Shares of Roku (NASDAQ:ROKU) have been pulverized over the past few months, despite running an excellent business. We’ve now seen Roku stock get cut in half from the highs it made just nine weeks ago.

Does it really deserve such a decline? Not really. One could argue that Roku shares were overvalued and many bulls would concede the fact that it wasn’t cheap. That said, it’s operating in a secular business environment.

Investors already know that streaming isn’t a flash in the pan; this trend is here to stay. It’s why Netflix (NASDAQ:NFLX) has outperformed so much over the past five years and why Disney (NYSE:DIS), AT&T (NYSE:T), HBO, Showtime and countless others have been rolling out their own streaming services. TV subscription companies are seeing a continual decline in cable and satellite customers, forcing them adapt to skinny bundles and other alternatives as Netflix and other cord-cutting streaming options eat into their business.

While the content wars make for an interesting debate between Netflix, Hulu, Disney, AT&T and others, Roku sidesteps most of that competition.

That doesn’t mean Roku’s without its own competition, though. Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) has the Chromecast, Apple (NASDAQ:AAPL) has Apple TV and Amazon

(NASDAQ:AMZN) has Fire TV. Don’t forget that these are three of the biggest companies in the world too.

Why Roku Can Compete

Going head to head in a hardware fight with Amazon, Google and Apple sounds like a suicide mission, doesn’t it?

On the surface, that’s what it looks like Roku is doing. But when we peel back some of the layers here, we realize it’s anything but. For starters, let’s look at last quarter. Roku grew sales 39% year-over-year (YoY), while platform revenue grew 74% YoY. Gross profit jumped 58% to $79 million.

No, Roku is not yet a profitable company, but its growth and business model are convincing. Analysts expect 42% sales growth this year and 35% growth in 2019, with break-even operations next year as well. Despite beating on top and bottom line estimates last quarter, management raised its full-year sales growth guidance up to 42% (the current expectation from analysts now). Last quarter, management was looking for 40% growth and at the beginning of the year that figure stood at 31%. They made a similar move for gross profit growth, going from 43% to 61% to most recently 63%.

That implies full-year revenue of $727 million and gross profit of ~$326 million (at the midpoints).

Hardware sales of its player grew 9%, but the platform is where it’s at. The Roku channel is one of the most popular across various app stores and is gaining in popularity. Roku holds down a 37% share of the streaming market, topping all of its mega-cap rivals. As its platform gains in popularity, we’re seeing an acceleration in gross profit and sales. Roughly 90% of gross profit came from Roku’s platform segment, revenue of which is growing much faster than the company’s overall sales growth.

As this platform continues to gain in popularity, it’s driving serious momentum for Roku’s business.

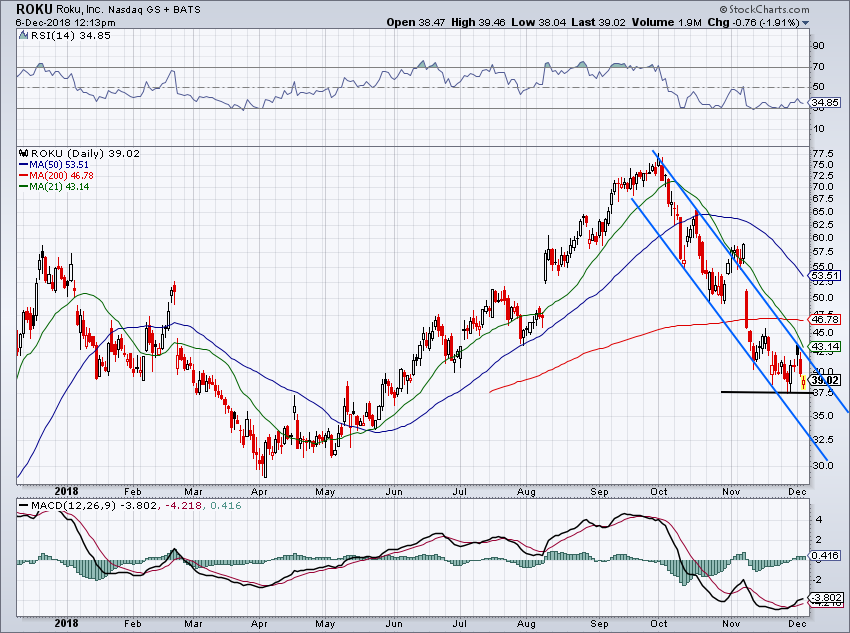

Trading ROKU Stock Price

Click to Enlarge

The fact that Roku is not only surviving, but actually thriving despite the presence of Apple, Google and Amazon shows why this stock had been so hot. That is, until October came around. Roku stock was cut down from $77.50 to $38. Shares now trade at roughly six times sales, which is on the pricey side of things, but again, we have to remember the growth here.

I don’t know when it will happen, but I do believe that Roku stock will take out its highs from 2018. From here, that represents about a 100% rally. Again, I’m not calling for this move in 2018 or possibly even 2019. As the broader market continues to buckle, Roku stock and many other mid-cap names will remain under pressure. Put simply, they don’t have the balance sheet power and dividend dependability that names like Coca-Cola (NYSE:KO) and Johnson & Johnson (NYSE:JNJ) have.

So what do the charts say?

Roku stock remains locked in a vicious downtrend. Bulls need two things right now, in this order. First, support near $37.50 needs to hold. A break below this mark opens up the possibility of a flush lower in Roku. Second, the stock needs to clear two marks, downtrend resistance (blue line) and the 21-day moving average. Third, we need to see Roku stock put in a higher low.

If it can do all of those things, the stock can regain some momentum. I expect next quarter to be another report of strong growth for Roku. It will need to be for bulls to regain some confidence and bid this name higher again.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AAPL, AMZN, GOOGL, T, and ROKU.