When investors are looking for future growth candidates, they often think of names like Netflix (NASDAQ:NFLX), Amazon (NASDAQ:AMZN) or Salesforce (NYSE:CRM). “But I missed most of the rally,” they say. That’s because they’re looking at these companies after they’ve gone from a $10 billion valuation to a $100 billion. Finding these stocks when they are mid-cap growth stocks can be a portfolio-changing phenomenon.

I’m not trying to play up mid-cap growth stocks too much. After all, many times these companies have little to no profits and the stocks have high valuations. Further, their price action tends to be super volatile, both on the upside and the downside. They also aren’t mature, meaning their business models can either deteriorate or strengthen over time, depending on how management adapts to new challenges.

It makes picking names in this group hard, but quite rewarding when investors hit a few home runs. Let’s look at seven mid-cap growth stocks now to see which ones could pay off big-time in the future. Mid-cap stocks are those that have a valuation between $2 billion and $10 billion.

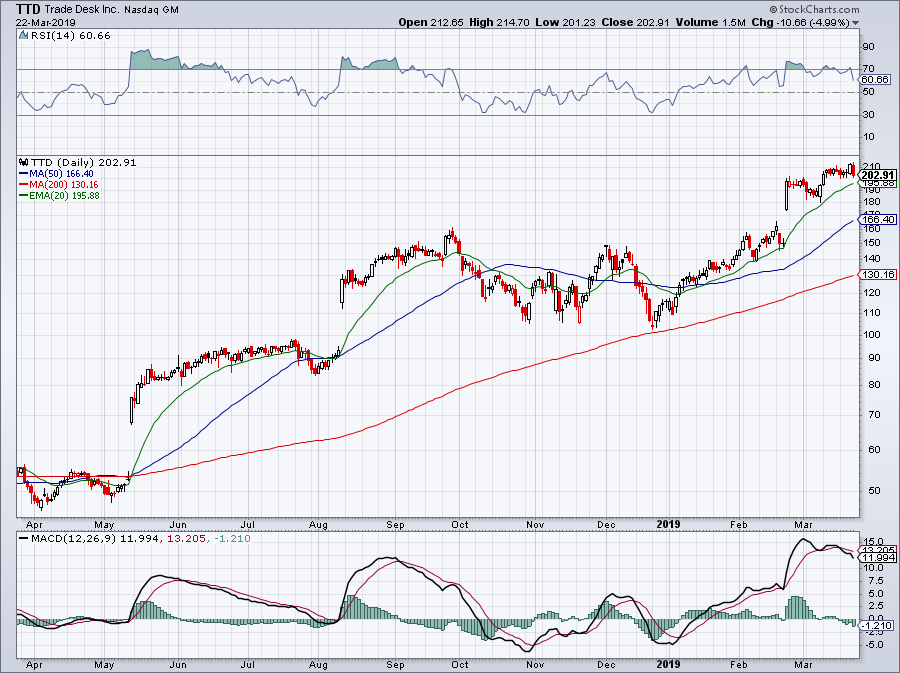

The Trade Desk (TTD)

Click to Enlarge

I barely missed my fill in this one in late December and I’m pretty darn disappointed as a result. On the plus side, I did get the next two names on this list. In any regard, let’s talk about TTD, because the growth here is simply too impressive to ignore.

When TTD reported earnings in February, it beat on earnings and revenue estimates. In fact, earnings of $1.09 per share came in a full 30 cents per share — or almost 40% — ahead of estimates. Revenue growth accelerated to 56% year-over-year and guidance for the the next quarter and full year came in ahead of expectations.

That’s music to growth investors’ ears. Beat-and-raise quarters are key to driving a growth stock higher. From CEO Jeff Green: “In the coming year, we will continue to make aggressive investments in high growth areas such as Connected TV, data, and global expansion, including in China.”

The company is free cash flow positive, which is a another huge plus for a mid-cap growth stock. Analysts expect about 35% revenue growth this year and 28% next year.

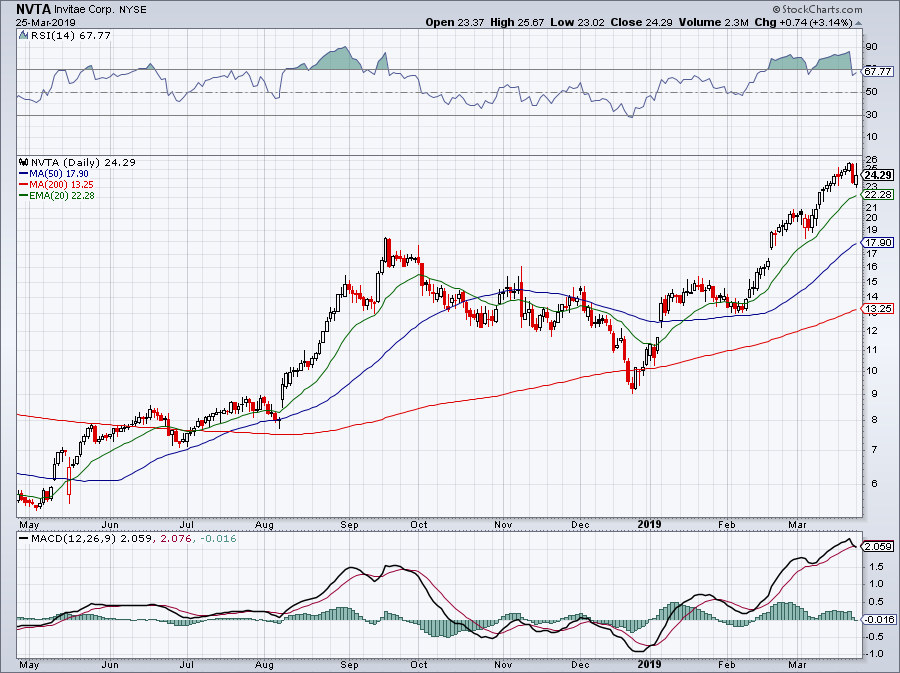

Invitae (NTVA)

Click to Enlarge

In February, NVTA beat already-heightened expectations as it grew revenue almost 80% year-over-year. After the stock’s explosive rally as a result, Invitae took advantage with a secondary offering, which was promptly bid up as investors rushed to get in this name below $20.

The recent selloff in the markets has weighed on NVTA, which almost hit $26 just a few sessions ago. Should it get back down the $20 to $21 level, I suspect it will bring buyers back in. So why is NVTA attracting so many investors? Because the company has a ton of runway right now. Estimates call for 50% revenue growth this year and 47% next year.

Even after the big run, its market cap sits at just $2 billion. M&A isn’t necessarily out of the picture at that range either, even though the company is not yet profitable. That will come soon enough.

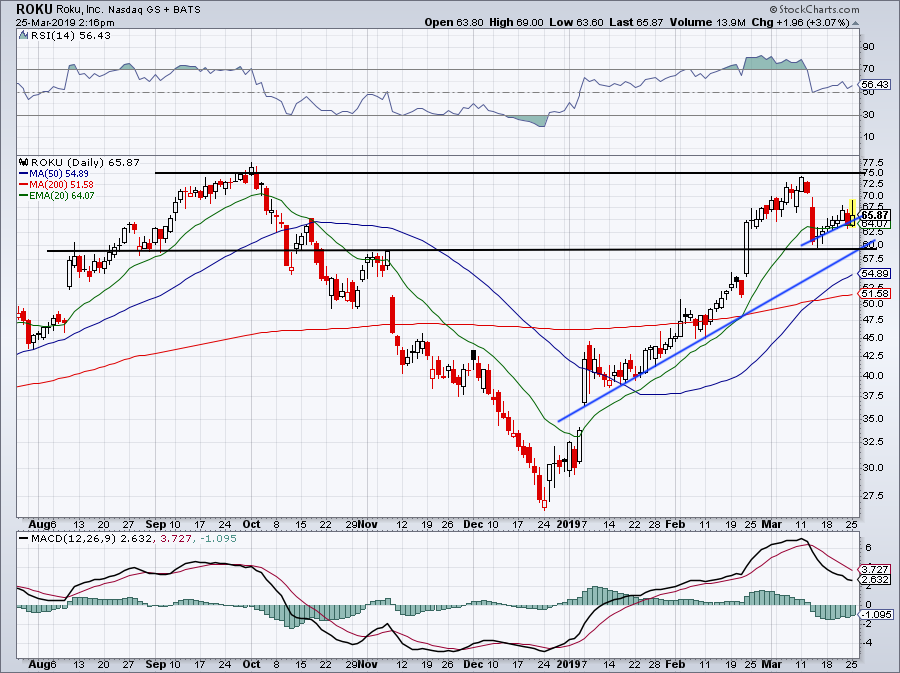

Roku (ROKU)

Click to Enlarge

The stock came up just short of making new all-time highs earlier this month. However, I wouldn’t be surprised if it happens at some point in 2019.

Many argue that Roku stock is overvalued and based on its current financials — and it is. Roku is not yet profitable, while sales are forecast to top $1 billion for the first time this year. Next year, expectations call for $1.36 billion in sales. Does that justify a $7 billion market cap?

Maybe not to some. But investors are forward looking and they can see what’s in Roku’s future.

That said, Roku is arguably the best-positioned company to take advantage of the streaming revolution. This secular shift will carry on for years and years, paving the way for tech companies to generate serious cash flow. In Roku’s case, it will eventually be profitable and go from free cash flow neutral to free cash flow positive. Its balance sheet is actually pretty strong too, with no debt, while total current assets of ~$433 million easily outweigh total current liabilities of $194 million.

If you don’t doubt streaming, then you shouldn’t doubt Roku.

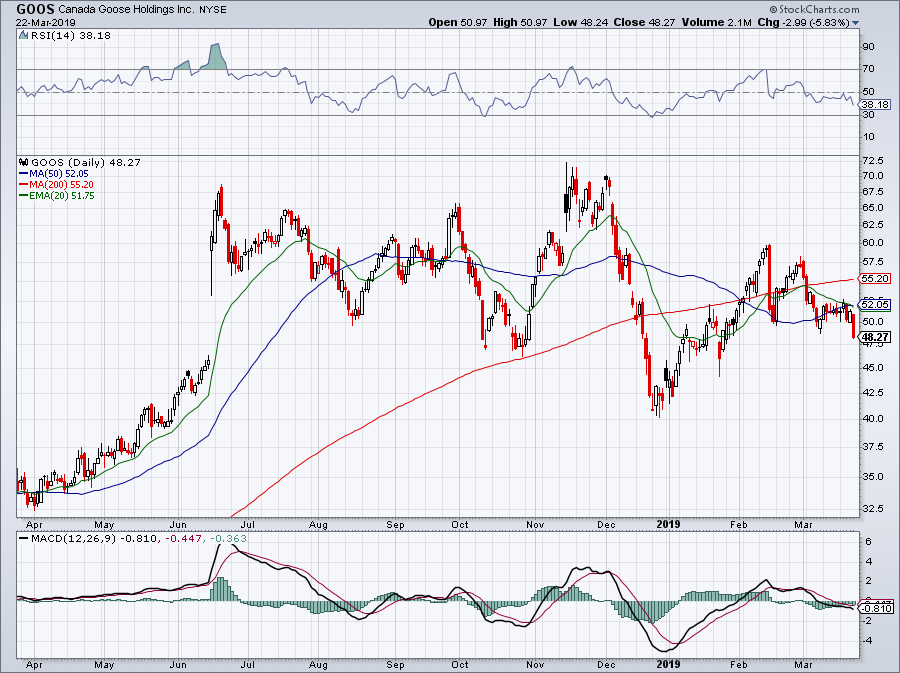

Canada Goose (GOOS)

Click to Enlarge

Get this. On February 14th, GOOS reported a blowout quarter. GAAP earnings of 93 cents a share came in 32 cents — or 52% — ahead of analysts expectations. Revenue of $399 million grew 50% year-over-year and blew past estimates of ~$266 million by 50%. This was a massive beat!

But it gets better. Gross margins improved 80 basis points to 64.4% and guidance was robust. Management expects its revenue growth rate in the mid-to-high thirties and for earnings in the mid-to-high forties. And notably, GOOS is profitable.

For whatever reason though, investors want nothing to do with it. Perhaps it’s concern over the global economy or that only so many customers will buy such expensive products. Those reasons are valid, but I wouldn’t throw out GOOS until it gives me a good reason to.

Maybe we can get this one on a discount as its charts are struggling to buoy the name.

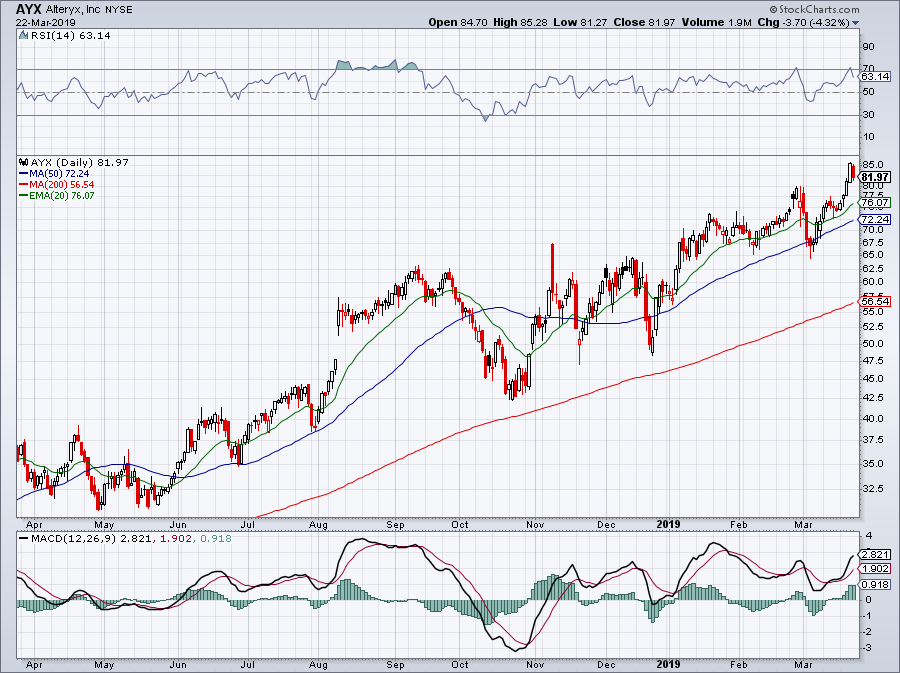

Alteryx (AYX)

Click to Enlarge

Alteryx “operates a self-service data analytics software platform that enables organizations to enhance business outcomes and the productivity of their business analysts, data scientists, and citizen data scientists worldwide.”

That kind of business model should have a long runway in this data-rich environment. Analysts are optimistic too, calling for almost 70% revenue growth this year. However, those estimates taper off to “just” 34% next year. While these estimates can always increase, it does cause some concern given AYX’s valuation. This name trades at almost 15 times this year’s revenue estimates. On the plus side, it is free cash flow positive.

I like this name, but it’s going on the back burner until we can get a better price. At its low in October, AYX was trading hands near $42.50. Just earlier this month, Alteryx was down at $65. Volatility can either work in investors’ favor or against them. Let’s make it the former.

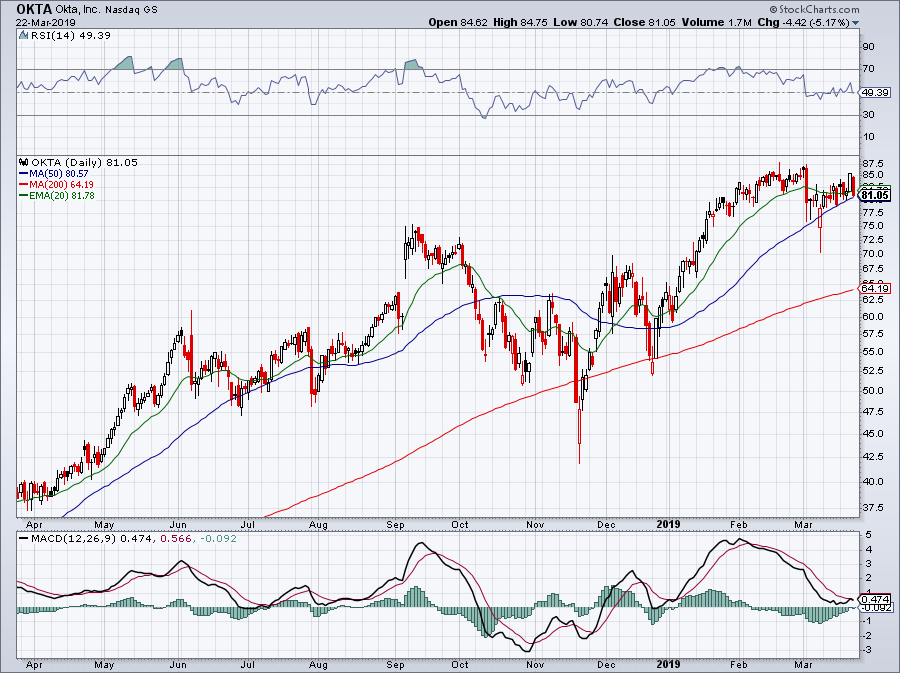

Okta (OKTA)

Click to Enlarge

Investors had a great chance in Okta stock when it reported earnings earlier this month. As investors reacted to the results, shares tumbled roughly 10% down to $70 per share. I flagged this as an overreaction before shares subsequently bounced back to the mid-$80s.

Can we get another shot at Okta at lower price?

If we get a market-wide correction, it’s certainly possible. Last quarter, revenue grew almost 50% year-over-year, while earnings and sales came in ahead of expectations. Revenue expectations came in far ahead of expectations, although management guided for a larger-than-expected loss.

At this point though, investors are willing to sacrifice the bottom line for top-line growth. That’s no surprise, particularly as Okta nears break-even free cash flow. Revenue estimates now call for 34% growth this year and 30% growth next year. That’s a solid run for Okta and it should allow dip buyers to cash in should management deliver.

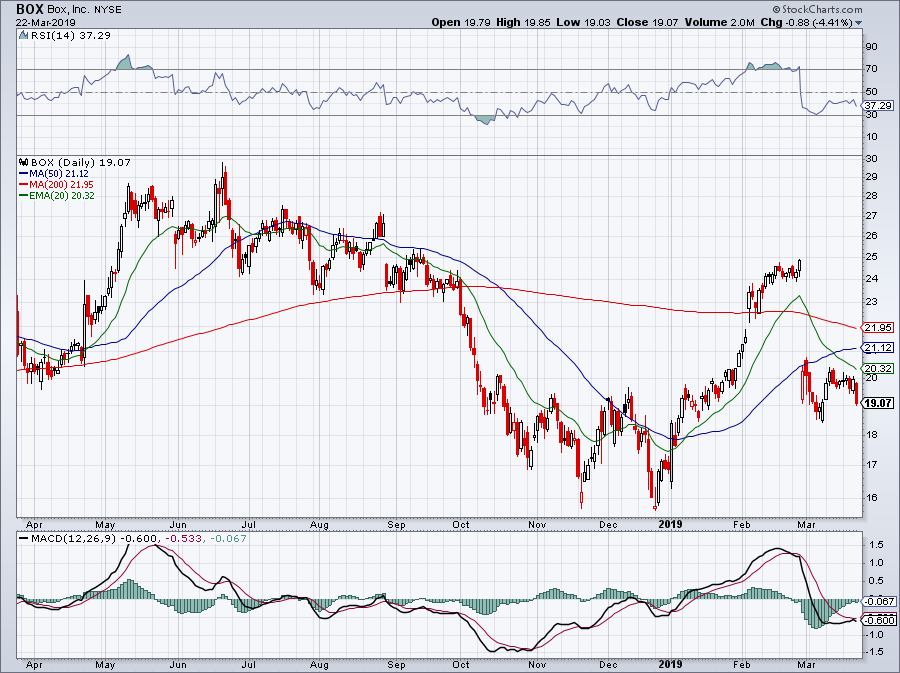

Box (BOX)

Click to Enlarge

Commanding a market cap of just $2.75 billion, that’s less than four times this year’s sales. That’s actually pretty cheap among the cloud group. But is the CEO’s seeming unwillingness to sell the company restricting that valuation? If he is, then to some extent I would say yes.

Either way, Box has a solid enough business and a low enough valuation where investors shouldn’t get too hurt owning the name. Analysts expect 15.4% revenue growth this year and 16% growth next year. Box is free-cash flow positive, as its net income hovers near break-even. Keep in mind, this stock was pushing $30 a share less than a year ago. If we can get another shot at this name at $17 or below, it may be a worthwhile investment.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AMZN, BOX, NVTA and ROKU.