.