Shares of Sony (NYSE:SNE) are being hammered after the company released its fiscal third-quarter earnings results. With its low valuation and SNE stock almost 25% off of 52-week highs, some are wondering if now is an opportune time to scoop up the shares while they’re under pressure.

At $65 billion, Sony’s not a small niche player. In fact, it has a number of businesses, ranging from music, video games, pictures, imaging, semiconductors and more. Still, Sony came up short for the quarter. Sales of 2.4 trillion yen ($21.84 billion) badly missed expectations of 2.67 trillion yen. Not only did revenue miss estimates by about 10%, they also declined 10% year-over-year. Profits also surprised, with the 377 billion yen result missing estimates of 384 billion yen.

That said, Sony gave a significant bump to its full-year guidance. The company now expects fiscal year profits of 835 billion yen vs. 705 billion yen offered up in management’s October outlook. That’s good for an 18% increase.

Valuing SNE Stock

For the year, analysts are looking for Sony to generate about $79.5 billion in sales — leaving the stock to trade at less than 1x revenue. That’s not all that surprising, given how much hardware Sony produces. At the same time though, it’s quite profitable and as a result, reminds me of a company like Micron (NASDAQ:MU) or other low-valuation tech companies. Albeit, SNE stock has a higher valuation than Micron, — a 9.64x price-earnings multiple compared to MU’s 3.24x — but it certainly is not commanding the type of premium that comes with a stock like salesforce.com

(NYSE:CRM) or Workday (NASDAQ:WDAY).

Full-year estimates call for earnings per share of $5.01, a massive 43% increase from last year’s $3.50 a share. Based on 2019 numbers, that leaves SNE stock trading at just 9.2x this year’s earnings estimates. That’s a pretty low number, given the solid earnings growth. Further, revenue expectations call for 3.2% growth in 2019.

However, some of the investor hesitation may come from 2020 forecasts. Fiscal 2020 is just one quarter away from now and estimates aren’t calling for robust growth. Currently, sales are forecast to climb just 30 basis points while earnings are actually expected to fall 14.5% to $4.29 per share. Based on 2020, Sony stock actually trades at 10.7x earnings estimates.

While both valuations are admittedly quite low, investors don’t want to be in a company that’s not growing its bottom line. SNE stock is a tough one though. Revenue estimates just came up very short in the quarter, meaning that perhaps full-year 2019 and 2020 revenue estimates are too aggressive. That Sony boosted profit guidance for the year, though, suggests that maybe 2020 estimates are too conservative.

This is what we call a very mixed bag and when there’s a lack of clarity, stocks tend to decline.

Trading Sony Stock Earnings

Click to Enlarge

That uncertainty is exactly what we have with Sony stock, along with a lack of catalysts. I would say by a sum-of-the-parts valuation that SNE stock is undervalued. It’s likely that many people agree with that thinking, but rarely does the market suddenly wake up and decide to put a market multiple on a stock based on a sum-of-the-parts thesis. That’s up to investors who want to hold for the long term.

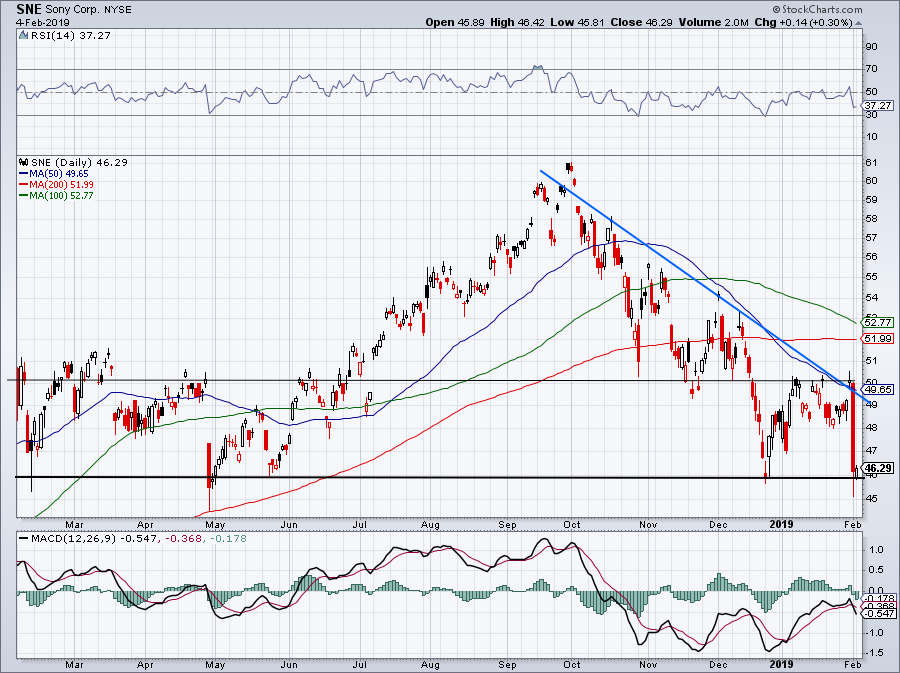

For the short term, there are the traders. I don’t like seeing Sony stock being squeezed against downtrend support (blue line). It’s clear that the $45 to $46 area is support, but how long can it hold up? As the trading wisdom goes, the more times a level is tested, the more likely it is to give way. While we could get a rally from $46 to $49 — good for more than 6% — I need to see SNE stock move through resistance to believe the rebound will stick.

If it doesn’t, look for resistance to push Sony stock back down to support. Those trading SNE stock right now can use Monday’s low at their st0p-loss.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.