Like most of tech, shares of Paypal (NASDAQ:PYPL) have struggled lately. PYPL stock is down 11% over the past few trading sessions following the company’s earnings results. So is now the time to buy?

PayPal Earnings (and Venmo)

The first reason to buy PYPL stock? Its last earnings report. On July 25, PayPal reported earnings of 58 cents per share, which came in a penny ahead of estimates and grew more than 30% year-over-year (YOY). Revenue of $3.86 billion squeaked by expectations and grew 23% YOY.

Not bad.

So why then is the stock lower now than when it reported? It makes no sense. The company processed $139 billion in payment volume last quarter, up 29% YOY. Total payment volume at Venmo exploded 78% YOY. Venmo is a hidden growth gem inside of PayPal. In my view, it’s what Instagram is for Facebook (NASDAQ:FB), albeit on a smaller scale.

More importantly, it boosted its third-quarter forecast for both sales and earnings. Further, it did the same thing for its full-year outlook. If only there were something else to bite into. Oh yeah, it announced a $10 billion buyback, which will begin when its $5 billion program is complete.

One hangup? Free-cash flow (FCF). In the press release, it showed that PYPL generated a $170 million deficit in FCF. Yikes — that’s not good. And it’s one reason investors could be sellers of the stock. But really, it was an accounting situation. From the conference call: “However, on a normalized basis, adjusting for this accounting designation, our free cash flow in the second quarter was $737 million. This equates to approximately $0.19 of free cash flow for every dollar of revenue.”

That last line — about its free cash flow generation — is superb. The quarter wasn’t necessarily perfect, but it shouldn’t be down on this. It was a great three months of business for PayPal.

Valuing PYPL Stock

Based on the last quarter, there’s no way we can call PYPL stock a sell. Its valuation though? More questionable.

Shares trade at 35 times this year’s estimates, but a more reasonable 29 times next year’s estimates. The valuation goes down so much because PayPal is still growing so quickly.

Analysts expect 18% sales growth this year and another 16% in 2019. On the earnings front, estimates call for 23% growth this year and 20% in 2019. Keep in mind, PYPL just raised its outlook, so 2019’s estimates could be conservative.

The valuation is tough for some investors to swallow. But I’m sorry, premium companies come at a premium valuation. The second reason to buy isn’t necessarily the valuation. It’s most certainly the growth — although the valuation is more compelling than Square (NYSE:SQ).

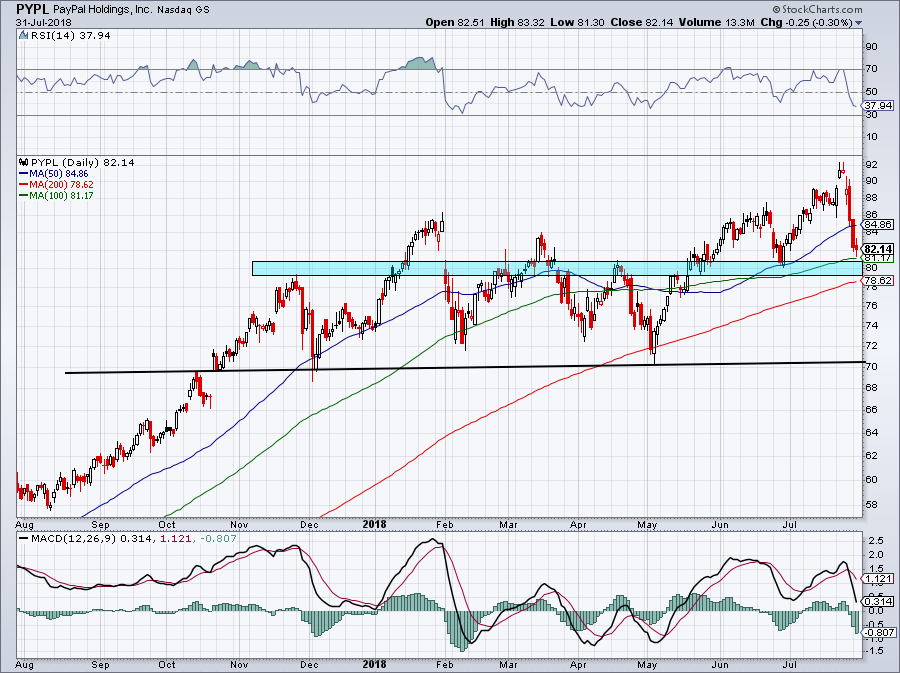

Click to Enlarge

The third reason sits on the charts.

PYPL stock has been in a strong uptrend for quite some time. It’s range is somewhat wide, but suffice it to say, shares have spent plenty of time between $70 and $80 in 2018. Now just above that area, PayPal should have some solid support nearby.

First, the 100-day moving average held as support on Tuesday, while the 200-day is nearby at $78.60. It’s prior range should act as support as well.

That said, investors can go long near current levels or on a slightly deeper pullback. On a close below the 200-day, perhaps we move on. But this story is still quite good.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.