Shares of Mylan (NYSE:MYL) plunged in Wednesday trading after the company reported disappointing fourth-quarter results. Mylan stock fell as much as 15% as a result and made new 52-week lows. This morning, MYL is up 1.5% from yesterday’s lows.

What’s going on with this stock and is it worth a deeper look?

With GAAP earnings of just 10 cents per share, and non-GAAP Earnings of $1.30 per share missing consensus expectations by 5 cents a share, the report is not being received well. Revenue of $3.08 billion did marginally beat analysts’ expectations by $20 million, but sales contracted 4.9% year-over-year.

The results are even worse under the surface, which is one reason why the GAAP and non-GAAP results are so different. Net income of $51 million plunged almost 80% from the prior year, which is exactly why so many companies lean on non-GAAP results when reporting. In this case though, not even non-GAAP could save Mylan stock. Non-GAAP net income still fell 12.5% year-over-year and earnings of $1.30 per share tumbled 9.1%.

Valuing Mylan Stock

It was an interesting quarter capping off an interesting year. While European and worldwide orders did well in 2018 — up 5% and 7% ex-currency, respectively — North American orders suffered, down 18% for the year. This was explained away:

“[The sales decline was] primarily due to lower volumes on existing products, including the EpiPen® Auto-Injector sales, which was primarily driven by the divestiture of certain contract manufacturing assets, the loss of exclusivity of certain products, actions associated with the restructuring and remediation activities at the Morgantown plant and the timing of purchases of our products by customers.”

On the plus side, operating cash flow of $2.34 billion grew 13.6% year-over-year and adjusted free cash flow came in at $2.7 billion for the year. Unfortunately, guidance was so kind. Management expects adjusted free cash flow of just $1.9 billion to $2.3 billion in 2019. While the midpoint of their revenue outlook of $11.5 billion to $12.5 billion is technically ahead of the $11.86 billion analysts expect, the company’s earnings outlook is baffling.

Guidance calls for non-GAAP earnings $3.80 per share to $4.80 per share. Not only is that a miraculously wide range, but it could likely mean a decline from the $4.58 per share the company reported in non-GAAP results for fiscal 2018. According to analysts, they were looking for earnings growth to $5.04 per share in fiscal 2019, while management was not able to provide a GAAP outlook at this time.

Mylan stock is down more than 30% from its 52-week highs. However, without a dividend to support its share price, I see no reason to buy this name. Its fundamentals are deteriorating and its metrics are under pressure.

Trading MYL Stock

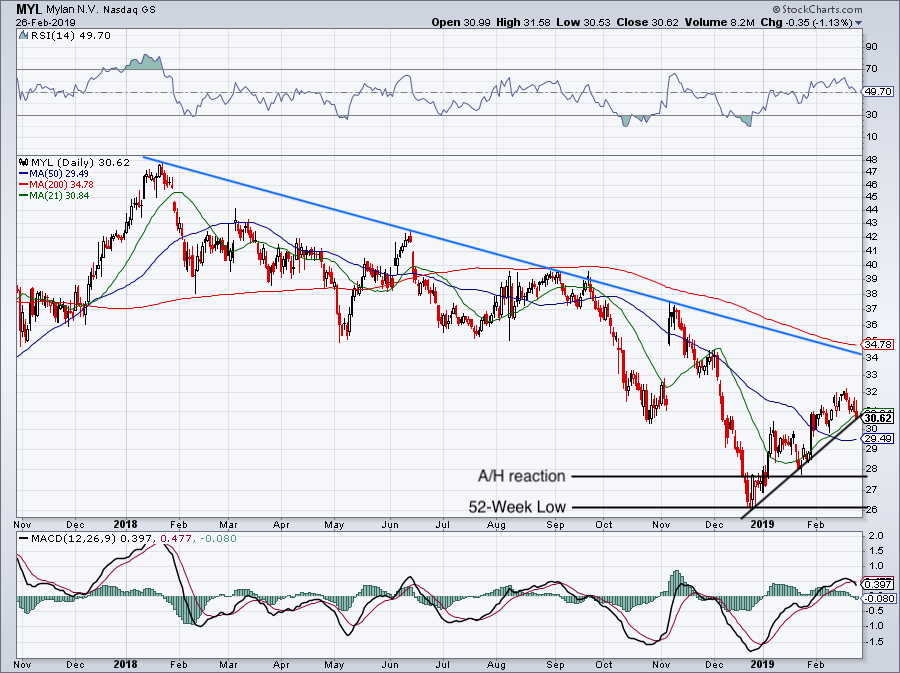

Click to Enlarge

The story doesn’t improve for MYL stock when we look at the charts either.

Mylan stock has been trapped in a nasty downtrend, which began just over a year ago. Until Wednesday, the recent trading had been encouraging. MYL stock was trending higher and was resting above both the 50-day and 21-day moving averages. It still had more than 10% in potential upside before running into the 200-day moving average and downtrend resistance.

This is why we don’t guess ahead of earnings.

Now MYL has hit 52-week lows. With this kind of report, guidance and no dividend yield, I actually expect Mylan stock to print new annual lows. This stock is in a nasty downtrend and it’s not over yet. Clearly investors thought the company was doing better than it is, hence the reaction to its fourth-quarter report.

Mylan stock is not want one I want to own right now. I’d much rather be long Johnson & Johnson (NYSE:JNJ) even amid its talc powder issues, or Celgene (NASDAQ:CELG) amid Bristol-Myers’ (NYSE:BMY) planned $74 billion takeover.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long CELG.