To be clear, Raymond James’ analysts made a good point about Pandora Media (NYSE:P) in Wednesday’s updated notes to investors, underscoring the company’s “Strong buy” on not just Pandora stock, but rival Spotify (NYSE:SPOT) as well.

That is, the two “pure play” names continue to see significant numbers of downloads of their respective apps, reinforcing Raymond James’ stance “that pure-plays have a stronger than perceived competitive position.”

It’s an indirect hint that consumers like the fact that the two services aren’t device-specific, and will work on most anyone’s hardware.

Yet, the firm’s optimism glosses over an overarching reality… two, actually.

One is that Pandora is still dipping deep into the red ink. The other is that if Pandora even just starts to look like it will be able to swing to the expected profit analysts collectively see in the cards several quarters from now, competing providers will step up their digital music offerings.

Just ask Netflix (NASDAQ:NFLX), which is seeing it happen within the market it largely cultivated by itself.

Misplaced Optimism

The premise is one that doesn’t quite jibe with the performance Pandora stock has dished out since hitting multi-year lows near $4.00 early this year. Pandora stock presently is trading above $9.00, up more than 125% for the past six months, mostly in response to the new-and-improved Pandora Premium and the rollout of programmatic ad sales.

Analysts, and now investors, expect big things from both initiatives. Namely, the pros are now looking for the streaming audio company to do something it’s never done before: turn a quarterly operating profit by the last quarter of 2020. Progress towards that goal will be gradual, but measurable.

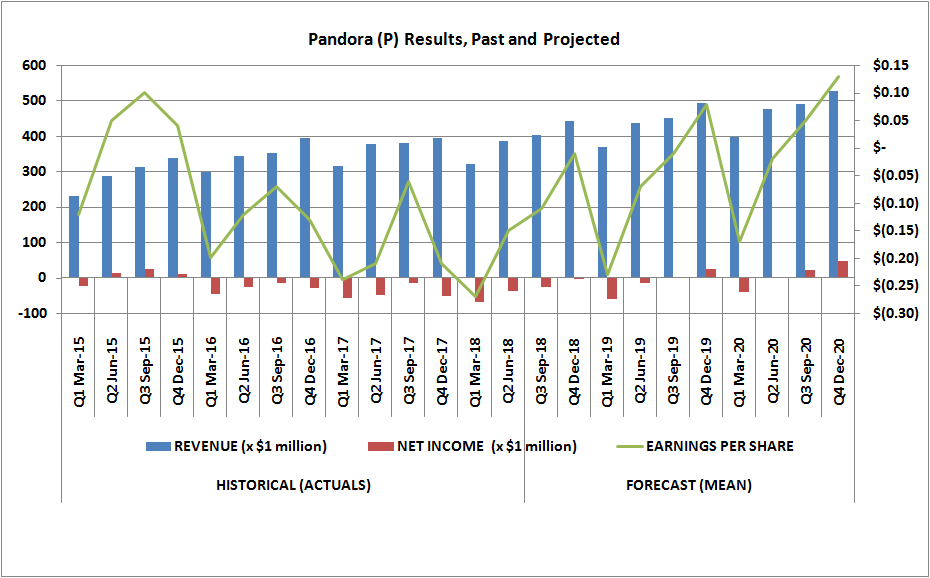

Click to Enlarge

Certainly anything’s possible, but a closer look at the company’s historical results reveals Pandora isn’t making any profit-progress at all. Indeed, its losses are widening as it grows the top line. Something dramatic is going to have to change to meet its lofty goals, and it’s not clear the new iteration of its Premium service or programmatic ads are the proverbial magic bullet.

The headwind may not be how it serves customers and advertisers though, but instead a flawed business model itself.

Pandora Stock Has No Moat

Although Pandora and Spotify are unique in how they address the market, their pure play nature and their flexibility may be of more interest to analysts looking to bolster a bullish call than to consumers themselves.

Music lovers just want a service to work, and their loyalty to a particular platform may be little more than a function of simplicity and easy access.

Enter

Apple (NASDAQ:AAPL), Amazon.com (NASDAQ:AMZN) and Sony (NYSE:SNE), each of which offers digital music, but none of which have aggressively pushed their offerings in a way intended to stop Pandora in its tracks.

That could change in an instant, and would likely change the minute it becomes clear that digital music, when delivered the way consumers want it, can be a legitimate profit center.

It’s a scenario not unlike the one Netflix fell into roughly a year ago.

It was essentially the only pure play name in the business a few years ago, but rivals were content to let Netflix take control of that market simply because it was a money-losing business.

Once Netflix began turning significant and sustainable profits just a few years back, however, competitors crawled out of the woodwork. CBS All Access, Huly, HBO Go, DirecTV Now, Sling and a slew of others are all rivals that materialized in response to Netflix’s success.

Netflix is still the market leader, but time and deep-pocketed rivals both are working against the dominant name in the business.

Pandora is starting the same leg of its journey with a significant disadvantage. Netflix was starting out some semblance of profitability and it was already the market leader and could leverage its name. Pandora isn’t a clear leader of the highly-fragmented streaming audio market, and the cash-strapped, cash-burning company may struggle to fund the initiatives it needs to embrace.

Bottom Line on Pandora Stock

And to be clear, Apple is already in the digital music business. It has been for years, but has only recently opted to focus on growing its service arm where its streaming audio business is operated.

Amazon’s streaming music offerings, meanwhile, don’t appear to be a priority, and it remains a bit unclear to would-be subscribers exactly how to sign up, and what they get; some music can also be accessed using a Prime subscription.

Regardless, the moment Amazon better defines and starts to promote its music platforms, it too can leverage its name, and then monetize those subscribers in a myriad of ways.

As for music giant Sony, it’s still not clear what its newly-revamped effort to become a serious digital/streaming audio outfit will look like. But, with Sony’s recently-announced acquisition of EMI, Sony’s catalog of music effectively doubled.

Also noteworthy is that streaming music revenue was up 32% last year for Sony, a year in which it was only starting to figure out where it fits in the new music marketplace.

None of these other providers quite what Pandora does but that could change in an instant.

None of this is to say Pandora is doomed. It is to say, though, if you bought Pandora stock anticipating that it’s going to eventually dominate this still-fragmented industry, think again. Anything Pandora can do, someone else with a fatter wallet can do just as well, if not better.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.